Mining and manufacturing unlikely to boost 3Q15 GDP growth meaningfully

Sanisha Packirisamy, Economist at MMI Holdings Investments and Savings.

Herman van Papendorp, MMI Head of Macro Research and Asset Allocation.

Weak commodity prices and subdued global demand weighs negatively on SA mining production.

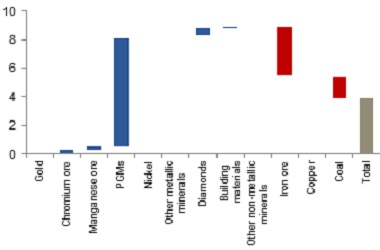

Stats SA mining production volumes increased by 3.8% y/y in August (4.0% y/y in July), but contracted by 1.1% in month-on-month terms as low global commodity demand kept mining volumes under pressure. Production in the platinum group metals (PGMs) sector was the largest growth contributor to overall mining growth in year-on-year terms, while a fall in iron ore production volumes detracted the most over the same time period (see chart 1). With a depressed, strike-impacted platinum production base likely to roll out of the numbers soon, overall year-on-year mining production growth is likely to come under pressure given weak global demand, low commodity prices and electricity supply constraints.

Chart 1: PGMs the largest contributor to growth in mining production volumes in August (% y/y)

Source: Stats SA, Momentum Investments

Coal production shaved off a further 1.5% from overall growth in mining production volumes in August. Potentially lower strike-induced coal production volumes add further downward pressure on mining performance, given this sector’s hefty c.25% weight of the total mining production basket. On the 4th of October, thousands of workers affiliated to the National Union of Mineworkers (NUM) went on strike for higher wages, including demands for a R1 000 monthly increase for the lowest paid workers. This affected operations at several key coal companies and could further threaten the production of coal volumes should the strike extend longer than a two-three week period. With Eskom’s current coal stockpiles sitting at around 45 – 55 days, the coal strike is not expected to pose any major risk unless the strike extends for a prolonged period.

Benign global commodity demand and weak commodity prices cloud the outlook for SA’s mining industry, while uncertainty over economic policy and labour unrest will likely prevent a faster acceleration in capital expenditure and employment growth in the sector. The Fraser Institute’s Annual Survey of Mining Companies in 2014 emphasised that SA’s “highly-political, unionised workforce that perpetually demands more and more in return for less and less productivity” and “inadequate power generation and inadequate labour laws regarding mineral sector strikes” have reduced investment attractiveness in SA’s mining industry, even when compared to a number of African economies including Namibia, Botswana, Zambia, Tanzania, Mali and Ghana.

Manufacturing production volumes disappoint

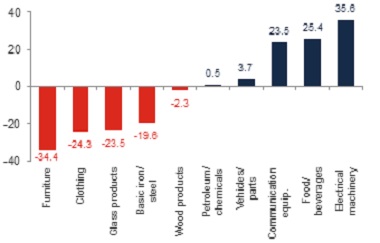

Manufacturing production volumes declined by 0.2% y/y in August, after posting an upbeat 5.3% y/y print in July, disappointing market expectations for a 1.4% y/y rise. According to Stats SA, the largest negative contribution was made by the basic iron and steel, metal products and machinery divisions, while the petroleum/chemicals and food/ beverages sectors were the largest positive contributors to year-on-year growth in August.

Growth in production volumes has been particularly poor in the furniture and clothing sectors. Here, production volumes fell by 34.4% and 24.3%, respectively, relative to 1Q08 levels (see chart 2). Meanwhile growth in production volumes has been stronger in the electrical machinery, food/beverages and communication equipment sectors, resulting in levels which are 35.6%, 25.4% and 23.5% higher (respectively) in comparison to 1Q08 levels.

Chart 2: Change in manufacturing production volumes since 1Q08 (%)

Source: Stats SA, Global Insight, Momentum Investments

The September Bureau of Economic Research (BER)/Barclays Purchasing Managers’ Index (PMI), a popular gauge of manufacturer sentiment, remained largely unchanged at 49 index points, signaling strain in the SA manufacturing sector. Although rand weakness and the continued recovery in the Eurozone may have provided some support for exporters, an uptick in the price sub-index and subdued domestic demand has prevented a further acceleration in manufacturing volumes. Moreover, the BER warns that potential adverse spillovers from the slowdown in China and the negative impact on commodity producers and prices could hamper growth in the SA mining industry, further affecting the manufacturing industry given the strong backward (machinery/equipment, transport equipment, petroleum/chemicals) and forward (basic metals, vehicles, chemicals) linkages between mining and manufacturing.

No changes to weak SA growth view

Mining production volumes contracted by 3.3% in August, based on the quarter-on-quarter seasonally-adjusted measure, while manufacturing production dipped by a further 0.3% on the same basis, suggesting little chance of a meaningful positive contribution to 3Q15 real GDP growth. Elevated input costs, soft global demand and benign commodity prices remain challenging for SA’s mining and manufacturing sectors.