FNB/BER Consumer Confidence Index

Siphamandla Mkhwanazi, Senior Economist at FNB

Consumer confidence edges up despite riots and looting

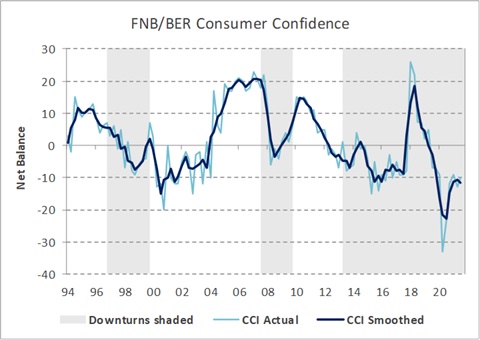

Having slipped from -9 to -13 index points during the second quarter of 2021, the FNB/BER Consumer Confidence Index (CCI) recovered some lost ground to -10 in the third quarter of 2021.[1] The fact that consumer sentiment did not deteriorate further on the back of the violent protests and rampant looting that tore through KwaZulu-Natal and Gauteng during July points to a level of resilience among consumers, and by extension consumer spending, during the third quarter of 2021. While the latest CCI reading of -10 remains well below the average CCI reading (of +2 since 1994) and therefore denotes depressed consumer confidence levels, it is nevertheless quite close to the reading of -9 recorded just prior to the onset of the COVID-19 epidemic in South Africa (in the first quarter of 2020).

Details

The increase in the CCI during the third quarter of 2021 can be ascribed to upticks in the household financial position and time-to-buy durable goods sub-indices of the CCI. Consumers turned notably less pessimistic about the appropriateness of the present time to buy durable goods (e.g. vehicles, furniture, household appliances and electronic goods), with this index recovering by 7 points to the best reading since the first quarter of 2020 - albeit still quite negative at -29 index points. The household finances index improved by 2 index points to +12, indicating that the majority of consumers anticipate an improvement in their household finances over the next 12 months. However, the economic outlook sub-index of the CCI remained rather depressed at -14 index points.

|

19Q3 |

19Q4 |

20Q1 |

20Q2 |

20Q3 |

20Q4 |

21Q1 |

21Q2 |

21Q3 |

|

|

Overall FNB/BER CCI |

-7 |

-7 |

-9 |

-33 |

-23 |

-12 |

-9 |

-13 |

-10 |

|

Economic outlook |

-17 |

-14 |

-16 |

-21 |

-23 |

-12 |

-5 |

-14 |

-14 |

|

Household financial outlook |

12 |

11 |

14 |

-13 |

-2 |

6 |

10 |

10 |

12 |

|

Suitability of the present time to buy durable goods |

-15 |

-18 |

-26 |

-64 |

-44 |

-30 |

-32 |

-36 |

-29 |

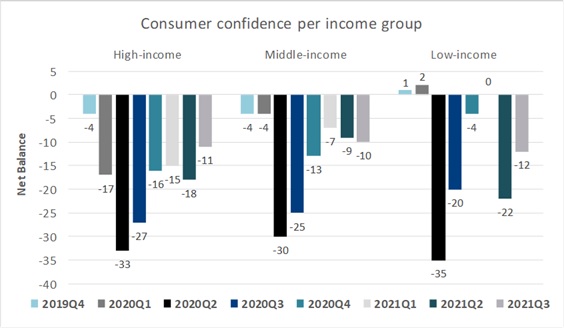

A breakdown of the CCI per household income group shows diverging results for the different income groups in South Africa. The confidence levels of high-income households (earning more than R20 000 per month) increased significantly, from -18 to -11 during the third quarter, while low-income confidence (consumers earning less than R2 500 per month) also rebounded strongly from -22 to -12. However, the confidence levels of middle-income households (earning between R2 500 and R20 000 per month) slipped further from -9 to -10 index points. Whereas the second quarter saw a sharp drop in the confidence levels of low-income consumers to lower levels compared to that of the other two income groups, the confidence levels of all three income groups were at broadly similar levels during the third quarter of 2021.

FNB Senior Economist Siphamandla Mkhwanazi said that "The reinstatement of the R350 per month Social Relief of Distress (SRD) grant between August 2021 and March 2022 would have been a major relief to millions of low-income households. Given soaring food and fuel prices and the fact that South Africa's unemployment rate climbed to a record high during the second quarter, the expiration of these grants at the end of April left gaping holes in the budgets of low-income households."

Similar to the CCI results for the low-income group, the upturn in consumer sentiment among high-income consumers was also largely driven by an improvement in their household financial prospects. Mkhwanazi noted that "The public sector wage agreement that was reached at the end of July in all likelihood bolstered the confidence levels of the more than a million civil servants in South Africa, most of whom fall in the high-income category. Although government employees will only receive a 1.5% increase in their salaries this year, the wage deal does include a non-pensionable cash allowance for civil servants ranging between R1 220 and R1 695 per month until March 2022. Since the cash allowances will be backdated to 1 April 2021, government employees will receive a significant boost to their September remuneration." The recent uptick in dividend payments likely also boosted the confidence levels of affluent consumers and contributed to their increased willingness to purchase durable goods during the third quarter.

In contrast to the high- and low-income groups, middle-income consumers turned less optimistic about the outlook for their household finances during the third quarter. This accounted for the small decline in the overall sentiment among middle-income consumers. Middle-income earners would typically not qualify for the reinstated SRD grant, but some will be government employees that would benefit from the recently negotiated cash allowances. Mkhwanazi said that "The alarming decline in formal sector employment during the second quarter - a drop of 375 000, or 3.5% quarter-on-quarter - in all likelihood hit middle-income households the hardest. The violent looting and arson that ravaged shopping malls, warehouses, factories and small businesses in KwaZulu-Natal and Gauteng during July would only have exacerbated the employment prospects for middle-income earners in particular during the third quarter." Furthermore, middle-income consumers are also less likely to be able to work from home compared to high-income earners, implying that soaring petrol prices - up by nearly R3,50 per litre since January - would also have a disproportionally negative impact on this group.

Bottom line

The protests, looting and property destruction that engulfed parts of KwaZulu-Natal and Gauteng would undoubtedly have knocked both business and consumer confidence during July. However, it appears as though the subsequent announcements of substantial further fiscal support in the form of the reintroduction of the SRD grant and cash allowances for government employees to a large extent countered the adverse impacts of the civil unrest on consumer confidence during the third quarter. The rollout of COVID-19 vaccinations to the 35-49 age group from 15 July and subsequently to the 18-35 age group from 20 August probably also bolstered the confidence levels of these age groups.[2]

The fact that consumer sentiment was able to recover so quickly following the extended level 4 lockdown and unprecedented social unrest points to a level of resilience amongst consumers - consumer spending may well hold up better than initially anticipated during the second half of 2021. Yet, since total employment remains nearly 1.5 million below pre-COVID levels, much of this resilience appears to be tied to government support, as well as special factors such as retrenchment packages and life insurance payouts. "We remain hopeful that job creation will start to recover next year once heavily hit industries such as tourism, liquor and restaurants and hotels are able to reopen fully, and that this will sustain the consumer spending recovery. However, there is certainly downside risk to the outlook should the current sizeable levels of fiscal support and other special factors propping up household income start to fade," said Mkhwanazi.

[1] The third quarter CCI survey was conducted by means of a telephone call survey between 16 and 31 August 2021. South Africa was on level 4 of the risk adjusted strategy from 28 June to 25 July, which included a 9pm curfew at night, prohibited social gatherings and leisure travel from Gauteng and once again banned alcohol sales. The country reverted back to adjusted alert level 3 on 26 July 2021.

[2] Confidence levels increased slightly across all age groups during the third quarter, bar the 50+ age group.