Headwinds and tailwinds

The US equity market has not seen a 10% correction since 2011, leaving many to feel that it is vulnerable to a sell-off. When and how a correction will happen cannot be forecasted with any accuracy, and there are many factors that could cause a sell-off in the short term (for instance an oil price spike if the turmoil in Iraq escalates greatly). Rather than trying to time the market, investors are better off focusing on valuations, having a long-term view and trying to understand the underlying drivers of market performance.

Factors supporting the rally

Since 2009, US equities have had a number of broad tailwinds. These include, firstly, the fact that after the crash, shares were cheap. Secondly, there was modest top-line growth (revenue growth) as the US economy improved gradually while several emerging markets continued growing well. Thirdly, and probably most importantly, was robust bottom-line (profit) growth as companies were able to slash labour costs and increase margins to record levels. Low interest rates also made it cheap for firms to buy back large quantities of their own shares, boosting earnings per shares (EPS) growth. Companies also sat on record cash piles. According to a report in the Financial Times, US share buybacks and dividend payments climbed to a record level of $241billion in the first quarter of 2014, as companies chose to boost shareholder returns (though it has to be pointed out that the previous record of $233billion was set in the third quarter of 2007, which was pretty much at the top of the cycle, thus destroying shareholder value).

Over this period, there have also been several headwinds, leading to “risk-off” periods, particularly with regards to the severe cutback in US government spending and several episodes of political uncertainty surrounding government spending (such as the fiscal cliff, the US downgrade and the debt ceiling). There were also fears of a double-dip recession in the US (Europe and Japan did experience double-dip recessions). Since 2009, large numbers of individual and institutional investors were net sellers of equities despite the rally.

Looking ahead, some tailwinds could become headwinds. US equities are no longer very cheap compared to history, but still cheap compared to bonds. Corporate margins can narrow, though not necessarily by much as labour’s share of national income is structurally depressed by competition from technology and the global pool of cheap labour.

These headwinds could be offset by other tailwinds, including mergers and acquisitions activity and capital expenditure. These are two different ways for companies to grow revenues, by buying competitors or by expanding the firm’s own capacity or enhancing its productivity. Companies sit on large piles of cash so they can afford to ? (as is evidenced on the large amounts currently spent on share buybacks). Capital expenditure in particular remains very low compared to past cycles, and could support future economic growth. Mergers and acquisitions can also keep margins high due to cost savings, but the promised cost savings or “synergies” often fail to materialise.

Future path of interest rates crucial

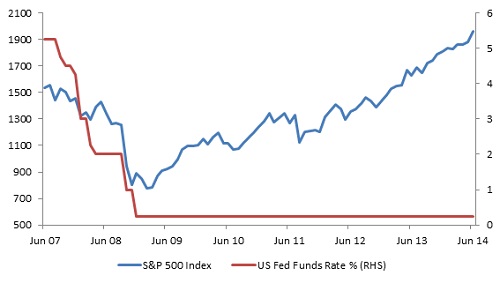

Key to the rally is the future path of interest rates, as premature interest rate hikes could do some serious economic damage. The market currently expects the first hike in the Fed funds rate to occur in the third quarter of 2015. This is in line with the Federal Reserve’s own current thinking and guidance. However, headline inflation in the US has now risen to 2%, which could start putting pressure on the Federal Reserve. There is an increasing concern in central bank circles that certain asset prices might be in bubble territory. Unemployment is also falling rapidly. However, both headline unemployment and inflation numbers hide underlying economic weakness in the US economy, which is expected to grow around 2% over the medium term. While last week’s policy meeting resulted in the Fed cutting back its bond-buying programme by another $10 billion to $35 billion a month, the Fed remains committed to accommodative policy, which is good. But if the Fed (or other major central banks) loses its nerve and hikes unexpectedly, early or harshly, the market could be hit hard.

If the US sneezes...

The US equity market usually sets the tone for global markets. The JSE has avoided bear-markets even during local economic downswings when the US market has performed well. While anything could happen in the short term and volatility could pick up, the rally still appears to have legs.

Chart 1: US equities and interest rates (Source: Datastream)

-----------------------------------------------------------------------------------------------------------------------------------------

Finally, a positive surprise

Last week was remarkably busy on the local economic data front. Statistics SA announced that consumer inflation rose to 6.6% year-on-year in May, from 6.1% in April. This was slightly above market expectations. Month-on-month, CPI was 0.2% higher.

Food inflation up, but core inflation steady

The biggest contributor to the sharp increase in annual inflation was higher food inflation. Prices of food and non-alcoholic beverages rose 8.8% year-on-year in May, up from 7.8% in April. Vegetable prices climbed, by 2.3% month-on-month and 13% year-on-year. Bread and cereal prices rose by 10.2% year-on-year in May, but price increases should moderate as the sharp drop in maize prices at the producer level start filtering through. Petrol inflation was also a big contributor.

Core inflation remained steady at 5.5%, indicating that the ‘second round’ effect of a weak rand, i.e. firms passing their currency driven cost increases on to consumers remains limited (but present nonetheless). Inflation expectations also remain well anchored.

Inflation is now well above the upper end of the SA Reserve Bank (SARB) target range, but probably still in line with its forecast. SARB indicated that rates will continue rising, but probably gradually given the weakness of the economy. The future path of the rand exchange rate remains key, while SARB will also keep a close eye on the impact of political turmoil in the Middle-East on global oil prices.

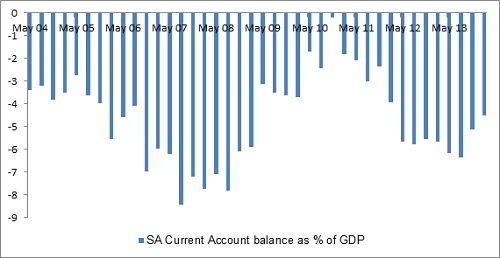

Current account surprises

SARB also released a whole range of important data in its Quarterly Bulletin last week. The most closely watched number at the moment is the current account balance. According to SARB, the current account deficit narrowed in the first quarter to R161 billion (4.5% of GDP) from R197 billion (5.1% of GDP) in the fourth quarter. The market expected the deficit to widen to 6.1% of GDP, so this is the first positive surprise the local economy has delivered in a while. The smaller current account deficit was due to an improvement in the services account, with a sizable increase in dividend receipts from abroad, while dividend payments to foreigners fell.

The trade balance, the other important component of the current account, deteriorated significantly in the first quarter to –R75 billion from –R45billion in the fourth quarter of 2013. This is a very disappointing outcome given that one would expect the weak rand to help close the trade deficit. In fact, import volumes rebounded in the first quarter, and increased by 4.4%. Factoring import prices and the impact of the weaker rand, the value of imports rose by 9% in the first quarter. In contrast, export volumes only rose by 2.1%, while export values rose by 7.2% as the boost from a weaker rand was somewhat offset by lower commodity prices. For the current account to continue closing, export growth will need to improve and import growth will have to slow down.

Fixed investment still too slow

The other notable data item in the Bulletin is on fixed investment spending, which is growing too slow. Fixed investment spending is important as it tends to give the economy an immediate boost, but also facilitates future economic activity. Fixed investment rose by 2.6% in the first quarter, down from 3.1% growth in the last quarter of 2013. Fixed investment by the government and parastatal sector increased in the first quarter (a cornerstone of government’s economic policy which has been slow to materialise), but private sector fixed investment growth slowed to 1%. Low levels of business confidence, lack of demand and high levels of excess capacity mean private companies are not investing. Higher levels of fixed investment are necessary to get the economy going.

Outlook not great

The Quarterly Bulletin also contained SARB’s estimates on the impact of the platinum sector strike. Real GDP would probably have grown by 1.6% in the first quarter instead of contracting by 0.6% if the strike did not take place. The current account deficit would have been 4.2%, instead of 4.5% of GDP. Therefore, a resolution in the strike (which we are apparently getting closer to) is important and should help the economy. However, even excluding the impact of the strike, it is clear that the underlying economy is weak and has run out of growth momentum. Consumers face a slow but relentless squeeze on their finances with poor job creation prospects; businesses being reluctant to invest, labour problems and inadequate electricity supply. Fiscal policy is tightening as government tries to close the budget deficit, while monetary policy is constrained by inflation rising above the SARB’s target.

Chart 2: SA current account balance (Source: SARB)