Inflationary pressures building but no further rate increases necessary

CPIX declined slightly from 6.5% in July to 6.3% in August but remains above the upper target level of 6%. However, even though the economy will be confronted with huge inflationary pressures over the next 10 months, interest rates should not be increased further, says prof. Chris Harmse, chief economist of Dynamic Wealth.

Harmse highlights three main reasons for this viewpoint.

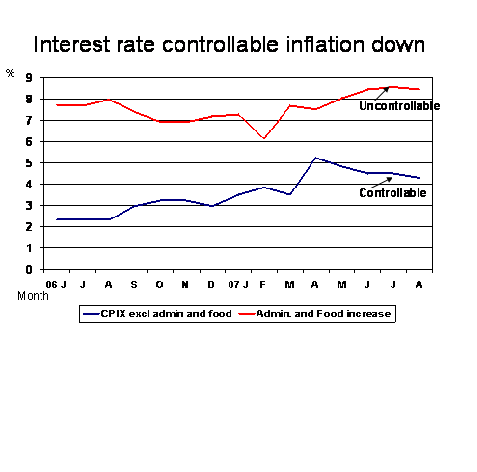

Firstly, the price increases which can be controlled by the South African Reserve Bank via interest rates peaked in April this year and seem to be on a downward trend. On the other hand, those prices which are not directly affected by rate increases are increasing at a steep rate.

He points out that food and administered price increases are mainly beyond the control of interest rates. These two items, which comprise about 45% of the CPIX basket, are mainly driven by external factors such as droughts, capacity constraints and government decisions (administered prices). The increase in these two uncontrollable price categories was 8.4% (y o y) in August, slightly down from 8.6% in July (see graph below). The main reason for this slower increase can be attributed to declining petrol prices in the transport price category.

| INDICATOR | Aug 07 | Jul 07 | Jul 07 | Jun 07 |

| Aug 07 | Jul 07 | |||

| CPIX | 6.30% | 6.50% | 0.30% | 1.10% |

| CPIX excluding food and administered prices | 4.3 | 4.50% | -0.05% | 0.25% |

| CPIX for food and administered prices | 8.4 | 8.60% | 0.72% | 2.06% |

| Core inflation (metropolitan areas) | 5.10% | 5.60% | 0.10% | 0.90% |

In contrast, prices that can be influenced by interest rates peaked at 5.2% in April and had been on a downward trend to 4.3% in August. These demand driven prices, which comprise about 55% of the basket, are not expected to increase at much higher rates in the future - even though input costs such as higher wages still need to filter through to retail prices. A slowdown in household demand (from 7.4% in Q1 to 5.5% in Q2), as well as in total domestic spending (from 5.8% in Q1 to 1.1% in Q2) will limit the extent of the price increases.

The second reason is that it takes 18 to 24 months for interest rates to have its maximum impact on prices. As a result time is needed for interest rates to work. The slowdown in spending especially on durable goods (shrunk 10% in Q2 from Q1) is signaling that the interest rate medicine is working and that time is needed for the patient to recover.

Thirdly, the Reserve Bank cant fight inflation alone. The government and labour unions also need to play their respective parts. For example, municipal tariff increases way above the level of 6% are not of assistance in the fight against inflation. The sharp increases in budget expenditure, whilst the Reserve Bank is trying to curb demand, are also not of any assistance. In addition, labour unions also need to focus on productivity growth during wage negations in order to lower unit labour cost increases.

Harmse says whilst CPIX will peak at above 7% early next year, the Reserve Bank already did what it could to limit price increases. Any further rate increases will be an overkill and overcompensate for increases that cant be controlled by rate increases.