Four in ten across 28 countries expect their disposable income to fall over the next year

New polling by Ipsos across 28 countries finds that in many markets the public expect recent cost of living pressures to continue.

Key findings

• A Global Country Average of 40% say they expect their disposable income to fall over the year, while 25% expect it to increase

• Three quarters of the public in 28 countries are concerned about the rising cost of goods and services in the next six months

• Public reactions to rises in the cost of living remain focused on cutting spending on luxuries and delaying big purchase decisions

• The state of the global economy is seen as the biggest driver of rising costs, followed by the impact of the Russian invasion of Ukraine and the policies of national governments

A Global Country Average of 40% say they expect their disposable income to fall over the next year. This is larger than the proportion who expect their disposable income to stay the same (31%) or increase (22%).

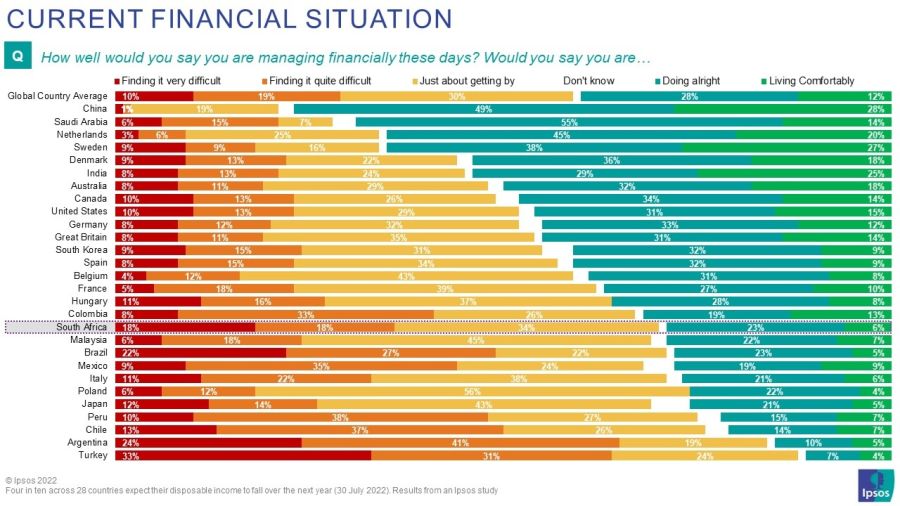

Expectation of falling incomes is highest in Turkey (58%), France (55%), Great Britain (54%) and Hungary (50%), where at least half agree this will be the case. By contrast, the countries who are most optimistic about their disposable income rising are India (48%), Saudi Arabia (42%) and South Africa (40%), although in all three of these countries the sample reflects a more affluent segment of society.

The study also finds those living in Latin America are more likely to report struggling with the cost of living. Across the 28 countries, three in ten report finding it difficult to get by financially (29%) and the same proportion say they are just about getting by (30%). Argentinian citizens are the most likely to be struggling, with two thirds (66%) finding it difficult to get by. While people in Turkey are close behind on 64%, the rest of the top five countries reporting financial challenges are also from Latin America: 51% in Chile, 49% in Brazil and 48% in Peru.

At the other end of the scale, just over one in ten of the global public feel they are living comfortably, including 28% of Chinese citizens and 27% of Swedes.

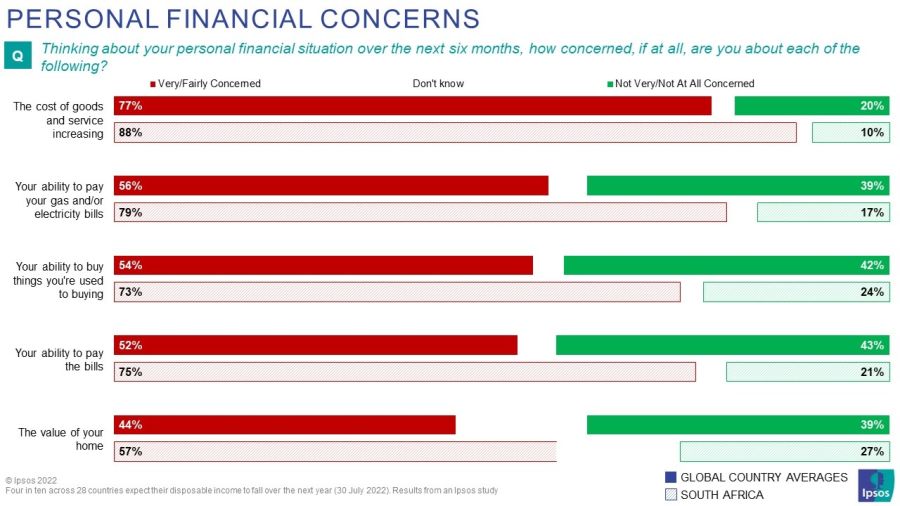

Three quarters of the global public are concerned about the cost of goods and services increasing over the next six months (77%). This includes 91% of Hungarians, 88% of those in South Africa and 86% of Argentines. Even in China where the concern is lowest, 45% say this is a worry over the next half year.

Other areas of significant public concern include:

• 56% are concerned about their ability to pay energy bills: emerging markets top the list with 79% of South Africans and 73% of Indians saying they see this as a concern, followed by Turkey (71%) and Argentina (70%) and Chile (69%). Among established economies, concern about energy bills is highest in Great Britain, where 67% are worried about their ability to pay utility bills.

• 54% worry about their ability to buy the things they are used to buying, led by Turkey (80%), South Africa (73%) and Argentina (69%). The Chinese (28%) and Dutch (33%) are least likely to say they are concerned about this.

There are widespread expectations of further price rises over the next six months.

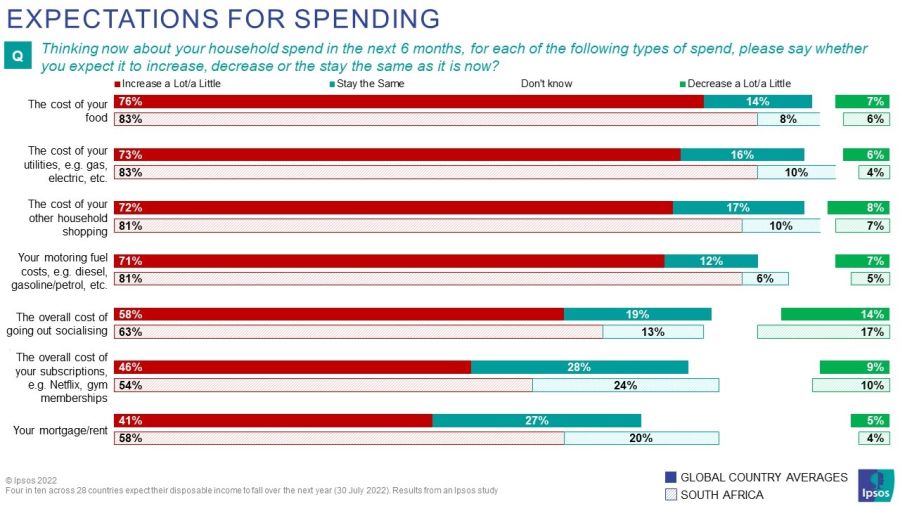

• Three quarters expect the cost of food to rise (76%), including 92% of Hungarians, 89% of Swedes and 88% of Turkish citizens. Just under three quarters expect the cost of other shopping to increase as well (72%).

• A similar proportion expect gas and electricity costs to increase (73%): Turks top the list with 87% expecting this to be the case, followed by Argentines (86%) and Poles (86%). Britons are most likely of any country to say they think the cost of gas and electricity will increase substantially: 65% expect it to increase “a lot” over the next six months.

• Seven in ten (71%) expect motoring fuel costs to increase. This is a particular concern in Chile and Korea where it is seen as the area where price rises are most likely. But the countries where the largest proportion say they expect an increase in fuel costs are Turkey (84%), Argentina (83%) and Poland (81%).

Public expectations of price rises are highest in the most impactful categories. Six in ten say that price rises in food shopping would have the most negative impact on their quality of life, followed by 51% who say the same about the cost of utilities and 42% who say rising fuel prices would have the biggest effect.

How might consumers react?

Potential consumer actions remain focused on cutting discretionary spending. In the face of rising costs which make their normal lifestyle unaffordable, almost half say they would spend less money on socialising (46%) and a similar proportion say they would delay large purchase decisions (44%). Over a third of people say they will spend less on holidays and other household shopping (37% and 36%)

Actions which focus on changing behaviour are less likely: three in ten say that in the face of rising costs they would use less energy or drive less to conserve fuel (both 29%) – although in Great Britain half say they would seek to reduce their energy consumption. A quarter would look to economise on food (26%) and just one in ten would move into cheaper accommodation.

Changes in employment are also less common. Across the 28 countries, just twelve per cent say they would look for higher-paid work with another employer if rising costs made their normal lifestyle unaffordable. Fewer still – eight per cent – say they would ask for a pay rise from their employer in this situation. These views are similar looking only at those in work: among the employed, 12% say they would ask for a pay rise and 18% would look for higher paid work.

What is driving inflation?

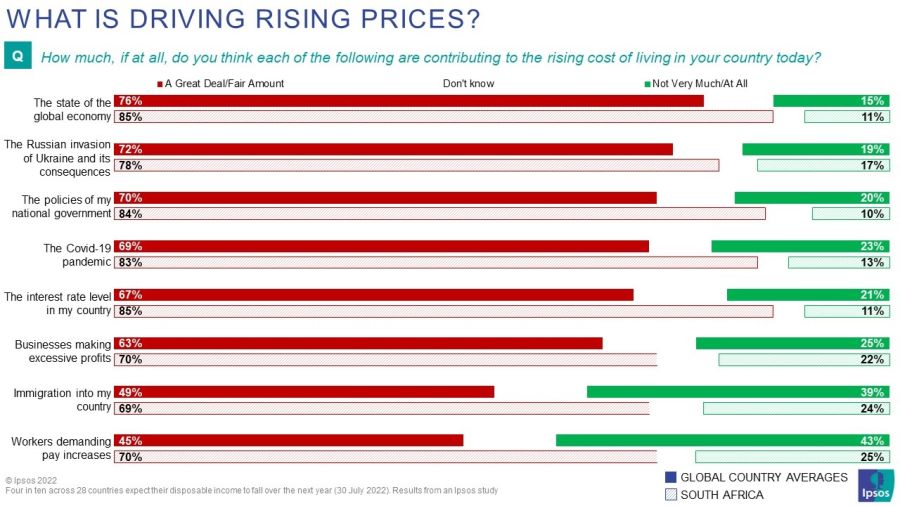

The global public is most likely to view the drivers of recent price rises as being external to their own country. At the Global Country Average level, the state of the global economy is considered the biggest contributor (76%), followed by the consequences of the Russian invasion of Ukraine (72%). However, the policies of the national government come third, on 70% - and it is the biggest driver for those in Argentina, Colombia, Indonesia and Poland.

European countries are more likely to see Russia’s invasion of Ukraine as a contributing factor to inflation: it is ranked as the biggest driver in Belgium, Germany, Denmark, France, Hungary, the Netherlands and Sweden. It is also held as the biggest driver of cost increases in South Korea.

COVID-19 is ranked as the biggest contributor predominantly in Asian countries. Those living in China, Malaysia and Saudi Arabia put it ahead of other factors in having a great deal or a fair amount of a role in driving the rising cost of living, as do people in Brazil.

In Turkey the view is different: Immigration is seen as the biggest driver of cost increases, followed by interest rates and the policies of the national government.

Ben Page, CEO of Ipsos, said:

“Inflation is the biggest worry worldwide and the global public expects things to get worse. And while countries with more recent experience of high inflation such as Turkey and Latin American countries tend to be most pessimistic, European countries and the US are not far behind.

At this point the consumer reaction is still focused on cutting discretionary spending and postponing large purchases, and we know from other Ipsos research that all categories are suffering as people focus on food and fuel. The proportion seeking higher-paid work or asking for a raise from their employer remains comparatively low but if high inflation becomes more than a 2-year phenomenon, we expect this to change”