October’s headline rate of inflation rises above expectations

Sanisha Packirisamy, Economist at Momentum.

Herman van Papendorp, Head of Asset Allocation at Momentum.

Headline consumer price inflation (CPI) rose to 6.4% y/y, marginally higher than our own and the market’s estimate for October 2016.

Headline inflation exceeded expectations, but is likely nearing a peak

In month-on-month terms, inflation increased by 0.5%, partly owing to higher food and transport costs.

In addition to the monthly surveys, recreation/culture (including gymnasium fees, soccer tickets and television licences) and funeral costs were surveyed. Recreation/culture inflation increased to 6.7% y/y in October 2016, from 2.9% y/y a year ago. Inflation associated with other services (including funeral costs) spiked to over 8% in year-on-year terms, significantly higher than the 2.8% y/y rate recorded a year ago.

Relative to our own forecasts, prices of durable (furniture and household appliances) and semi-durable (clothing and footwear) goods increased by slightly more than expected while the price of vehicles increased by less than anticipated, most likely in response to poor vehicle sales observed of late.

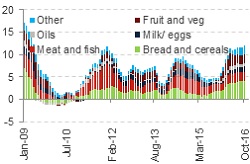

Strong rise in food prices, but likely nearing a peak

Food inflation picked up by 1% m/m, leaving the year-on-year rate close to 12%. Inflation in bread/cereal prices remains high at 16.5% y/y, while meat price inflation remained within the 3% - 6% target band. Over the course of 2017 we expect a faster rise in meat prices as farmers are likely to focus on rebuilding herds that were culled during the drought, limiting meat supply and forcing prices higher. Nevertheless, a sharp move lower in rand maize prices thanks to an improvement in rainfall should allow food inflation, overall, to fall meaningfully to an estimated 2% by the end of 2017.

Chart 2: Contribution to food inflation (% y/y)

Source: Stats SA, Global Insight, Momentum Investments

Lower food inflation in 2017 should provide some relief to lower-income earners

The gap in inflation experienced between low-income earners (earning up to R14 564 p.a.) and high-income earners (earning over R79 153 p.a.) has exceeded 2% over the past seven months. This is largely due to the sharp rise in food inflation accounting for a larger share of the lower-income earner’s consumption basket. Should food inflation dip markedly over the course of 2017, as we expect, lower-income earners may experience some much-needed relief in terms of the growth in their real (inflation-adjusted) wages.

Another substantial rise in petrol costs expected for November, but could reverse in December

A 44c/l Gauteng 95 petrol price increase in October 2016 led to a 2.9% m/m rise in private transport costs. A 45c/l hike followed in early November suggesting another meaningful monthly inflation contribution from petrol prices which could leave the year-on-year rate in private transport costs closer to 5.5%. The current over-recovery in the petrol price for December is however pointing to a fuel price cut of around 43c/l.

Core inflation ticks higher

The Reserve Bank’s measure of core inflation (headline CPI excluding the impact of food, non-alcoholic beverages, petrol and energy) increased to 5.7% y/y in October 2016 from 5.6% y/y a month earlier. We expect core inflation to drift lower from a projected 5.6% average in 2016 to 5% in 2017. A recent study by the Reserve Bank on currency pass-through shows that retailers are less likely to pass on cost increases related to rand depreciation in a downward phase of the economic cycle as their attention shifts to protecting volume growth. With consumers facing significant headwinds including further job losses, declining growth in wealth (namely house and equity prices) and lower real disposable income growth, retailers have likely not passed on the full extent of prior rand depreciation. As such, we have experienced a more muted impacted on core inflation this time around.

Interest rates likely near the peak

Despite the higher than expected inflation print for October 2016, our projections point to a decline in overall inflation from around 6.3% in 2016 to an estimated 5.6% in 2017 (largely owing to lower food prices) and a sharper fall to below 5% in 2018 (thanks to an expected appreciation in the currency in response to a mild uptick in commodity prices as the overhang in supply narrows). The outlook for inflation expected to return to within the target band, coupled with low growth, suggests that we are likely near the peak in the current interest rate cycle.

Nevertheless, we believe that interest rate cuts are still some way off given upside risks to the inflation profile posed by a volatile domestic currency and above-inflation nominal wage settlements. Moreover, core inflation shows signs of underlying inflationary pressures, while inflation expectations by businesses and labour unions remain elevated, even over a five-year horizon, posing a risk to headline inflation.