Government must deliver on Capex promises

The improvement in the FNB/BER building confidence index from 37 in the first quarter of 2013 to 41 in the second half of 2013 was a new four-year high and the first time since 2005 that the index has recorded increases for three successive quarters. However the FNB/BER Civil Confidence Index shed 6 points to 45 in the second half of 2013 after gaining 15 to record 51 in the first quarter of 2013. This still indicates a position of net contraction in both these sectors. “Given the low growth outlook, it is paramount that everything is done to restore confidence and stability in order that the infrastructure thrust can gain traction once again,” says Luke Doig, Senior Economist, Credit Guarantee Insurance Corporation.

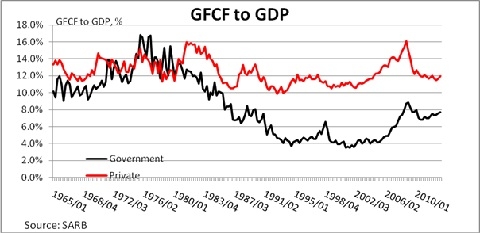

The long-term graph below shows the capex (or Gross Fixed Capital Formation) spend by both the private and government (including parastatals) sectors as a percentage of GDP. In the entire period from 1965 until the mid-1980s, total GFCF spend averaged around a healthy 25% of GDP with levels of 30% being achieved in the mid-70s. However from the mid-80s the levels declined to around 15% over 1992-4. A recovery only took place from 2002 onwards, further reinforced by the country's preparations for the 2010 World Cup. There are a number of economic developments such as the oil crises and global and domestic recessions which obviously impacted on the relative ability of each sector to engage in fixed investment to varying degrees.

Firstly, both the state and the private sector previously contributed towards fixed investment in the economy on roughly equal terms. This changed rapidly in the early 80s when Government's contribution dropped off sharply; similarly so did that of the private sector which was battling to cope with the boom-and-bust economic cycles of the times when two downward phases in the business cycle were experienced.

Secondly, the subsequent gap of around 7% between the two sectors (as a % of GDP) has since narrowed to closer to 4% in recent years as the global crisis took its toll on private sector confidence and willingness to invest.

Thirdly, Government's contribution rate has been edging up since late 2010 as it endeavours to bring to fruition the large number and range of projects under its broad infrastructural thrust. The private sector's contribution rate has broadly tracked sideways close to 12% as it battles poor economic conditions and an environment beset by weak confidence.

Doig comments further, "It is of vital importance that everything possible must be done to stabilise such brittle confidence in order that the private sector's contribution can improve closer to 15%. Government needs to deliver on capex promises and increase its contribution rate closer to 10%, something last seen in 1985. This would then allow for a combined contribution rate of closer to 25% and provide a buffer to the under-pressure contribution of personal consumption spend to the domestic growth cycle. It would also provide opportunities for the numerous job seekers which at this time do not appear to have any alternative hopes. That is why the slowdown in real GFCF spend from 5.7% in calendar 2012 to just 2.5% (saar) in the first quarter of 2013 is most concerning.” The displacement of capex spend by government on current expenditure (salaries) has to be reversed and the run-up to elections next year may see this, although doubts remain. The fragile improvement in building confidence in the second half of 2013 is welcome but this needs to be far stronger before this avenue will provide a boost to overall growth. With GDP expected to average just 1.9% and 2.75% in 2013 and 2014, this is sorely needed.

Credit Guarantee entered the Bonds and Surety Market in May 2012, offering Bid Bonds, Performance Guarantees, Retention Guarantees, Advance Payment Guarantees and Materials off Site Guarantees to the construction industry.

"The SA government's infrastructure drive is intended to jump-start growth, and this will hopefully stimulate the demand for guarantees,” says Rhyna Brand, Manager of Sureties at Credit Guarantee. "The Medium-Term Expenditure Framework has set aside R845 billion for public sector infrastructure projects with a further R3.2 trillion in infrastructure projects under consideration up to 2020. This means R250 billion spend per year, about R100 billion more than the average spent during the past five years.”

The Minister of Public Works has stressed the need for private/public partnerships in order to ensure the successful implementation of government's planned Strategic Infrastructure Projects over the next 20 years. These projects include power stations, new mines, additional railways, a new Coega refinery, upgrading of schools and hospitals, and numerous infrastructure and maintenance projects. The government is working on a PICC (Presidential Infrastructure Coordinating Committee) rollout which will focus on long term strategic integrated projects.

"We issue guarantees to employers/beneficiaries such as Eskom Holdings SOC Limited, Transnet SOC Limited, the Department of Public Works, SANRAL and various municipalities among others, continues Brand. "We also offer Electricity Supply Guarantees, Customs Bonds and Liquidator Bonds.

South Africa has a high level of Renewable Energy potential and presently has set a target of 10 000 GWh of Renewable Energy. 3 725 MW to be generated from Renewable Energy sources is required to ensure the continued uninterrupted supply of electricity; this is broadly in accordance with the capacity allocated to Renewable Energy generation in IRP 2010-2030. This IPP Procurement Programme has been designed to contribute towards the target of 3 725 megawatts and towards socio-economic and environmentally sustainable growth, as well as to start and stimulate the renewable industry in South Africa.

"Because of this renewable energy target, we have seen a number of applicants during the past 12 months applying for bonds in this arena. As a bond provider, we participated in some of these solar and wind farm projects,” concludes Brand.