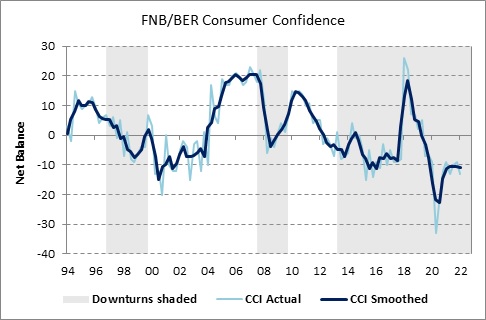

FNB/BER Consumer Confidence Index

Mamello-Matikinca Ngwenya, Chief Economist at FNB

Ukraine knocks consumer confidence

Despite a large drop in coronavirus infections and a welcome easing of COVID-19 regulations since December, the FNB/BER Consumer Confidence Index (CCI) declined from -9 to -13 index points during the first quarter of 2022.[1] Russia’s military invasion of Ukraine, the unfolding humanitarian crisis and the economic ramifications of the war no doubt shook consumer confidence levels around the globe. Domestic consumer sentiment dropped back to -13 index points, the same depressing level that was last recorded in the second quarter of 2021 when the social relief of distress grant was (temporarily) discontinued, the lethal Delta COVID-19 variant surged through SA and lockdown restrictions were drastically tightened (from level 1 to 4) through the quarter. The latest reading remains well below the long-run average CCI reading of +2 since 1994, signalling a low willingness to spend (or increased caution) among consumers.

Details

The slump in the CCI during the first quarter of 2022 can be ascribed to marked (6-point) declines in the economic outlook (from -12 to -18) and household financial position (from +14 to +8) sub-indices of the CCI. Both indices dropped back to levels last seen in 2020. While the index measuring the appropriateness of the present time to buy durable goods (e.g. vehicles, furniture, household appliances and electronic goods) edged up marginally (from -30 to -28), the vast majority of consumers nevertheless still consider the present as an inappropriate time to buy expensive durable goods.

|

19Q4 |

20Q1 |

20Q2 |

20Q3 |

20Q4 |

21Q1 |

21Q2 |

21Q3 |

21Q4 |

22Q1 |

|

|

Overall FNB/BER CCI |

-7 |

-9 |

-33 |

-23 |

-12 |

-9 |

-13 |

-10 |

-9 |

-13 |

|

Economic outlook |

-14 |

-16 |

-21 |

-23 |

-12 |

-5 |

-14 |

-14 |

-12 |

-18 |

|

Household financial outlook |

11 |

14 |

-13 |

-2 |

6 |

10 |

10 |

12 |

14 |

8 |

|

Suitability of the present time to buy durable goods |

-18 |

-26 |

-64 |

-44 |

-30 |

-32 |

-36 |

-29 |

-30 |

-28 |

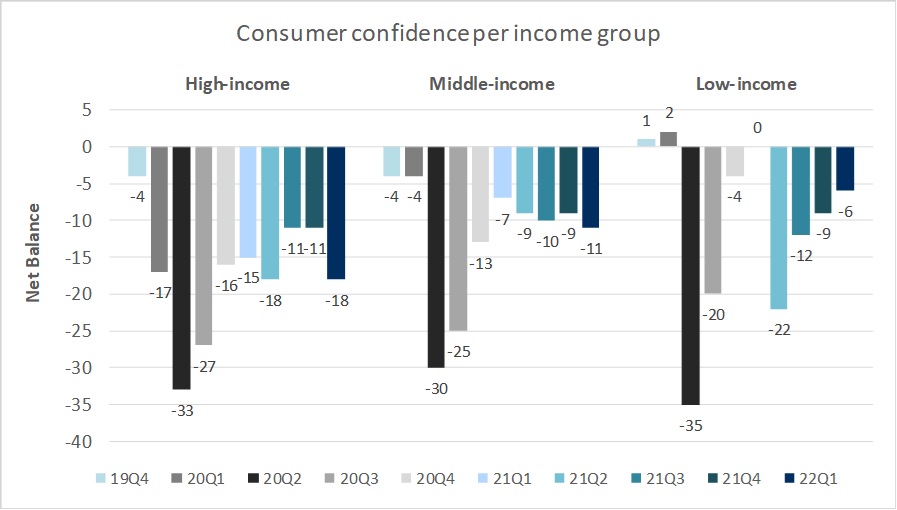

A more detailed breakdown of the CCI shows diverging results across different household income groups. The confidence level of high-income households (earning more than R20 000 per month) declined sharply from -11 to -18 index points, while the confidence level of middle-income households (earning between R2 500 and R20 000 per month) sagged from -9 to -11 index points. However, low-income confidence (consumers earning less than R2 500 per month) further extended its recovery from -9 to -6. Although consumer sentiment remains downbeat across all three income groups, affluent consumers are now considerably more pessimistic about the outlook for the economy and their household finances compared to low-income households.

FNB Chief Economist Mamello Matikinca-Ngwenya said that "The marked decline in the confidence levels of affluent consumers can largely be explained by the alarming images of Russia’s military invasion of Ukraine, unprecedented sanctions against Russia and the unfolding economic ramifications of this conflict. Soaring fuel prices and another 25-basis-point hike in the prime interest rate during the first quarter may also have started to squeeze the spending power of high- and middle-income consumers.”

Skyrocketing international oil prices have already seen the domestic prices of petrol, diesel and paraffin shoot up by around R2 per litre since January, and further massive price hikes are on the cards for April. On top of this, soaring global wheat prices are likely to spill over into higher food inflation, while economists expect another interest rate hike at the end of March – all of which will further increase the cost of living in South Africa.

Mamello Matikinca-Ngwenya noted that “Even though low-income confidence remained seemingly impervious to the economic toll of the war during the first quarter, less affluent households will eventually be the hardest hit by spiralling fuel and food prices, as these categories make up a proportionally larger share of their household budgets compared to that of wealthy consumers.” However, in the meantime, the extension (until March 2023) of the R350-a-month social relief of distress grant to more than 10 million impoverished South Africans announced in the February 2022 national budget likely underpinned the confidence levels of low-income consumers. Furthermore, following more than 2 million job losses since the start of the COVID-19 pandemic, job creation probably turned the corner with the relaxing of COVID-19 regulations and the concomitant uptick in economic activity in recent months, particularly in the employment-intensive services sector.

Bottom line

By the end of 2021, the CCI had recovered most of the ground lost since the outbreak of the COVID-19 pandemic, albeit that consumer sentiment remained pessimistic (with a reading of -9 during the fourth quarter of 2021, compared to -7 in the fourth quarter of 2019). Real consumer spending also rebounded nicely during the fourth quarter of 2021 and incoming survey data suggests that the household sector extended its recovery during the first quarter, with consumer spending on services in particular now resurging (e.g. hospitality, transport and medical services). Positive developments that should boost economic growth and job creation even further include more optimistic fiscal projections (e.g. lower budget deficits and increased government spending) and a significant easing of COVID-19 regulations – such as shorter isolation periods (and no isolation for the asymptomatic) and the proposed lifting of COVID-19 testing requirements for fully vaccinated inbound tourists.

Discouragingly, however, Russia’s war on Ukraine and the ensuant inflationary pressures and deterioration in the global economic outlook have now triggered fresh concerns among South African consumers. Matikinca-Ngwenya explained that “Falling consumer confidence levels signal a decreased willingness to spend among households, while higher inflation will also erode their purchasing power, or ability to spend.” Even though affluent consumers were the first to become alarmed about South Africa’s economic prospects and downwardly revise the outlook for their household finances, less affluent consumers will eventually have to make the largest adjustments to their budgets. “Discretionary spending will come under strain as the prices of necessities such as food and fuel scale new record highs and interest rates continue to edge up, calling for downward revisions to real consumer spending projections for 2022,” said Matikinca-Ngwenya.

Background

Consumer confidence surveys provide regular assessments of consumer attitudes and expectations and are used to evaluate economic trends and prospects. The surveys are designed to explore why changes in consumer expectations occur and how these changes influence consumer spending and saving decisions.

The FNB/BER CCI combines the results of three questions posed to adults in South Africa, namely the expected performance of the economy, the expected financial position of households and the rating of the appropriateness of the present time to buy durable goods, such as furniture, appliances and electronic equipment.

Until the second quarter of 2019, the FNB/BER CCI was based on face-to-face interviews of between 2 000 and 2 500 urban adults. The BER switched to telephone call surveys in the third quarter of 2019. The 500 respondents are representative of the racial and household income composition of the urban adult population of South Africa. Internationally, the majority of CCIs is based on telephone call surveys.

Consumer confidence is expressed as a net balance. The net balance is derived as the percentage of respondents expecting an improvement / good time to buy durable goods less the percentage expecting a deterioration / bad time to buy durable goods.

A low level of confidence indicates that consumers are concerned about the future. They may be worried about job security, pay raises and bonuses. With such a frame of mind, consumers tend to cut spending to basic necessities (e.g. food and services) to free up income for debt repayment. If confidence is high, consumers tend to incur debt (or reduce savings) and increase spending on discretionary items, such as furniture, household equipment, motor vehicles, clothing and footwear. Some of these items are often financed on credit. Spending on these items declines when confidence is low, as households can generally delay their purchase without experiencing an immediate deterioration in living conditions.

A rise in consumer confidence reflects an increased willingness of consumers to spend. However, this willingness only translates into actual sales if consumers’ ability to spend improves. Their ability to spend depends on their inflation adjusted after-tax income and the availability of credit. A rise in consumer confidence could therefore result in an upturn in household consumption spending in general and retail and motor vehicle sales in particular. The opposite applies when the level of consumer confidence declines.