Fuel price cut dampens August 2015 CPI print

Sanisha Packirisamy, Economist at MMI Holdings Investments and Savings.

Headline inflation surprised the market yet again to the downside, printing at 4.6% y/y in August from 5.0% y/y in July.

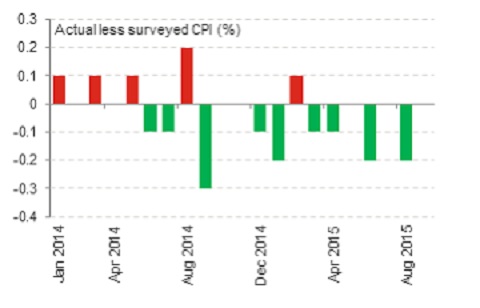

Another downside surprise on headline inflation

This was c.0.2% lower than the Bloomberg consensus figure, but broadly in line with our own forecast for August. Despite the rand depreciating against the US dollar by an average c.1.5% per month over the past twelve months, inflation surprises have largely been to the downside (see chart 1). The lower pass-through can partly be explained by muted domestic demand as well as the more limited depreciation on a trade-weighted basis, until more recently where the rand has sold off on a broader scale.

Chart 1: Inflation has largely surprised to the downside for the past year

Source: Stats SA, Global Insight, Momentum

Inflation was unchanged on the month as an increase in food and non-alcoholic beverage prices largely offset a decline in petrol prices. Moreover, August is a relatively low surveyed month with only an additional c.18% of the basket being surveyed on top of the regular monthly surveys. Following an extended delay, food price inflation has eventually ticked higher by a sharp 0.8% m/m increase in August. Elevated rand-maize prices (caused by poor weather conditions earlier this year) are expected to feed into higher meat prices which should push food inflation higher over upcoming months.

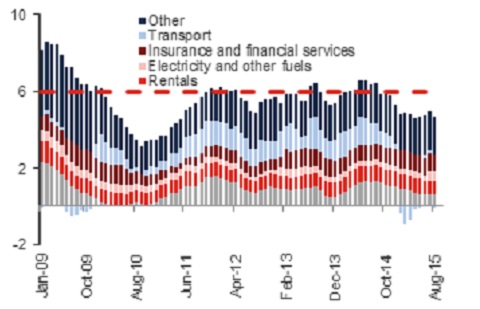

Prices in the transport component fell by 1.1% over the month and by 0.7% relative to August 2014, detracting from overall headline inflation (see chart 2). This was largely due to the 51c/l cut in the petrol price, while a further 69c/l cut should provide further reprieve in September. Recent unfavourable movements on the rand price of oil over the past few weeks have nonetheless led to a marginal under-recovery for October. A steeper fall in transport costs was prevented by the 0.7% m/m (+3.9% y/y) increase in vehicle prices. It should however be noted that the price of new vehicles has been steadily declining in year-on-year terms from a peak of 7.9% y/y in January 2015 to 5.0% y/y in August 2015. According to the National Association of Automobile Manufacturers of South Africa (Naamsa), “intense competition in the increasingly difficult trading environment continued to put pressure on margins throughout the domestic automotive value chain” likely limiting exchange rate pass through in recent months. Used vehicle prices continued to fall, declining by over 8% y/y in August, further reflecting weak consumer demand.

Chart 2: Contribution to headline inflation

Source: Stats SA, Global Insight, Momentum

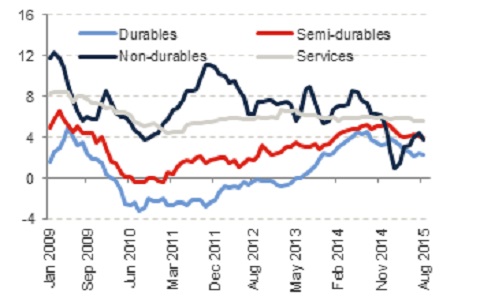

Sticky services inflation

Despite continued rand weakness against the US dollar, as well as on a trade-weighted basis more recently, goods inflation remained reasonably benign at 3.6% y/y while services inflation stayed sticky at 5.6% y/y (see chart 3). Durable goods edged higher by 0.7% m/m largely owing to a 0.7% uptick in vehicle prices, a 0.4% rise in furniture prices and a 0.7% increase in prices of household appliances. Meanwhile, in year-on-year terms, durable goods inflation remained below the bottom-end of the inflation target band at 2.4% y/y.

Chart 3: Services inflation remains elevated (% y/y)

Source: Global Insight, Momentum

Core measures of inflation ticked lower in August with the CPI ex-food and petrol measure declining to 5.6% y/y in August from 5.7% y/y in July. CPI ex-administered prices (where administered prices account for electricity costs, municipal charges, fuel and school fees) steadied in August at 5.0% y/y.

Expected rise in inflation close to 6% next year suggests further interest rate hikes are necessary

A dip in international oil prices aided a move lower in headline inflation in both July and August and have since stabilised around USD48/bbl as elevated inventory levels and weak demand prevent a faster acceleration in prices. Similarly, downward pressure on commodity prices has also had an impact on international food prices which are around 9% weaker than levels seen this time last year. Nevertheless, the favourable impact of lower international commodity prices has partly been eroded by a weaker domestic exchange rate. Since the Monetary Policy Committee (MPC) meeting in July, the rand has sold off by 10.2% against the euro and by 8.3% against the US dollar. Although a still-negative output gap has depressed demand-pull inflation pressures and has limited the pass-through of a weaker exchange rate, above-inflation wage settlements, steep administered price increases and higher rand-food prices point to higher rates of headline inflation in upcoming months, leaving the average expected rate in 2016 close to 6%.

Moreover, longer-dated inflation expectations of businesses and trade unions, in particular, remain stubbornly high at the top end of the inflation target band posing a threat to second-round inflation pressures. While we expect a further modest deceleration in underlying measures of inflation, we do not see core CPI breaching the mid-point of the target band and in fact see renewed pressure building in core inflation by 2H16.

That said, a smaller-than-anticipated print on the current account (due to import compression and robust exports) and dominating negative news flow around suppressed business and consumer confidence, prompting further growth downgrades, are more likely than not to keep the Reserve Bank’s hand steady at the upcoming MPC meeting. Nevertheless, an expected widening in SA’s current account deficit in the remainder of the year, sticky inflation expectations and an anticipated rise in inflation close to 6% in 2016 argues for a further interest rate hike of 25 basis points before year end (next MPC decision meeting to be held on the 19th of November) and a further 50 basis points over the course of next year. This would take the repo rate to a level of 6.75% and real rates into mildly positive territory by the end of 2016.