Economic and market snapshot for January 2016

Sanisha Packirisamy, Economist at MMI Holdings.

Herman van Papendorp, Head of macro research at MMI Holdings.

Global economic developments.

United States (US)

US futures market pushed out rate hike expectations in response to negative growth surprises

In line with market expectations, the US Federal Reserve (Fed) kept benchmark interest rates on hold at the first rate setting meeting of 2016 after lifting rates for the first time in nearly a decade, from a range of 0–0.25% to 0.25-0.5%, in December 2015.

The Federal Open Market Committee (FOMC) admitted to slowing economic growth over the final quarter of 2015 despite a further improvement in labour market conditions. Although economic growth surprises have moved decisively into negative territory (see chart 1), we expect firmer growth to resume over the course of 2016 on the back of a strong employment recovery, firm credit extension and supportive real wage growth.

Chart 1: Negative growth surprises in the US

Source: Bloomberg, Momentum Investments

Nevertheless, tighter financial conditions, tame inflation and uncertainty around potentially negative spillover effects (arising from adverse global economic and financial market developments) are likely to remain key considerations in further gradual adjustments in the stance of monetary policy.

Eurozone

European Central Bank (ECB) talked up prospects of additional stimulus to boost ultra-low inflation

The ECB kept policy on hold at the January 2016 interest rate meeting, but kept the door open to further easing. ECB President Mario Draghi hinted that the Bank was ready to respond to disinflationary pressures by launching additional stimulus on top of the current €1.5 trillion programme. In the news conference following the rate decision, Draghi disclosed that the entire governing council had agreed to “review and possibly consider” the bank’s stimulus at the next rate-setting meeting in March.

Draghi warned that a sharp drop in oil prices and headwinds from financial and commodity markets could entrench ultra-low inflation in the Eurozone (see chart 2).

In our view, growth fragilities, given still-weak corporate credit extension and fading growth support from lower oil prices and a weaker euro (relative to 2015), could further urge the ECB into action – either through an additional cut in the deposit rate or an expansion in current monthly asset purchases.

Although we expect the ECB to take stock of the effectiveness of their latest actions before embarking on additional easing, they will need to convince the market about the capacity of the Bank to act timeously against rising deflationary risks.

Chart 2: Eurozone inflation remains stubbornly low (%)

Source: Bloomberg, Momentum Investments

Japan

Bank of Japan (BoJ) shifted focus away from quantitative balance sheet expansion back to interest rates

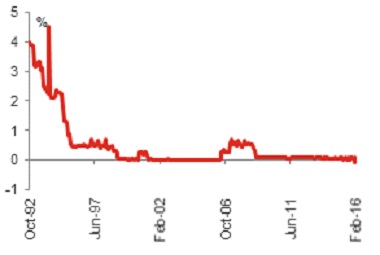

In a widely unanticipated move, the BoJ (in a narrow 5-4 vote) cut their benchmark interest rate below zero (to be implemented in mid-February), effectively charging 0.1% on selected current account deposits that financial institutions hold with it (see chart 3).

Although the BoJ stated their intention to continue with its bond buying programme, embarking on negative interest rate policy (NIRP) could be an indication of declining effectiveness of large-scale asset purchases. They indicated that they could cut the interest rate further into negative territory “if judged necessary”.

Chart 3: Japan embraces NIRP

Source: Bloomberg, Momentum Investments

The BoJ still sees a moderate recovery underway in the Japanese economy boosted by higher real wage growth, but concerns over recent negative developments in emerging markets raises risks to the growth outlook. In our view, a slowdown in growth in investment spend and a muted response from export volumes to a weaker currency pose further downside risks to economic activity.

Emerging markets (EM)

EM fragilities remain a threat to shallow global growth recovery

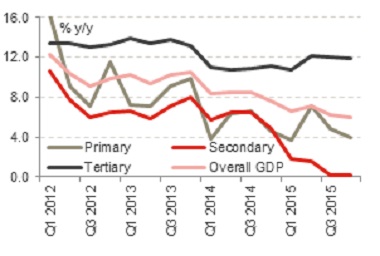

Despite an increase in real incomes, rising unemployment has weighed negatively on private consumption spend in key EMs, while slowing credit growth has led to an underperformance in investment spend. Eroding fiscal and monetary policy buffers are further likely to limit a faster acceleration in domestic demand growth. Meanwhile, soft commodity prices (owing to a significant supply overhang and China’s shift away from commodity-intensive growth – see chart 4) and increased on-shoring by developed markets has suppressed global trade activity, curbing emerging economies’ export contributions to overall GDP growth.

Chart 4: Chinese GDP growth buoyed by services

Source: China NBS, Momentum Investments, data up to 4Q15

A 6.9% print in 2015 marked the slowest annual growth rate in China in a quarter of a century, marginally undershooting the official 7% growth target. We expect a managed slowdown in the economy as the central government steers the country away from an export- and investment-led growth model towards less commodity-intensive consumption and services growth.

A deeper adjustment in the low value-add manufactured goods industries and moderating investment growth is unlikely to arrest a slowdown in primary and secondary GDP sectors, whereas government support and steady confidence is likely to keep services and consumption growth afloat.

Local economic developments

South African Reserve Bank (SARB) raised rates by 50 basis points amid weak growth

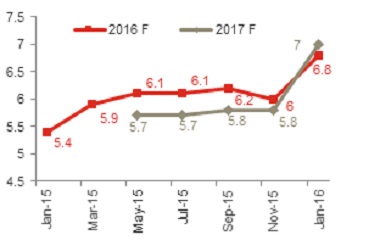

Despite signs of a weakening domestic economy, the SARB raised interest rates by 50 basis points in an effort to contain rising prices. A sharp 12.9% depreciation in the trade-weighted currency since the November meeting and drought-inflicted food price shocks have driven the SARB’s inflation projections considerably higher over the next two years relative to their previous November 2015 forecasts.

The SARB now sees average headline inflation at 6.8% in 2016 (previously 6.0%, see chart 5), peaking at 7.8% in 4Q16 and 1Q17 (previously 6.9% in 1Q16). Headline inflation is expected to remain outside the target band for the full forecasted horizon (two years), whereas previously it was expected to breach for two quarters only.

The Bank has shown a firm commitment to their inflation targeting regime by reacting pre-emptively to a rising inflation trajectory. In our view, a higher inflation profile, stubbornly-high inflation expectations and a sizeable current account deficit still point to the need for a further rise in interest rates.

Chart 5: SARB headline CPI forecast revisions (%)

Source: SARB, Momentum Investments

We expect rates to rise by a further three increments of 25 basis points each over the course of 2016-2017 as the Monetary Policy Committee (MPC) continues to balance rising inflation pressures against further downside risks to economic growth. The pace of additional rate tightening will likely remain a function of how inflation expectations react to the increasing risks of a low growth and high inflation environment.

Financial market performance

Global markets

A violent lurch lower in world stock markets at the start of 2016 was initially triggered by renewed fears of an economic slowdown in China, after the region posted its lowest annual growth rate in two and a half decades. An oil price slide further compounded the pessimism in financial markets.

World stock markets staged a recovery in the last week of January on further talk of easing by the ECB and the adoption of NIRP by the BoJ. The MSCI World Index declined by 6% in January, driven by an 8% decline in the Nikkei 225 and a 6.6% decline in the Eurostoxx 50 indices, followed by a 5.0% dip in the S&P 500 Index.

Intra-month, the Eurostoxx 50 Index jumped by 5.8% in late January on the increased likelihood of additional stimulus measures, while the Nikkei 225 Index surged by 9.4% following an unexpected cut in the benchmark rate into negative territory.

The MSCI Emerging Markets Index suffered a 6.5% blow in January, with the MSCI Emerging Markets Asia Index collapsing by 7.3% on the back of Chinese growth concerns. This was followed by a 4.6% drop in the MSCI Latin America Index and a 4.2% drop in the Emerging Markets EMEA Index.

Following a 1.7% dip in commodity prices, the VIX volatility index nudged higher by 2 index points in January.

Local markets

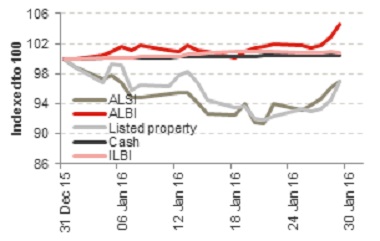

The South African equity market (FTSE/JSE ALSI) followed global markets lower, dipping by 3% during January (see chart 6).

Chart 6: Local asset class returns

Source: Bloomberg, INET BFA, Momentum Investments

The FTSE/JSE Financials Index was the hardest hit, falling by 3.3% in January while the FTSE/JSE Industrials Index and the FTSE/JSE Resources Index lost 2.9% and 2.7%, respectively. The FTSE/JSE Mid-cap Index gained 2.7% in January, while the FTSE/JSE Small-caps Index weakened by a further 4.6% over the corresponding period.

The ALBI posted gains in excess of 4.5% (SA ten-year yields rallied by 55 basis points), while further losses (-3.0%) in listed property were noted in January. Inflation-linked bonds ended the month marginally higher (+0.8%), followed by a 0.5% gain in SA cash.

The rand staged a recovery in late January, following a decisive 50 basis point move higher in domestic interest rates in an effort to combat rising inflationary pressures, but earlier losses in the month still left the rand 2.5% weaker against the dollar and 2.4% weaker against the euro.