KPMG Global Economic Outlook: Commodity prices counteract impact of rising inflation & slowing growth in South Africa

• Russia-Ukraine war to lower global growth prospects and increase inflationary pressures

• Central banks’ change in policy stance could add to markets’ volatility

• On-going geopolitical uncertainties could see further disruptions to production and trade

KPMG GLOBAL ECONOMIC OUTLOOK H1’2022

The on-going conflict in Ukraine is set to lower global growth prospects and increase inflationary pressures across the world, according to the latest KPMG Global Economic Outlook.

The bi-annual report provides economic forecasts and analysis from the global organisation’s team of economists in territories and regions throughout the world – including South Africa.

The latest edition, covering H1’2022, warns progress on global issues including public health and climate change has slowed as political and business leaders grapple with the broad implications of the war in Ukraine.

While Russia and Ukraine together represent a relatively small part of the world economy, both countries account for a large share of global energy exports, as well as exports of a range of metals, food staples and agricultural inputs. Together, Russia and Ukraine account for almost a third of global wheat exports.

Inflation on a high exacerbates central banks’ dilemma

The global economy emerged from the COVID-19 recession with higher public debt and as central banks raise interest rates, the servicing cost of sovereign debt also increases, making it particularly challenging for emerging countries whose debt is denominated in an appreciating US dollar. With policymakers and many businesses still reeling from the consequences of the pandemic, they are less ready to counter another significant economic shock.

Frank Blackmore, Lead Economist at KPMG South Africa, said:

“South Africa is in a unique position having profited from the rise in commodity prices caused initially by COVID-19 supply disruptions and as a consequence of the conflict in Ukraine, Similarly, we have seen an increase in commodity prices improving South Africa’s terms of trade (export prices over import prices) and relatively large surpluses on the current account in 2020 and 2021.This surplus has also underpinned a relatively resilient local currency and will also contribute to GDP growth in 2022 – set to grow by 2% led by the finance, real estate and business services sector, and growth in personal services as well as mining, agriculture and trade, catering and accommodation.”

“The positive balance on the current account resulting from the increased value of commodity exports, although being supportive of the rand, is not large enough to shield South Africa from inflationary increases with inflationary pressures for 2022 set to increase and remain cost push in nature due to increasing energy prices, as well as food prices caused by ongoing supply chain disruptions. The global increase in commodity prices, including oil, has meant South Africa is facing rising imported fuel and food production costs. As a consequence, the headline consumer inflation rate is expected to increase towards the upper boundary of the central bank’s inflation targeting range of 3% to 6% in 2022 before moving back towards the midpoint of the targeting range in 2023.”

Global growth outlook

The outlook for the next two years will depend on how the conflict between Russia and Ukraine evolves. With so much uncertainty at present, KPMG’s Global Economic Outlook has developed three scenarios to examine the prospects for the world economy:

• The main scenario assumes that world oil prices will be US$30 higher than their path prior to the escalation of the crisis, while gas prices will be 50% higher across Europe. It also incorporates a 5% rise in global food prices.

• A more severe scenario looks at the potential impact with world oil prices US$40 higher together with a 100% rise in gas prices for Europe and 50% rise in gas prices for the rest of the world. This downside scenario also assumes a 10% rise in global food prices. Both scenarios incorporate a 23% rise in average metal prices and a 4% increase in the cost of agricultural inputs. They also include higher investment risk premia and additional government spending in Europe.

• The report’s upside scenario looks at the possible outcome should the conflict resolve sooner than anticipated, with prices returning to early February levels and production and trade flows restored.

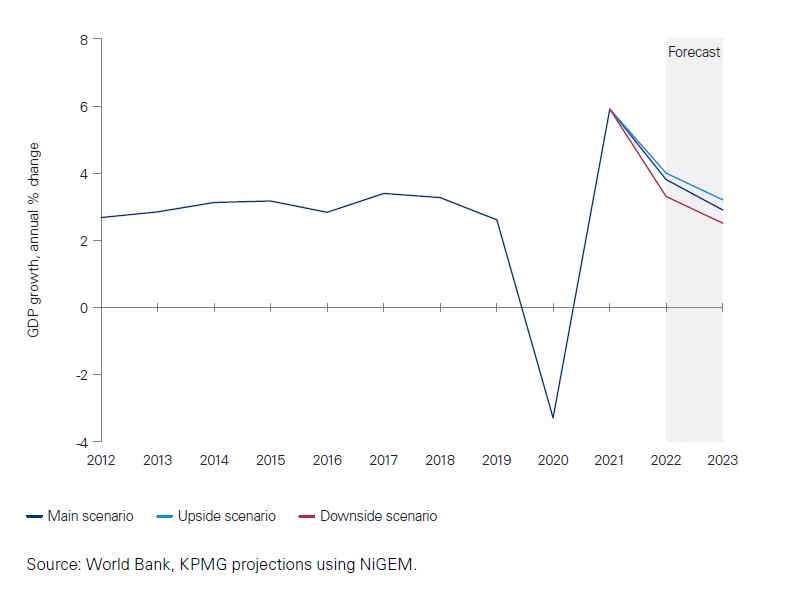

Chart: World GDP group under three scenarios

The report’s analysis found that global GDP growth could range between 3.3%-4% this year and between 2.5%-3.2% in 2023, depending on the scenario. Risks to KPMG’s forecast are currently skewed to the downside.

“However, in South Africa the forecast is much lower with a 1.8% growth in 2023 and a possible convergence back to the average pre-COVID-19 level of 1.7%. This driven by insufficient tangible policy action to increase the lower investment and consumption spending caused by a reaction to a number of governance challenges including ongoing policy uncertainty, corruption, aging infrastructure and continued power shortages, the absence of growth stimulating policy interventions and inadequate levels of service delivery,” continues Blackmore.

It is possible to envisage that the conflict between Russia and Ukraine escalates beyond the report’s downside scenario, with cuts to energy supplies for example causing a significant disruption to production in parts of Europe. The COVID-19 pandemic is still causing shutdowns in major economies such as China, and a new wave could undo the progress in easing global supply chain blockages.

Gary Reader, Global Head of Clients and Markets at KPMG, commented:

“Before the outbreak of war in Ukraine, different territories and regions were at different stages of their post-COVID-19 economic recovery, and that is reflected in the analysis from our Chief Economists. But, while GDP forecasting varies, there are a number of clear, consistent themes and threats facing the planet. Armed conflict may currently be restricted to Eastern Europe, but it’s already having far-reaching consequences for all nations.

“Supply chain issues have moved from a post-covid issue to a major immediate threat, with potential shortages in natural gas, metals and grains, among many others. While shortages will impact every territory, we anticipate a disproportionate impact on some of the world’s poorest places and people, compounding long-term challenges for the planet’s collective recovery. Meanwhile, inflation looks set to become a major theme for everyone, raising the threat of a worldwide cost-of-living crisis. Economic forecasting is not a perfect science, but what KPMG’s Global Economic Outlook does do is shine a light on the path ahead, providing a degree of guidance in an increasingly difficult journey.”

Click here to read more...