MTBPS shows fiscal prudence despite many obstacles

Lullu Krugel, Chief Economist at KPMG South Africa.

Christie Viljoen, Economist at KPMG South Africa.

Minister of Finance Pravin Gordhan delivered the Medium Term Budget Policy Statement (MTBPS) 2016 to Parliament on Wednesday, October 26. The MTBPS is a government report providing information on the country’s economic context, fiscal objectives, and spending priorities over a threeyear period. Given South Africa’s current economic and political context, this year’s MTBPS was one of the most anticipated since the annual statement was launched almost 20 years ago.

A weak economy in need of investment

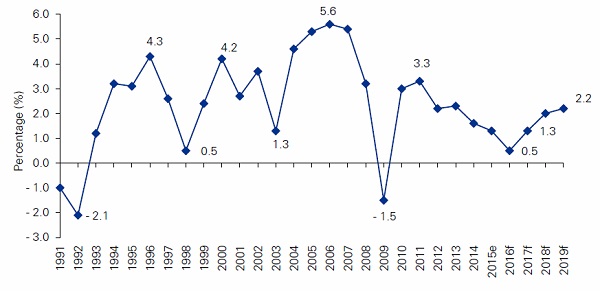

The National Treasury now expects real GDP growth of only 0.5% this year and a below-trend 1.3% in 2017 due to the impact of an uncertain global economy and low (local and foreign) investor confidence. Echoing recent comments from the South African Reserve Bank (SARB), the minister indicated that this low level of confidence stems from elevated political risk and concerns about the ability of public institutions to make good decisions.

Figure 1: Real GDP growth (%) 1991 – 2019f

Source: Business Monitor International (BMI) and National Treasury

To achieve faster economic growth, the country needs more private sector investment. Private investment has fallen in all sectors this year and is expected to contract in real terms by 2.9% in 2016 – the first decline since 2010. On a positive note, the government is pleased with efforts in the labour sphere resulting in the number of working days lost to strikes declining, and a depreciation in the rand boosting the country’s export prospects. This should, in theory, support greater investment.

However, if GDP growth remains below 2% - the country’s current potential growth rate based on known constraints - the government will not be able to sustain current spending based on its policy directives. Growth will need to return to 3% p.a., according to the MTBPS. The need for faster growth is limiting the speed at which Minister Gordhan can narrow the budget deficit, as an aggressive fiscal consolidation drive could see the economy stuck in a low-growth trap.

With this in mind, the minister and his department will continues to work towards a stable and sustainable fiscus. Combined with transparent monetary policy and economic reforms, this, he argued, will result in economic growth rising to the +5% levels envisaged by the National Development Plan (NDP). He warned that everyone in South Africa needs to work towards achieving reforms that will remove obstacles to faster, inclusive, job-creating growth.

The MTBPS is frank about what these growth obstacles are, and they are all significantly influenced by government activity and policy: infrastructure bottlenecks, low levels of competition in certain (unnamed) markets, a volatile labour relations environment, regulatory constraints, red tape, inefficiencies in state-owned enterprises (SOEs), and economic policy uncertainty. Success in reducing these obstacles depend on how well these efforts are coordinated and put into action.

Tax policy measures needed to boost revenues

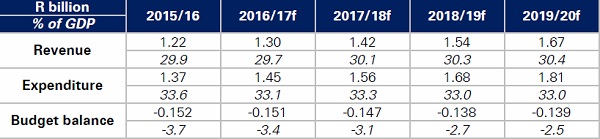

Weaker economic growth will result in a R23 billion shortfall in previously projected tax revenues during 2016/17. The South African economy is currently characterised by low consumer confidence, which directly translates into weaker value-added tax (VAT) collections – if consumers do not spend on goods and services, VAT cannot be levied. The impact of this and other pressures will result in projected government revenues of R1.3 trillion in 2016/17, equal to 29.7% of GDP.

The government will look to raise an additional R43 billion in revenue during 2017/18 – 2018/19 through “tax policy measures”. The MTBPS, however, did not detail these measures. It is likely to include the planned tax on sugar-sweetened beverages (SSBs), which the statement did not elaborate on. There was no hint of increasing personal income tax rates next year but the National Treasury is keeping all options on the table.

Table 1: Consolidated government fiscal framework

Source: National Treasury

Reprioritising government spending amidst diverse demands

Cost containment measures introduced in December 2013 saw a real decline in spending on

consultants, travel, catering, as well as stationary and printing. The Office of the Chief Procurement Officer (OCPO) is hard at work to further improve the quality of spending and addressing the R240 billion in state spending currently affected by inflated prices. Cabinet will consider a Public Procurement Bill before April 2017 in this regard.

State expenditure is expected to total R1.45 trillion during the current fiscal year, equal to 33.1% of GDP. Spending is planned to increase by an average of 7.6% p.a. during 2016/17 – 2019/20 to reach R1.81 trillion in the final year of the period. In light of the country’s deteriorated economic conditions over the past six months, the expenditure ceiling has been reduced by another R10 billion in 2017/18 and R16 billion in 2018/19 from the levels planned in February this year.

Considering that the National Treasury expects government debt (as percentage of GDP) to only stabilise in 2019/20, debt service costs will rise by 10.1% p.a. during 2016/17 – 2019/20, and will account for 10.5% of fiscal spending in 2017/18. The second highest expenditure increase will be on spending for post-school education and training. Admittedly, most of this will go to early childhood development as well as vocational and technical skills training – this is in line with the post-school education goals set out by the NDP.

Transfers to universities and the National Student Financial Aid Scheme (NSFAS) will rise by 10.9% p.a. and 18.5% p.a., respectively, over the medium term. Some of the money will come from a drawdown in the state’s contingency reserves. Furthermore, instead of committing to free tertiary education, the MTBPS indicated that a roadmap is needed towards fully financing the cost of study for poor and working class families. The plan will have to consider how to maximise social and economic transformation. This implies that if university education were increasingly subsidised, the benefits (i.e. increased quality of labour supply) would need to benefit the country as a whole.

A new agreement on public sector wages must be finalised by April 2018. Compensation of public sector employees is planned to increase by an above-inflation 6.9% p.a. over the medium term. At the same time, the National Treasury wants to see a decline in the public sector staff headcount. With no executive power to order the dismissal of workers, the MTBPS indicates that a headcount reduction will be achieved via the freezing of posts left open by people resigning or retiring.

Budget balance still planned to narrow in coming years

The MTBPS indicated that the fiscal deficit will narrow from 3.7% of GDP in 2015/16 to 3.4% of GDP in 2016/17 – the latter number is 0.2 percentage points higher than planned in the 2016/17 budget speech, though the increase is in line with economists’ expectations. The budget shortfall is projected to narrow to 2.5% of GDP – seen as a sustainable level – by 2019/20. However, the minister acknowledged that budgets tend to be optimistic about outer-year forecasts. Just two years ago, the National Treasury projected GDP growth of 3.5% in 2016/17, and its current projection for this year (0.5%) is also above that of most local economists.

On a positive note, fiscal consolidation in recent years will result in a primary surplus during 2017/18 – this means that government revenue will be higher than non-interest spending. This has resulted from the expenditure ceilings introduced in the 2015/16 and 2016/17 budgets being enforced and proving effective in curtailing overspending. When also considering that real government spending per capita has been stable since 2010/11, there is no denying that fiscal consolidation – at a measured and balanced speed - is in place and working.

However, the minister warned that “several SOEs could pose risks to public finances.” These include South African Airways (SAA), Eskom, the Post Office, and SANRAL. In order to stabilise these entities, the Presidential State-Owned Companies Coordinating Council will coordinate and monitor interventions, with the statutory responsibilities of the boards and executives of these SOEs remaining unchanged.

Will this be enough to appease rating agencies?

S&P Global Ratings currently rates South Africa “BBB-“ (the lowest possible investment-grade rating) with a negative outlook, and any adverse adjustment to this assessment would see the country moved to non-investment grade. S&P will publish its latest official review of the sovereign’s rating during the first week of December. In early October, the agency warned that low economic growth and the threat of political tensions hampering much-needed reforms are challenging the country’s rating.

Minister Gordhan led a high-level delegation to New York in early October to convince investors and rating agencies that he government, private business and labour are working together to avoid a ratings downgrade. The MTBPS 2016 showed that the National Treasury remains strongly committed – within exiting constraints - to placing the fiscus on a more sustainable trajectory, despite some widely publicised recent political distractions.

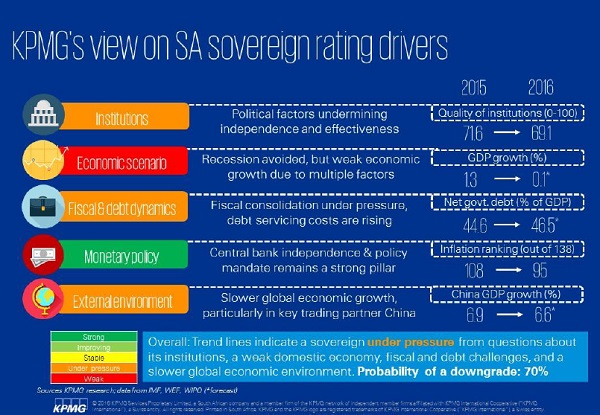

In their assessments of sovereigns, rating agencies consider a country’s institutions, economic scenario, fiscal and debt dynamics, monetary policy and the external environment. If it is assumed that S&P will be happy with the MTBPS 2016, that still leaves the economic scenario and quality of institutions to worry about. In recent months, several of the world’s largest rating agencies have commented that South Africa’s current political situation is pressuring the quality of key institutions – e.g. the National Treasury, Office of the Public Protector, and the judiciary.

Figure 2: KPMG’s view on South Africa’s sovereign rating drivers