Policy ambiguity constrains infrastructure, forcing local contractors to look abroad

Patricia Zvarayi, a senior analyst at GCR.

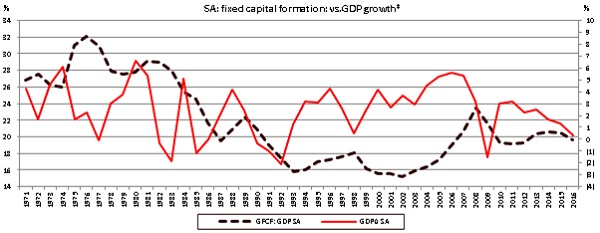

Despite South Africa exiting from a technical recession in the second quarter of 2017, the economy remains fragile, with weak growth exposing widening structural fissures and further polarising the socio-political discourse.

A critical component of creating sustainable growth in the economy is through capital investment, as it accelerates the pace of growth. As such, the contraction in investment seen in the past 15 months - following decades of sluggish fixed capital accumulation - has the effect of constraining economic growth well into the long term.

According to Patricia Zvarayi, a Senior Analyst from the Global Credit Ratings Co. (GCR), the construction industry is the perfect vehicle for government and private sector to create growth in the economy through large projects, which drive job creation and community upliftment.

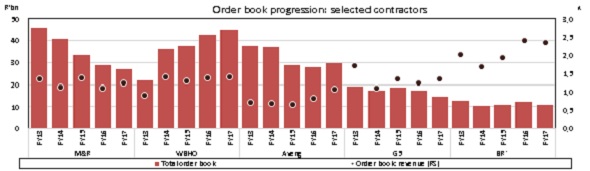

“Erratic public infrastructure spend has exacerbated the cyclicality of the construction sector. In the run-up to the 2010 World Cup for example, we saw strong order books for South African contractors. Since then, the Medupi and Kusile power stations have dominated contractors’ local workflow, not only due to their scale, but also due to a limited flow of major projects coming to market,” says Zvarayi.

The commodity downcycle and uncertain policy direction with respect to the mining charter, the Mineral and Petroleum Resources Development Amendment Bill, and the land expropriation bill, have significantly reduced the construction deal flow from that sector.

*1H position for FY17.

Murray & Roberts has been reclassified to General Industrials, and is included for historical comparison/illustrative purposes.

Broader policy direction that impacts investment decisions also has a downstream impact on construction activity, whether planned or inadvertent. Hawkish monetary policy during a period of stagflation, for example, has contributed to restricting consumer spending, weak domestic demand, and corporates deferring fixed capital accumulation decisions. As a result, listed contractors have shown a pronounced shrinkage in their domestic order book, while poor financial performance resulting from the loss of scale economies have been worsened by legacy claims, low-to-zero-margin work and underperformance on certain projects.

Accordingly, contractors that have developed a wider geographic footprint typically show more stable credit risk profiles than peers that are focused on the local market.

Although much more diversified than most emerging economies, South Africa remains strongly reliant on the commodity cycle for economic stimulus. “This is an indication that South Africa simply isn’t spending enough on infrastructure, which is the engine of sustainable growth in any economy,” warns Zvarayi.

*GDP growth: RS

Source: World Bank

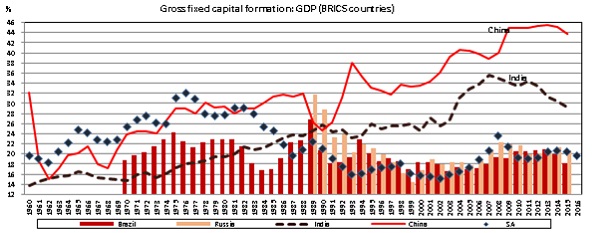

South Africa’s ratio of fixed capital formation to GDP is around 20%, which according to the World Economic Forum, is just enough to stave off fixed capital erosion.

“This is well behind South Africa’s strong-performing BRICS peers, China and India, whose particularly high spend on infrastructure underpinned the economic transformation both countries have achieved. Anecdotal evidence points to rates c.35% of GDP sustaining sufficient growth to double an economy within 10 years,” says Zvarayi.

Source: World Bank

It is crucial for the economy that more infrastructure projects are in the pipeline and rolled out, this will provide contractors a much stronger workflow domestically.

“This will only be achieved when the ambiguity surrounding policy direction makes way for clarity. Government needs to provide clear and precise legislation that attracts foreign direct investment and stimulates domestic productivity,” explains Zvarayi. “This will engender a stronger pipeline of higher-yielding infrastructure projects which will see sustainable economic growth in the country and contribute to stabilising the credit risk profiles of large contractors,” says Zvarayi.

She clarifies that industry and government have set the groundwork to find solutions. The seven largest contractors’ commitment to the Voluntary Rebuild Programme and progress on the draft Construction Sector Code shows positive sector engagement with government in support of transformation.

National Government is also looking for solutions to have metros, SoEs, and the private sector fund more infrastructure projects to relieve pressure on the fiscus, but given the economic headwinds and the country’s constrained fiscal position, this is not likely to unlock meaningful workflow in the intermediate term.

To stimulate inclusive growth in the value chain in the South African construction industry, it is important for large contractors to ensure the engagement of small and emerging players on a steady stream of projects. “This will entail the South African government unlocking a stronger workflow through direct investment in public infrastructure, and by providing an enabling environment for the private sector to increase its fixed capital spend,” concludes Zvarayi.