March 2017 retail sales surprise positively, but momentum remains weak

Sanisha Packirisamy, Economist at Momentum.

Herman van Papendorp, Head of Asset Allocation at Momentum.

Real retail sales increased by 0.8% in year-on-year (% y/y) terms in March 2017.

Low base effect boosts retail sales in specialised food and furniture categories

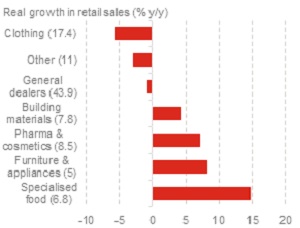

Buoyed by a robust 14.8% y/y increase in the sales of specialised food, beverages and tobacco, followed by a rebound in growth in furniture and appliances sales to 8.2% y/y. These growth rates compare favourably when compared to the average growth rate of 3.8% y/y and negative 3.3% y/y over the past twelve months, respectively.

Nonetheless, the largest contributors to retail sales, namely sales by general dealers and retailers of textiles and clothing, which cumulatively account for more than 60% of total monthly sales, experienced negative growth in sales volumes relative to a year ago. Sales by general dealers dipped 0.8% y/y in March 2017, while sales by textile and clothing retailers experienced an even sharper contraction (negative 5.6% y/y).

Despite retail sales increasing by more than expected in March 2017 relative to a year ago in real terms, volumes decreased by 1.1% between the 3-month period October to December 2016 and the 3-month period between January and March 2017, indicating a slowing in retail sales momentum.

Chart 1: Negative sales growth in the largest contributors

Source: Stats SA, Global Insight, Momentum Investments. contribution weights in brackets

Chart 2: Households pessimistic about economic outlook

Source: Stats SA, Global Insight, Momentum Investments

Households are under pressure

Consumers are still feeling financially exposed. The latest MMI Unisa Consumer Financial Vulnerability Index ticked higher to 52.7 points in the fourth quarter of 2016, but at this level, the index suggests that consumers’ cash flow remains impacted and households are still at risk of becoming financially vulnerable. Scores were lowest in the savings and debt servicing sub-components. The latter has been confirmed in the latest fourth quarter reading of the TransUnion Consumer Credit Index, which ticked lower to 49.6 points (50 = breakeven). TransUnion pointed out that the sideways trend in the Consumer Credit Index over the past year is indicative of a consolidation in consumer credit markets in a difficult economic environment. Although distressed borrowing sub-indicators remained in check, household cash flow remained under pressure.

Prolonged growth weakness and elevated economic and political uncertainty point to further consumer stress in the short to medium term. The Bureau of Economic Research’s Consumer Confidence Index slipped back to negative 10 points in the final quarter of 2016 from negative 3 points a quarter before. Households have become increasingly glum over the economic outlook over the next year and continue to rate the present time as inappropriate to buy durable goods (including cars and furniture).

Muted growth outlook

Depressed consumer sentiment, high household debt burdens, higher taxes, tepid credit growth and a poor employment outlook continue to weigh heavily on the South African consumer, while uncertainty over the likely direction in economic policy hinders fixed investment spend in the private sector. Momentum Investments anticipates a shallow recovery in economic growth from 0.3% in 2016 to 0.9% in 2017, with continued pressure in the domestic demand components, while an improvement in export growth and a marginal inventory rebuild should support a mild recovery in overall economic activity this year.