Higher food prices push headline CPI above 6%

Sanisha Packirisamy, Economist at MMI Holdings.

Herman van Papendorp, Head of macro research at MMI Holdings.

Headline inflation surprises to the upside after a lengthy period of undershooting expectations.

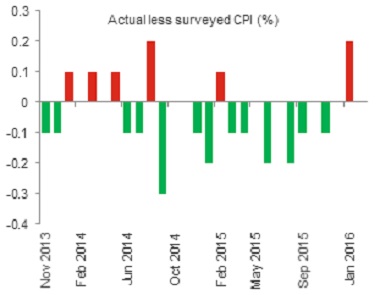

Stats SA reported an increase in headline consumer price inflation (CPI) from a mild 5.2 % y/y print in December 2015 to a more threatening 6.2% y/y in January 2016. Despite having surprised to the downside (or meeting expectations) for the past ten months, headline inflation printed higher than expected in January, at 0.2% above the consensus forecast for a 6.0% y/y increase (see chart 1).

Chart 1: Headline CPI shoots above market expectations

Source: Stats SA, Bloomberg, Momentum Investments

January is traditionally a relatively high survey month, with over a quarter of the basket surveyed in addition to the normal monthly surveys. Relative to our own forecasts, the price increases related to food, beverages, vehicles, restaurants and funeral expenses surprised to the upside.

Higher food inflation materialising

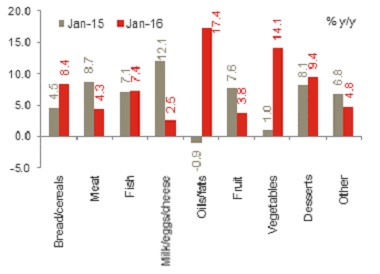

After months of surprising to the downside, higher food price pressures are finally emerging in the consumer inflation basket. Food inflation surged by a higher than anticipated 2% m/m in January, leaving the year-on-year rate at 7.1% y/y, exceeding the upper end of the 3% to 6% inflation target band for the first time in eleven months.

Six provinces in SA have been declared as drought disaster areas. The lowest rainfall experienced in 100 years has affected maize, wheat and sugar crops most severely, while also having a negative impact on oil seed and vegetable crops. Given that yellow maize and soybean are vital to animal feed, beef, lamb and chicken prices are also likely to come under pressure in upcoming months, particularly as farmers begin to rebuild their herds following excessive culling during the severe drought conditions which have temporarily suppressed meat prices (4.3% y/y in January).

Chart 2 suggests that the price increase in maize and wheat (in rand terms) has started to filter through into higher bread and cereal costs (8.4% y/y) while oils/fats (oil seed), vegetable and dessert (sugar) prices have shot up to 17.4% y/y and 14.1% y/y, respectively.

Chart 2: Drought-inflicted food price increases

Source: Stats SA, Global Insight, Momentum Investments

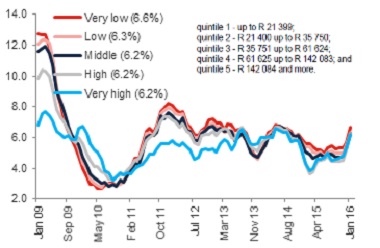

The producer price inflation (PPI) figures suggest that grain mill and sugar-related foods will continue to experience upward price pressure. Meanwhile, PPI data point to relatively low inflation in meat and dairy products in the short term. As the oversupply in meat products work their way out of the system and as farmers begin to rebuild herds, meat inflation (which accounts for a third of the consumer food inflation basket) is expected to build in later months, leaving food inflation as a key contributor to rising headline CPI this year. With food comprising a larger share of the lower-income households’ consumer basket, rising headline inflation could become more of a problem for these households. During the first six months of 2009, when food inflation averaged 13.7% y/y, we saw a major divergence in consumer inflation rates between the various income-earning groups (see chart 3). During this period, headline inflation peaked at 12.7% for those in quintile 1 (classified as those earning <R21 399 p.a.), while only peaking at 7.5% y/y for those in quintile 5 (classified as those earning >R142 084 p.a.).

Chart 3: Inflation rates per income group (% y/y)

Source: Stats SA, Global Insight, Momentum Investments

Beverage prices also surprised to the upside, most notably non-alcoholic beverages which increased by 2.7% m/m (7.1% y/y). According to Morgan Stanley, the increase likely arose from a steep 2.9% m/m increase in beer prices which could have been related to the sharp increase in grain prices.

On track to a sizeable over-recovery in fuel prices in March

Petrol prices declined by 3c/l in January, but were hiked by 6c/l in February. The current over-recovery suggests that petrol prices could be cut by a sizeable 57c/l in March (-3.7% m/m) keeping a lid on year-on-year inflation in the private transport category in the near term.

However, with rising fiscal pressures, Treasury could take advantage of low international oil prices and increase the general fuel and Road Accident Fund (RAF) levies in an effort to bolster revenue collections. Government implemented a steep 30.5c/l hike in the general fuel levy and a 50c/l increase in the Road Accident Fund (RAF) levy in the February 2015 national budget. Fuel levies have increased by 16.4% y/y on a fiscal YTD basis relative to Treasury’s 14.9% y/y full-year target set in February 2015 and have come in marginally higher than the revised 16.2% y/y target in October 2015.

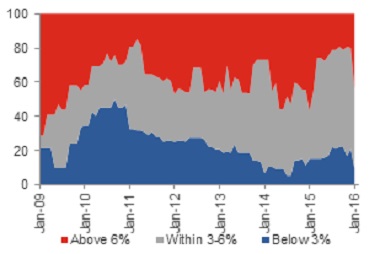

Higher proportion of the basket printing price increases in excess of 6%

There was a notable jump in the proportion of the consumer basket printing in excess of 6% y/y from 19.8% in December 2015 to 43.8% of the basket in January 2016 (see chart 4). This was largely due to year-on-year inflation exceeding 6% in the food, private transport and financial services (mostly bank charges) in January. Meanwhile, price increases in categories including water, electricity, education, medical services, insurance and alcoholic beverages remained stubbornly above 6%.

Chart 4: Nearly 44% of the CPI basket is printing above the 6% upper target

Source: Global Insight, Momentum Investments

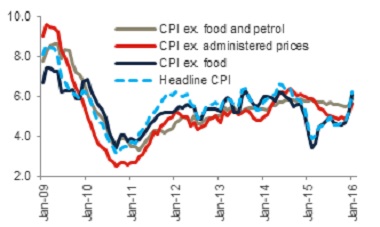

Uptick in core inflation suggests upward pressure present outside of food prices

Core inflation (headline CPI excluding food and petrol) increased to 5.9% y/y in January from 5.6% y/y the month before (see chart 5). Administered price increases are partly to blame for the rise in core inflation. According to Stats SA, administered price inflation rose to 8.8% y/y in January, with regulated administered prices registering at an even higher 9.0% y/y over the corresponding period.

Chart 5: Measures of headline and core inflation (% y/y)

Source: Global Insight, Momentum Investments

Rising inflation pressures point to further interest rate hikes

Despite elevated global food stocks keeping international food prices more than 10% lower than where they were a year ago, unfavourable domestic weather conditions and a weaker currency have driven domestic food prices higher. Elevated administered price increases, the potential for an additional steep hike in electricity prices and the rising threat of second-round inflation point to headline CPI increasing close to c.6.5% y/y in 2016 from 4.6% y/y in 2015.

A sharp sell-off in the currency on a trade-weighted basis and above-inflation wage settlements have further led to stubbornly high (and rising) inflation expectations by the price setters of the economy, namely businesses and trade unions. The South African Reserve Bank (SARB) noted that they will remain focused on the evolution of inflation expectations and will pay close attention to any indications of second-round effects of the exogenous shocks to inflation. The uptick in core inflation in recent inflation prints could suggest the possible emergence of such second-round inflation pressures.

In addition to a rising inflation trajectory and the threat of second-round inflation pressures, a still-elevated current account deficit raises concerns over funding given our reliance on volatile portfolio flows. The need for positive real interest rates further points to the likelihood of additional interest rate rises to the order of 75 basis points by the end of 2017. We expect these to be increasingly front-end loaded in the event of a material deterioration in survey-based inflation expectations, relative to the 4Q15 survey which was conducted by the Bureau of Economic Research just prior to the sharp December sell-off in the currency.