Headline consumer price inflation hits 7%

Sanisha Packirisamy, Economist at MMI Holdings.

Herman van Papendorp, Head of Asset Allocation at Momentum.

Stats SA reported an increase in headline consumer price inflation (CPI) from an already above-target 6.2% y/y print in January 2016 to a more worrisome 7% y/y print in February 2016.

Headline inflation increases to its highest level since May 2009

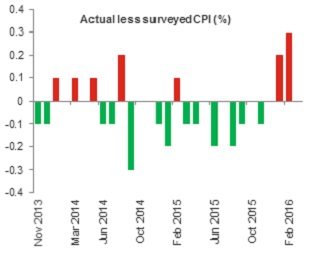

After having surprised to the downside (or meeting expectations) for the most part of 2014 and 2015, the trend in positive inflation surprises reversed in early 2016 with CPI surprising to the upside for the past two months. In February, headline inflation printed higher than anticipated at 0.3% above the consensus forecast for a 6.7% y/y increase (see chart 1).

Chart 1: Headline CPI surges ahead of market expectations

Source: Stats SA, Bloomberg, Momentum Investments

February is usually a relatively low survey month, with only c.12% of the basket surveyed in addition to the normal monthly surveys. Relative to our own forecasts, the price increases related to food (notwithstanding our expectation of higher food costs given the impact of the drought), non-alcoholic beverages, furniture, appliances and hotels surprised to the upside.

Drought impact pushes food inflation higher

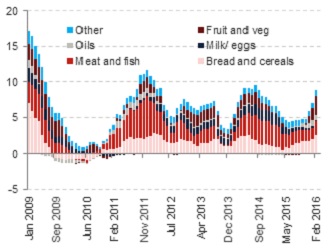

After months of surprising to the downside, higher food price pressures are finally materialising in the consumer inflation basket. Food prices surged by a higher than projected 2.2% m/m in February, leaving the year-on-year rate at 9.1% y/y, exceeding the upper end of the 3% to 6% inflation target band for a third consecutive month.

The impact of the drought has started to filter through into unprocessed food prices. Unprocessed food price inflation reached 10.4% y/y in February, while processed food inflation registered at a lower (but still above target) print of 7.1% y/y. The sharp increase in food prices mostly stemmed from higher bread/cereal (10.6% y/y), vegetable (21.6% y/y), fruit (13.2% y/y) and oils/fats prices (17.8% y/y), see chart 2. Though meat price increases remained contained below 6%, higher feed costs and herd-rebuilding (following increased slaughtering during the drought) are likely to lead to higher meat inflation down the line, keeping food inflation elevated this year.

Chart 2: Contribution to food inflation (% y/y)

Source: Stats SA, Global Insight, Momentum Investments

Sizeable fuel price increase on the horizon

The February inflation print captured a marginal 6c/l hike in petrol prices, but this is likely to reverse by 69c/l in March. The current 43c/l under-recovery (largely owing to the uptick in international oil prices) and a 30c/l fuel tax increase suggest a 73c/l increase in petrol prices next month (April). In year-on-year terms however, private transport inflation (mostly petrol costs) is likely to move significantly lower given the high base created in April last year.

Signs of rising broad-based price pressures

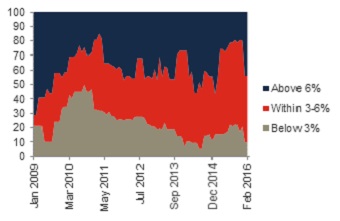

Less than half of the inflation basket has experienced price increases within the 3% - 6% inflation target band. Chart 3 shows that prices of nearly 45% of items in the consumer inflation basket are rising at a faster pace than 6% y/y.

Chart 3: Proportion of CPI basket trading below, within and above the 3% - 6% target band

Source: Global Insight, Momentum Investments

Core inflation inching higher

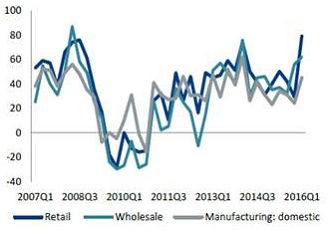

Core inflation (headline CPI excluding food, non-alcoholic beverages, energy and petrol) increased to 5.7% y/y in February from 5.6% y/y in January. Higher food prices have pushed goods inflation to 7.9% y/y in February, while services inflation remains marginally outside the target range at 6.1% y/y. According to the Bureau of Economic Research (BER), underlying survey detail in the manufacturing, retail and wholesale sectors are pointing to a sharp deterioration in the level of average selling prices, indicative of a wider effect of rising prices across the consumer basket (see chart 4).

Chart 4: Net percentage expecting an increase in selling prices

Source: BER

Build up in inflation pressures point to further interest rate hikes

Despite elevated global food stocks keeping international food prices around 10% lower than where they were a year ago, unfavourable domestic weather conditions and a weaker currency have driven domestic food prices nearly 20% higher over the corresponding period. A steeper ramp up in food inflation and increasing evidence of broader-based price pressures, owing to a steep depreciation in the currency on a trade-weighted basis, are indicative of a likely prolonged breach in the headline measure of inflation. While the South African Reserve Bank (SARB) sees inflation exceeding the upper 6% target for the remainder of this year and most of next, we expect the breach to persist for a period of five quarters.

Currency weakness and wage cost pressures have further led to stubbornly high (and rising) inflation expectations by the price setters of the economy, namely businesses and trade unions. The latest BER Inflation Expectations Survey noted the overall measure surveying five-year inflation expectations remaining at 6.1% with the expectation of analysts edging higher to 5.7% from 5.5%. Expectations by businesses and trade unions improved by 0.1% to 6.4% and 6.1%, respectively, but nonetheless remained above the target range. In recent speeches, the SARB noted that they will remain focused on the evolution of inflation expectations and will pay close attention to any indications of second-round effects of the exogenous shocks to inflation. The further uptick in core inflation in recent CPI prints and the result of escalating selling price pressures being noted in the BER sector surveys could suggest the possible emergence of such second-round inflation pressures.

In addition to a rising inflation trajectory (brought forward by a higher than expected increase in price pressures in February) and the threat of second-round inflation pressures, a still-elevated current account deficit raises concerns over funding given our reliance on volatile portfolio flows, which have recorded in negative territory since Nenegate in December 2015. The need for positive real interest rates further points to the likelihood of additional interest rate rises to the order of 50 basis points over the course of the next twelve months.