Macro Digest: The mood sours

• Excessively low inflation problematic for risk assets • ECB, BoJ & Fed showing different degrees of ineptitude • Yellen is much more dovish than folk realise

I have had several macro conference calls and speaking engagements over the course of this week – a few takeaways:

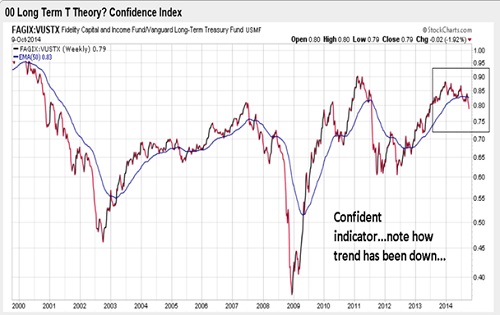

1. The mood has changed – See the “confidence index” from T Theory below for data. The driver in my opinion is the gradual acceptance of disinflation/deflation – as Albert Edwards has been pointing out and as Russel Napier has substantiated that when inflation gets low enough it becomes a problem for risky assets.

2. There is growing belief that the “narrative of the central banks” is failing. We've had such low yields for so very long now that it's becoming an issue. I've discussed this with several of you and the consensus opinion is that the European Central Bank's Mario Draghi lost out with his latest “wide in scope, small in size” programme; that the Bank of Japan looks like a deer caught in the headlights; and most importantly, Fed chief Janet Yellen and her team are doing a poor job in communicating their message.

There is even open resentment of Yellen as a female chair. I don’t condone any of the Fed's policies, but I firmly believe Yellen is misunderstood. She is more dovish than the market can figure out and in contrast to her predecessors, she allows more room for the opinions of fellow board members. This is why we are seeing Stanley Fischer being a new and much-improved voice for the Fed, as is also the case with William Dudley. Further, Yellen is considerably better than both Alan Greenspan and Ben Bernanke in terms of understanding the mechanics of the Fed and the economy.

Janet Yellen is far more of a dove than people realise. Photo: Federal Reserve

Finally on the Fed – I never understood how the market could pay so much attention to regional presidents. They are politicians, representing either specific economic agendas relative to their own region or are subscribers to some specific economic theory. Let’s hope the “dots” die soon as they are without doubt the most useless pieces of information ever. (You can reach a specific growth forecast from many angles being one of the issues.)

3. Central banks are now concerned about the velocity of foreign exchange moves (ECB and BoJ) and the Fed is explicitly worried about the impact on future US growth. This major change – a vocal change as often before initiated by New York Fed’s Dudley (September 21, 2014) and confirmed by Fed Minutes this week: "Officials at the Federal Open Market Committee’s Sept. 16-17 meeting warned that the stronger dollar may hamper exports, and said the economy could be hurt by a global slowdown.

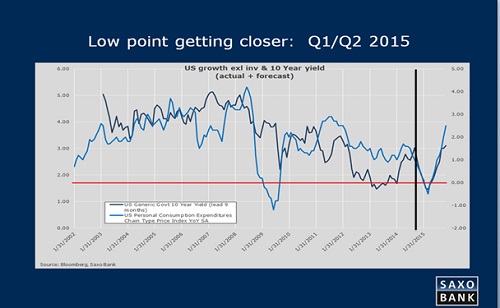

Of course 95% of Wall Street and 98% of all hedge funds remain long US dollar as it’s an island of strength – my model, however, disagrees, as seen below. The vertical line is the present…..

Source: Bloomberg, Saxo Bank

My only call (since Q4-2013) remains that global yields (G10) drop to all-time lows – and in this final phase will be lead to the US 10-year going to 1.5% and the 30-year to 2.5%. This creates a derivative trade which is that the US dollar's strength is about to top. There is a significant possibility of the US dollar retesting recent highs.

However, central banks, the momentum of the US economy, disinflation trends and a global geopolitical environment which sees the US lose power week by week, are all signs, although still early, of changes to the outlook. The world – growth-wise – does not work with a strong US dollar. Asia is linked and is suffering…

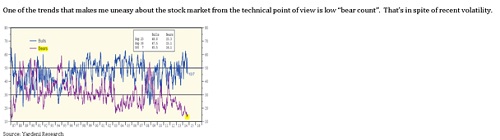

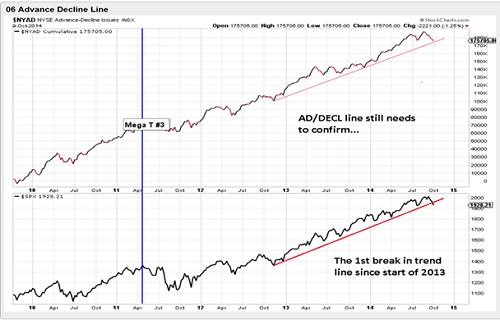

4. It’s often “too easy” to find negative charts after big down move, but I think these three represent more than a day or two of sell-offs…

Below, from Daily Shot: