PwC focus on rating agencies

Ratings agencies to focus on three priorities in October’s budget statement

All eyes are on newly appointed Finance Minister Tito Mboweni’s first Medium Term Budget Policy Statement (MTBPS), scheduled to be delivered to Parliament on 24 October. Just two weeks into his tenure, Minister Mboweni will face the task of affirming government’s commitment to fiscal consolidation and strategic investment in the face of low economic growth.

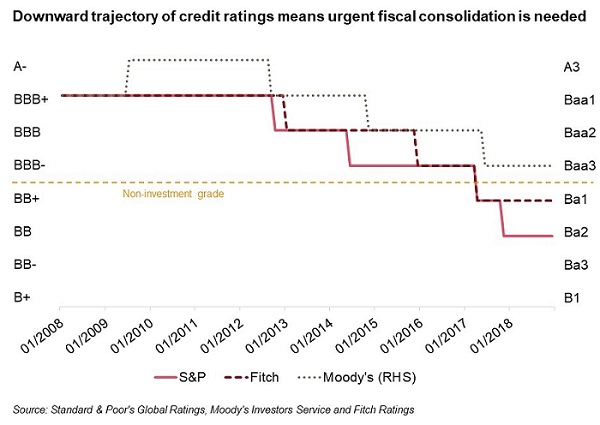

Keeping close watch of potential changes to the creditworthiness of South Africa’s sovereign, ratings agencies S&P Global Ratings, Moody's Investors Services and Fitch Ratings will be looking out for key credit-relevant details in the MTBPS.

In September, Moody’s offered South Africa some good news, when it noted a downgrade of South Africa’s credit rating to below investment grade was unlikely in the near future. Moody’s is the last of the three major credit rating agencies that has kept South Africa’s credit rating at investment grade level, currently with a stable outlook. If Moody’s were to downgrade South Africa’s debt to sub-investment level, South Africa would be removed from the Citi World Government Bond Index, prompting asset managers and pension funds to sell domestic bonds. This would sharply increase the cost of debt and pressure the exchange rate. In view of South Africa’s limited fiscal room, hopes are high that the MTBPS will be, on balance, credit positive.

Ratings agencies will likely look out for three priority areas that could trigger changes to the country’s credit rating, namely 1) the pace of fiscal consolidation, 2) reforms in state-owned enterprises (SOEs) and 3) measures to lift economic growth.

1. Continued commitment to fiscal consolidation

Consolidation measures that narrow the budget deficit and achieve a substantial reduction in the government debt-to-GDP ratio are deemed credit positive by ratings agencies.

Following a notable increase in projected debt-to-GDP levels announced in the previous MTBPS, ratings agencies responded negatively, and S&P downgraded South Africa’s credit rating further into sub-investment grade territory.

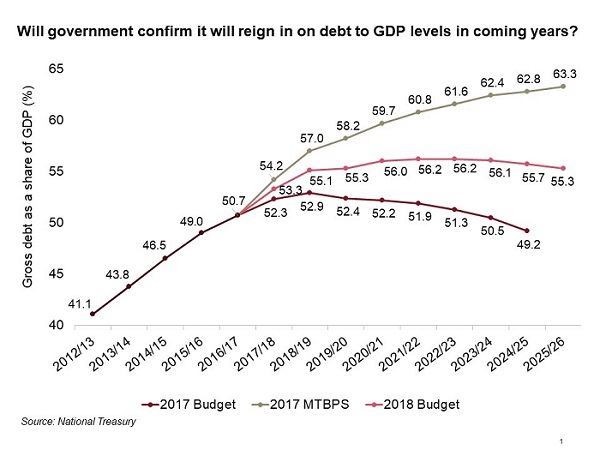

The 2018/19 fiscal budget (delivered in February this year) outlined a series of measures to rebuild economic confidence and return public finances to a sustainable path. These included R85 billion in spending reductions and various tax hikes, including a 1 percentage point increase in value-added tax (VAT). The proposals emphasised government’s renewed commitment to right the fiscal ship.

February’s budget proposals suggested a considerably narrower budget deficit (as a percentage of GDP) than was presented in October last year, indicating a path to debt stabilisation over the long term.

To be viewed as credit positive, a similar outlook should be presented in October this year, which would reiterate a commitment to fiscal restraint in the face of difficult prioritisation decisions.

2. Reform in state-owned enterprises

The National Treasury has noted on several occasions that the debts of SOEs have grown rapidly, with large government guarantees and the long-term viability of many SOEs increasingly presenting a fiscal risk. Capital markets have pulled back their lending to some SOEs in the absence of reforms, and ratings agencies increasingly highlight the financial state of SOEs as a matter of routine.

Ratings agencies will look out for any measures announced in the MTBPS that help to stabilise the precarious finances of SOEs. Measures focused on improved governance, clarifications of mandate and strategy, strong oversight and regulation, as well as enhanced operational efficiency could significantly improve the developmental impact and financial viability of SOEs. These, in turn, would be viewed as credit positive by ratings agencies.

3. Focus on economic growth

South Africa entered a technical recession in the second quarter of 2018. Depressed economic conditions commonly precipitate pressure on tax revenues. If not met with changes in government expenditure, poor economic performance reduces government’s ability to meet its loan agreements, ultimately affecting its sovereign creditworthiness. Ratings agencies will watch closely what measures could be announced to improve the outlook for the South African economy.

In response to poor economic conditions, President Cyril Ramaphosa announced a stimulus and recovery package in September aimed at boosting economic growth and job creation. In addition to the implementation of an infrastructure fund and the reallocation of R50 billion in fiscal funds towards high-impact growth projects, the package aims to provide policy certainty for the telecommunications, agriculture, and mining sectors in particular.

More detail may be presented in the MTBPS to outline how the fiscal package will target priority sectors, and spur economic growth and job creation without risking fiscal consolidation. The ratings agencies will look closely to determine whether these interventions will lift the outlook for potential growth in the medium term.

In the meantime, however, National Treasury will likely revise downward its 2018 growth expectations. During February, the National Treasury forecast annual GDP growth of 1.5% in 2018. Considering average economic growth of only 0.6% in the first half of 2018, South Africa would have to achieve economic growth of 2.4% y-o-y on average in the second half of the year to achieve this forecast.

Trends across the economy, however, suggest the cyclical upswing is slow to materialise, with economic growth of below 1% likely this year. While slow economic growth is viewed as credit negative, measures that raise the growth trajectory sustainably would, however, provide support to South Africa’s credit rating.

If the MTBPS effectively addresses all three priority areas, ratings agencies are likely to respond favourably. In the end, South Africa’s credit rating remains a crucial ingredient for keeping the costs of debt under control, and freeing up spending for South Africa’s most pressing economic challenges, including the alleviation of poverty, inequality and unemployment.