Rand could weaken further against dollar

Over the past year the South African currency has experienced many headwinds. Many of these resulted from home grown issues like the deteriorating local economic landscape, negative sentiment related to labour strikes, high unemployment coupled with an unsustainable large current account deficit (and the largest compared to other emerging markets). On top of this, the currency also experienced headwinds from the international landscape.

The likely direction of the Rand

Most emerging market currencies came under severe pressure after the US Federal Reserve (Fed) hinted during May 2013 that they might start reducing/tapering their quantitative easing program. As a result, many emerging markets experienced strong capital outflows as global investors sentiment turned bearish resulting in them re-allocate capital back to the US on the expectation of higher future US interest rates. These capital flows weighed on most emerging market currencies. This trend continued after the Fed indicated at their last meeting that tapering will commence in January 2014 by reducing the current programme by $10 billion per month.

Given the current level of the Rand, the question is where to from here?

The reality is that most of the above mentioned fundamentals are still present and the currency headwinds are unlikely to turn into currency tailwinds soon. Furthermore, the Fed only started tapering so the international headwinds are likely to get stronger.

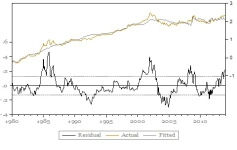

We run a simple model on the R/$ exchange rate to help us determine what a reasonable fair value should be given current underlying fundamentals (such as the current account deficit, interest and inflation differentials, commodity prices and global economic activity). The graph below shows the currency vs. such a fair value estimate (log transformation). What is more important is the black line at the bottom, showing the difference between the actual currency and the fair value estimate. For example this line (valuation indicator) clearly demonstrates that the currency deviated significantly from fair value and probably depreciated too much during 2001 and 2008. Similarly, its shows that, given the underlying fundaments at the time, the currency probably appreciated too much during 2005 and moved too far away from fair value.

The signal seems to suggest that the current level of the currency is not yet extreme compared to the underlying fundamentals at the moment. Therefore, despite the fact that it feels like we had severe currency depreciation over the past year, the model seems to suggest that it wasn’t an over-depreciation like we experienced in 2001 and 2008.

Thus, given current fundaments it seems that the currency can easily depreciate further. Even at 10.50 – 11.00 it doesn’t seem like the currency is over-stretched compared to 2001 and 2008. The Rand remains vulnerable in the event of a deterioration in risk appetite for emerging market assets. Given the uncomfortable current account deficit, it is difficult to see the currency appreciating significantly from current levels. Less foreign capital inflows coupled with the size of the current account deficit will keep the currency under pressure (despite solid capital flows into South Africa over the past two years the currency continued to depreciate, a significant change in capital inflows is likely to weigh on the currency even further). Hence, most fundamentals suggest that the currency is likely to trade in a range of 10.00 – 11.50 over the medium term with a potential risk for further depreciation.