Economic and market snapshot for November 2015

Sanisha Packirisamy, Economist at MMI.

Herman van Papendorp (Head of macro research) from MMI.

Global economic developments.

United States (US)

Short-term outlook on consumption remains encouraging, keeping the prospect of a December rate hike on the table

Although October’s personal spending and durable goods data led the Atlanta Fed 4Q15 GDP Nowcast (a high-frequency statistical model predicting GDP growth) lower, to 1.8% in late-November from 2.5% in mid-November, there are some positive growth signals emerging for the remainder of the fourth quarter.

Real disposable income continued to grow at 3.3% y/y in October, while a robust c.8% y/y uptick in household credit extension suggests scope for further gains in consumption spend in upcoming months. Meanwhile, labour market conditions have strengthened further, with the headline rate of unemployment falling to 5% and payroll gains averaging close to 215 000 over the past six months. Moreover, the number of discouraged work seekers (those that have given up looking for work for a period longer than a month) has nearly halved since its post-crisis peak. The level of long-term unemployment (>15 months) has furthermore dropped back to 2.1 million from c.6 million in early-2009.

With the labour market rapidly approaching full employment, wage growth has shown tentative signs of rising price pressures. We expect rising wage and still-elevated housing inflation to drive headline prints higher over the course of 2016. Anchored inflation expectations further argues for rates to be lifted from ultra-low levels, albeit at a protracted pace, given tighter monetary conditions from a stronger dollar and lingering global growth concerns, which could negatively impact US economic activity.

Chart 1: Market sees a 70% chance of a Dec ‘15 rate hike

Source: Bloomberg, Momentum Investments

Eurozone

More easing likely as persistently-low inflation threatens to de-anchor inflation expectations

Headline CPI in the Eurozone remained subdued at 0.1% y/y in October, following a renewed dip in oil prices and leaving the European Central Bank’s (ECB) 2% inflation target still largely out of reach. External emerging market (EM) risks and a still-fragile economic outlook has led to the expectation that potentially over-stimulating the economy may hold a lesser risk for the Eurozone outlook than not stimulating enough. This sentiment was reiterated by ECB President Draghi more recently when he commented that: "If we conclude that the balance of risks to our medium-term price stability objective is skewed to the downside, we will act by using all the instruments available within our mandate".

The ECB has indicated that a deposit rate cut and changes to the quantitative easing (QE) programme top the list of easing options at the ECB’s disposal. Given fairly high market expectations, their delivery of additional stimulus will need to reflect an aggressive commitment to raising inflation in order to prevent an unwind in the fall in the euro (see chart 2).

Chart 2: EURUSD could unwind on lack of ECB action

Source: Bloomberg, Momentum Investments

Japan

Struggling to spur inflation and economic growth in the absence of further monetary stimulus

In response to a string of weak economic data, the Bank of Japan has been forced to cut its growth outlook and extend the timeline for achieving its 2% inflation goal. Prime Minister Abe has responded by ordering his government to draft a supplementary fiscal budget in light of disappointing growth and inflation prints.

Chart 3: Japan’s 2% inflation target remains elusive

Source: Bloomberg, Momentum Investments

The budget for the current fiscal year will now include more support for rural areas and cash payouts to low-income households to kick-start private consumption. Falling inflation (see chart 3) has created an incentive for delaying spending in the economy as consumers factor in the potential of paying less for the same goods further down the line. This has had a negative consequence on firms’ expansion and hiring plans, hurting economic growth prospects overall.

Emerging markets (EM)

Growth continues to slow, but no signs of a collapse

Capital Economics’ EM GDP tracker showed a slight deceleration in September, but the third quarter GDP prints for the underlying regions confirm that the rate of slowdown has abated since the start of the year. Overall EM GDP growth has shown a decline from c.4% in 1Q15 to c.3% in 3Q15.

Although growth in the so-called BRIC nations (Brazil, Russia, India and China) continues to outstrip that of their non-BRIC counterparts, the gap between the two continues to narrow primarily as a result of a further decline in BRIC GDP, while growth in the non-BRIC composite has been reasonably stable for the most part of two and a half years.

EM private consumption in 2Q15 grew at the weakest pace since 2009, at 1.7% y/y. This was mainly driven by softer growth in household spend in net commodity-exporting EMs which have undergone a negative terms-of-trade shock, triggering weaker economic conditions. In select EMs, a combination of inflationary pressures and tighter fiscal and monetary policy suggests little scope for a major turnaround in spend in 2016.

EM export growth is negative across the board. The Emerging Europe, Middle East and Africa region experienced the largest decline, close to 25% y/y in September on a rolling three-month basis. This was followed by a 15% y/y decline in exports in Latin America, while exports in Emerging Asia were c.10% y/y lower than a year ago. Although economic surprise data in EM exports points to a marginal turnaround, on a net basis export data continues to surprise on the downside (see chart 4).

Chart 4: EM export surprises (net balance, %)

Source: Bloomberg, Momentum Investments

Local economic developments

SA avoids a technical recession, but unexciting growth prospects lie ahead

SA avoided a technical recession (two consecutive quarters of negative growth) in 3Q15, with overall economic activity expanding by 0.7% q/q in seasonally-adjusted annualised terms (1.0% y/y). Growth in the tertiary sector (the largest contributor to overall economic activity) maintained a positive growth rate of 1.9% q/q from 1.0% previously, supporting overall economic growth in the third quarter of the year.

Meanwhile, three out of the ten GDP sectors (viz. agriculture, mining and utilities) printed negative growth rates for two consecutive quarters (see chart 5). However, the negative impact on overall growth was limited as these components accounted for only 12% of GDP in 3Q15. Growth in the agriculture sector, which contributed a mere 2% of GDP over the corresponding period, contracted by 12.6% q/q on a seasonally-adjusted (saar basis), following a sharp 19.7% decline in 2Q15 due to the decrease in production of field crops. The SA non-agricultural economy expanded by 1.1% q/q saar, recovering from a 1.0% contraction in 2Q15.

Chart 5: Three SA GDP sectors in a technical recession

Source: Stats SA, Global Insight, Momentum Investments

Drought conditions and further pressure on commodities are likely to further damage growth rates in the primary sector (agriculture and mining) of the economy in upcoming quarters, but we expect this to be offset by mildly positive growth in the less cyclical tertiary/services sectors culminating in an overall pedestrian outlook for economic growth over 2016.

Financial market performance

Global markets

World stock markets showed a mixed performance over November, while commodity prices grinded lower. Copper, gold, iron ore, nickel and the Baltic Freight index all posted new multiyear lows on falling industrial profits in China, a firm US dollar and continued anxiety over the potential for US monetary policy to start diverging from other major markets.

The MSCI World Index dipped by 0.5% over the month despite solid gains in the Eurostoxx 50 (+2.7%) and Nikkei 225 (+3.5%) indices on mounting speculation of further monetary stimulus in response to still-weak inflation and fragile growth.

Meanwhile, the MSCI Emerging Markets Index declined by 3.9% over November, partly thanks to lower commodity prices which collapsed by 7.3% over November. Within EM, the largest falls were observed in the MSCI Emerging Markets EMEA and Latin America indices which slipped by 6.2% and 4.2%, respectively. The MSCI Emerging Markets Asia Index settled 3.3% lower over the corresponding period.

Despite the steep decline in commodity prices and rising geopolitical tensions, volatility measures remained well-behaved, tracking largely sideways over the month.

Local markets

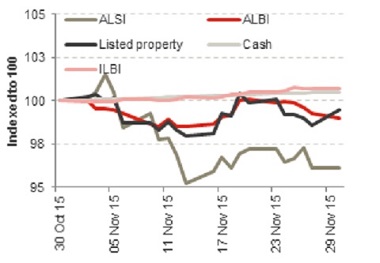

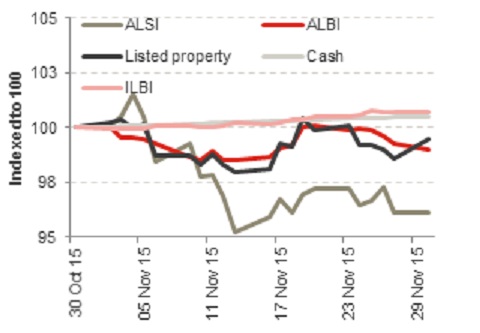

The South African equity market (FTSE/JSE ALSI) followed emerging markets lower, dipping by 3.9% in November (see chart 6). The FTSE/JSE Resources Index posted the worst performance, plunging by over 20% over the month. The FTSE/JSE Financials and Industrials indices also printed in the red, but falls were limited to 3.4% and 1.2%, respectively.

Chart 6: Local asset class returns

Source: Bloomberg, INET BFA, Momentum Investments

The FTSE/JSE Mid-cap Index lost 4.2% over November, while the FTSE/JSE Small-caps index fell by a lesser 0.3% over the same time period. Both the ALBI and the listed property returns were negative for November, declining by 1.0% and 0.5%, respectively.

This left inflation-linked bonds and SA cash as the outperforming asset classes in November, increasing by 0.7% and 0.5%, respectively.

In line with emerging market peer currencies, the rand extended losses against the US dollar, depreciating by 4.3% over the month. The rand was flat against the euro over the corresponding period given the long stretch of declines in the euro as investors continued to price in a stimulus package from the ECB in response to benign inflation and a weak growth outlook in the Eurozone.