FNB/BER Consumer Confidence Index

Consumer confidence edges up further

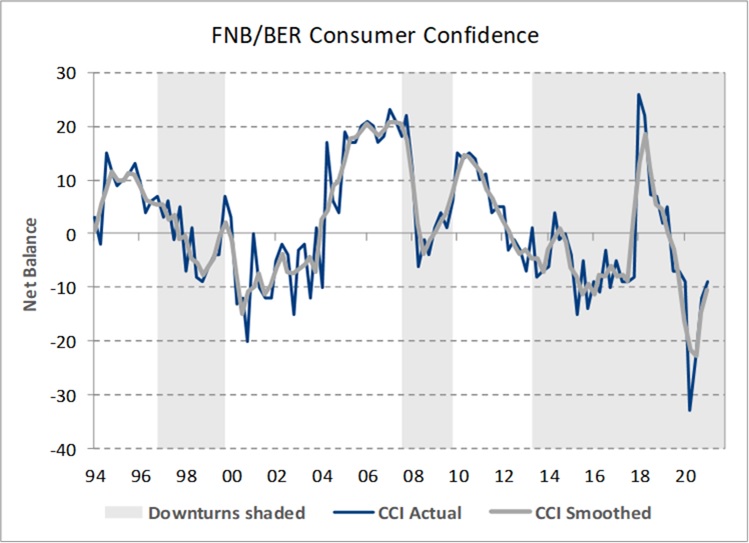

The FNB/BER Consumer Confidence Index (CCI) increased by another 3 index points to a level of -9 in the first quarter of 2021.[1] Prior to the COVID-19 outbreak, a deterioration in South Africa's economic prospects already saw the CCI retreat from +7 at the end of 2018 to -7 in the fourth quarter of 2019. The sudden onset of the coronavirus pandemic and the concomitant severe economic restrictions saw consumer confidence collapse to a 35-year low of -33 in the second quarter of 2020. The recovery to -9 index points brings the CCI back in line with the reading recorded in March 2020, just before South Africa entered its first strict nationwide lockdown. Although it is heartening that the CCI has now recovered most of its COVID-19-induced losses, consumer confidence in general remains depressed - the latest reading of -9 is still well below the average CCI reading of +2 since 1994.

Details

The continued recovery in the CCI during the first quarter of 2021 can be ascribed to further increases in the economic outlook and household finances sub-indices of the CCI. The economic outlook index booked another solid gain of 7 index points to reach a level of -5, the best reading since the second quarter of 2019. The household financial outlook sub-index of the CCI edged up further from +6 to +10 index points - now only slightly below its first quarter of 2020 reading of +14. However, the sub-index measuring the appropriateness of the present time to buy durable goods (e.g. vehicles, furniture, household appliances and electronic goods) slipped back from -30 to -32 index points during the first quarter of 2021.

|

18Q4 |

19Q1 |

19Q2 |

19Q3 |

19Q4 |

20Q1 |

20Q2 |

20Q3 |

20Q4 |

21Q1 |

|

|

Overall FNB/BER CCI |

7 |

2 |

5 |

-7 |

-7 |

-9 |

-33 |

-23 |

-12 |

-9 |

|

Economic outlook |

14 |

0 |

11 |

-17 |

-14 |

-16 |

-21 |

-23 |

-12 |

-5 |

|

Household financial outlook |

15 |

13 |

13 |

12 |

11 |

14 |

-13 |

-2 |

6 |

10 |

|

Suitability of the present time to buy durable goods |

-7 |

-8 |

-10 |

-15 |

-18 |

-26 |

-64 |

-44 |

-30 |

-32 |

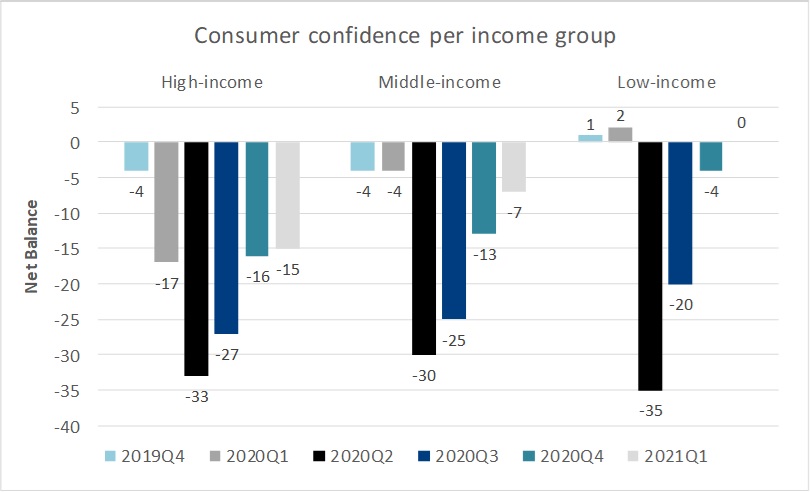

A breakdown of the CCI per household income group shows that middle-income confidence (i.e. households with a monthly income of between R2 500 and R20 000) and low-income confidence (earning less than R 2 500 p.m.) posted the largest gains in the first quarter of 2021. The confidence levels of middle-income consumers jumped by 6 index points to -7 in the first quarter, while low-income confidence rose from -4 to zero. The confidence level of high-income consumers (earning more than R20 000 p.m.) edged up by only 1 index point and, at a level of -15, remains the lowest of all the income groups. Unlike low- and middle-income consumers, high-income households are still very concerned about the outlook for the South African economy and are also considerably less optimistic about their financial prospects over the next 12 months. Consumers across all income groups consider the present time as highly inappropriate to purchase durable goods.

FNB Chief Economist Mamello Matikinca-Ngwenya noted that, "A range of positive developments in all likelihood supported the sustained recovery in consumer confidence during the first quarter, including a sharp decline in COVID-19 infection rates since the peak of the second wave in early January; the extension of the Social Relief of Distress (SRD) grant and Temporary Employer/ Employee Relief Scheme (TERS) through the end of April 2021; higher-than-inflation adjustments to personal income tax brackets, soaring stock prices on the JSE; and a recovery in employment - albeit muted - as the South African economy continues to mend. Notwithstanding some challenges and delays, the eventual commencement of the COVID-19 vaccine rollout to thousands of healthcare workers may also have lifted the spirits of some South Africans."

To be sure, there were also some adverse developments that probably curbed the upward momentum of the CCI during the first quarter. Knocked by a plunge in company profit levels in 2020, lower end-of-year performance bonusses likely checked the confidence levels of high-income consumers heading into 2021. Workers in the hospitality and entertainment industry (such as hotels, guest houses, restaurants, wedding venues and casino’s) faced reduced working hours and earnings due to the absence of international tourists, the closure of beaches, the alcohol sales ban, restrictions in the number of people at gatherings and the extended curfew during the crucial summer holiday season. Sporadic periods of load-shedding also dampened consumer confidence.

Low-income households will likely soon start to feel the pinch from surging petrol and paraffin prices, marked increases in excise duties on alcoholic beverages and tobacco products and below-inflation increases in the monetary values of social grants. These factors, coupled with the fact that the SRD grant and TERS programme are set to expire at the end of April, have the potential to deflate the confidence levels of less affluent consumers in particular in coming months.

Another noteworthy development in the latest consumer confidence survey is the fact that - in contrast to the sustained recovery in the other two sub-indices of the CCI - the index measuring the appropriateness of the present time to buy durable goods actually sagged back slightly. This finding is in line with the results from the BER's latest retail survey, which showed a deterioration in durable goods sales volumes during the first quarter of 2021. Matikinca-Ngwenya said that, "The cumulative 300-basis-point cut in the prime interest rate and shift to work-from-home and home-schooling boosted sales of office furniture and equipment, electronics and DIY hardware products during the second half of 2021. However, in the absence of further interest rate cuts, and with an increasing number of workers now returning to company offices and more schools reopening fully, the demand for these types of durable goods has started to wane."

Bottom line

The further uptick in consumer confidence during the first quarter of 2021 is good news for the consumption driven South African economy, but the recovery continues to be fuelled by a rise in low and middle-income sentiment. The economic boost would be more robust had the confidence levels of high-income consumers - the group with the largest spending power - increased in line with that of low- and middle-income consumers. Instead, the confidence levels of affluent consumers remain exceedingly depressed, pointing to a low willingness to spend.

In addition, the recent rise in the CCI was purely driven by upticks in the two forward looking indicators - namely consumers' expectations about the performance of the national economy and their household finances in 12 months' time - while the sub-index measuring the appropriateness of the present time to buy durable goods slipped back somewhat. Matikinca-Ngwenya pointed out that, "Given the sharp increases in fuel prices, mounting food inflation, below-inflation adjustments to social grants and the expiration of the SRD grant and TERS programme at the end of April, there is a real risk that the household finances of low-income consumers could come under more pressure compared to their current optimistic expectations. This would likely put the brakes on non-durable goods consumption, whereas the latest survey results suggest that the growth in durable goods consumption has already started to slow."

Employment levels would have to rebound considerably in order to counter these unfavourable dynamics, but job creation may also face headwinds in the form of a potential third wave of coronavirus infections and the concomitant further economic restrictions, as well as South Africa's protracted power supply crisis. In all, the pace of the recovery in real household consumption expenditure is therefore expected to slow somewhat compared to the fourth quarter, despite the slight increase in consumer confidence in the first quarter of 2021.

Background

Consumer confidence surveys provide regular assessments of consumer attitudes and expectations and are used to evaluate economic trends and prospects. The surveys are designed to explore why changes in consumer expectations occur and how these changes influence consumer spending and saving decisions.

The FNB/BER CCI combines the results of three questions posed to adults in South Africa, namely the expected performance of the economy, the expected financial position of households and the rating of the appropriateness of the present time to buy durable goods, such as furniture, appliances and electronic equipment.

Until the second quarter of 2019, the FNB/BER CCI was based on face-to-face interviews of between 2 000 and 2 500 urban adults. Due to weak demand, the three service providers in South Africa - Nielsen, Ipsos Markinor and TNS Kantar – could not always guarantee surveys with a quarterly frequency between 2016 and 2019. Internationally, the majority of CCIs are based on telephone call surveys. As a result, the BER switched to telephone call surveys in the third quarter of 2019. The 500 respondents are representative of the racial and household income composition of the urban adult population of South Africa.

Consumer confidence is expressed as a net balance. The net balance is derived as the percentage of respondents expecting an improvement / good time to buy durable goods less the percentage expecting a deterioration / bad time to buy durable goods.

A low level of confidence indicates that consumers are concerned about the future. They may be worried about job security, pay raises and bonuses. With such a frame of mind, consumers tend to cut spending to basic necessities (e.g. food and services) to free up income for debt repayment. If confidence is high, consumers tend to incur debt (or reduce savings) and increase spending on discretionary items, such as furniture, household equipment, motor vehicles, clothing and footwear. Some of these items are often financed on credit. Spending on these items declines when confidence is low, as households can generally delay their purchase without experiencing an immediate deterioration in living conditions.

A rise in consumer confidence reflects an increased willingness of consumers to spend. However, this willingness only translates into actual sales if consumers’ ability to spend improves. Their ability to spend depends on their inflation adjusted after-tax income and the availability of credit. A rise in consumer confidence could therefore result in an upturn in household consumption spending in general and retail and motor vehicle sales in particular. The opposite applies when the level of consumer confidence declines.