Economic and market snapshot for February 2016

Sanisha Packirisamy, Economist at MMI Holdings.

Herman van Papendorp, Head of Asset Allocation at MMI Holdings.

Global economic developments.

United States (US)

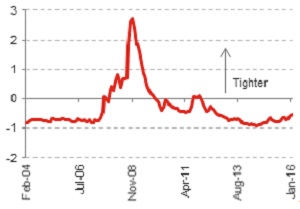

Financial conditions have tightened, but not signalling a recession

Various indices show that financial conditions (financial shocks that influence economic activity) have tightened over recent months due to falling stock prices, a widening in credit spreads and a further strengthening in the US dollar.

The Chicago Fed’s National Financial Conditions Index (FCI), which measures a wider range of financial activity indicators, points to a smaller deterioration in financial conditions than the Goldman Sachs FCI. Although this index remains low on a historic comparison, the Chicago Fed’s National FCI is currently registering the tightest financial conditions observed since 3Q12 (see chart 1), consequently posing a downside risk to overall GDP growth this year.

Chart 1: Chicago Fed’s FCI ticking higher

Source: Bloomberg, Momentum Investments

According to Deutsche Bank research, if the tightening in financial conditions is sustained, the resultant drag on real GDP growth would be the equivalent of one interest rate hike.

Though tighter financial conditions and global growth fragilities have eroded chances of a hike at the March rate-setting meeting. incoming economic data looks broadly consistent with the US Federal Reserve’s (Fed) outlook. Negative economic surprises bottomed out in early February and have started to reverse. Moreover, lower unemployment rates and rising wages support a modest interest rate hiking cycle.

Eurozone

Further easing by European Central Bank (ECB) likely following sharply weaker economic surprise data

Economic surprises have plummeted since the start of the year. In addition to a slowdown in activity, business and consumer sentiment has waned, pointing to a soft GDP print for the first quarter of the year.

The rate of expansion slowed in both the manufacturing and services sectors in February (see chart 2), with the flash estimates of the headline Purchasing Managers’ Indices (PMI) declining further in the region’s two largest economies, namely Germany and France. The slowdown in the manufacturing index has most likely followed on from on-going weakness in emerging markets (EM) and a rebounding euro which has hurt manufacturers in the region, while supportive real wage growth, modest gains in employment and continued fiscal easing should prevent a shallower recovery in overall gross domestic product (GDP) growth.

Chart 2: Momentum in economic sentiment rolling over

Source: Bloomberg, Momentum Investments

Nevertheless, recent financial market turmoil suggests a further risk to the credit transmission mechanism in the Eurozone and the stability of the region’s banks, which could feed back negatively into lower growth prospects.

In December 2015, the ECB cut its deposit rate by 10 basis points to -0.3% and extended its asset buying programme by six months, taking it to €1.5 trillion euros. With current market turbulence derailing the ECB’s efforts to boost inflation and lift economic activity, we expect the ECB to ease policy further either by cutting the deposit rate again or by increasing/front-loading asset purchases.

Japan

Yen weakness insufficient to revitalise Japanese exports

The Japanese economy continues to feel the aftershocks of the global financial crisis (GFC). The latest GDP figures show that the Japanese economy is shrinking again. Economic activity contracted by an annualised 1.4% in 4Q15, exceeding the market’s consensus forecast for a 0.8% decline.

Chart 3: Lack of clear growth in export volumes

Source: Bloomberg, Momentum Investments

The first two arrows in Prime Minister Abe’s economic policy quiver (dubbed Abenomics), including the monetary arrow (expanding money supply to combat inflation) and the fiscal arrow (stimulating demand via increased government spending), have failed to sustainably boost export volumes since the GFC (see chart 3). The effect of yen depreciation on Japanese exports has weakened given the stronger link between the yen and rising production costs, as well as a loss in global competitiveness. Moreover, Japanese manufacturers are increasingly meeting overseas demand via products produced in nearby countries rather than in Japan itself. As a result, yen weakness has had only modest effects on Japanese exports and overall growth.

Though the Bank of Japan (BoJ) has adopted negative interest rates in an effort to stimulate the economy and overcome deflation, inflation expectations have softened further. As such, Japanese authorities may be forced to consider further monetary and fiscal stimulus.

Emerging markets

Gloomy outlook for those EMs facing high inflation risks and sticky external imbalances

Though the gradual pace of interest rate rises expected from the US Federal Reserve should allow for some breathing room in emerging markets, the outlook for many EMs (particularly those facing high inflation risks and sticky external imbalances), remains grim.

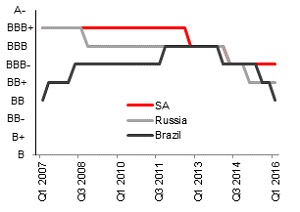

Weaker commodity prices have weighed negatively on net commodity-exporting nations, particularly those which are heavily dependent on commodity-related revenues such as Russia and Brazil. In addition to poor external conditions, a series of problematic policy decisions have weakened the Brazilian economy, which is likely to post a negative growth print in 2016 for the second year in a row.

Economic and political stresses have prompted Standard & Poor’s (S&P) rating agency to downgrade Brazil’s sovereign debt rating to BB as the slide in international oil prices has eroded fiscal buffers (see chart 4). S&P kept Brazil on a negative outlook, suggesting that Latin America’s largest economy remains at risk of a further loss in creditworthiness.

Chart 4: S&P sovereign debt ratings (long-term debt)

Source: Bloomberg, Momentum Investments

Local economic developments

Limited revenue proposals raise fiscal risks

SA’s tax receipts have waned in the face of softer economic growth. The three largest contributors to overall tax (personal income tax, value-added tax and company income tax) have all fallen short of government’s earlier expectations in FY2015/16, while property taxes, fuel levies and international trade taxes (thanks to a weaker currency) have exceeded projections.

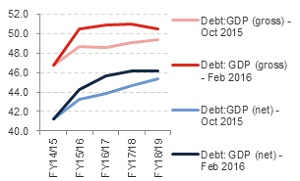

Chart 5: Deterioration in SA government debt profile (%)

Source: National Treasury, Momentum Investments

In our opinion, Treasury has missed an opportunity to take a tougher stance on taxes this year, but they have left the door open to implementing more burdensome tax hikes in upcoming fiscal years, including ongoing limited relief for fiscal drag, increasing marginal personal income tax rates or introducing new personal income tax brackets.

Government acknowledges that a key risk to their borrowing programme is the re-pricing of government debt at a higher level.

Treasury highlights that higher interest rates, rising inflation and the significant depreciation in the exchange rate, partially offset by higher cash balances, have resulted in higher debt levels. The gross debt to GDP ratio is expected to peak at 51% of GDP by FY2017/18 (1.6% higher than projected in the October 2015 medium-term budget), while the peak in the net debt to GDP ratio deteriorated by a further 0.8% over the corresponding period (see chart 5).

Financial market performance

Global markets

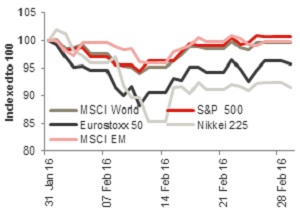

World stock markets moved sharply lower over the first half of the month on the back of growth risks and rising concerns over the stability of the global financial system. Nevertheless, comments by the Organization of the Petroleum Exporting Countries (Opec) energy minister sparked hopes of coordinated production cuts in the second half of the month, spurring oil stocks and leaving world stock markets only 0.3% lower for the month.

Within developed markets, the Nikkei 225 lost 8.5% in February amid uncertainty about the financial system in a negative interest rate environment and a jump in the value of the yen. This was followed by a 4.3% dip in the Eurostoxx 50 Index, while the S&P 500 Index gained 0.7% over the corresponding period (see chart 6).

In line with a 2.2% fall in commodity prices, the MSCI Emerging Market Index ended the month 0.2% weaker. The MSCI Emerging Markets Asia Index was the weakest performer across EM (-0.8%), while the MSCI Latin America Index ended the month 2.2% firmer. The MSCI Emerging Markets EMEA Index inched 0.4% higher over the same time period.

Chart 6: Global asset class returns

Source: Bloomberg, Momentum Investments

Local markets

Budget concerns led the South African equity market (FTSE/JSE ALSI) lower over the first half of February, while weaker Chinese markets and a disappointing meeting held between G20 policymakers limited gains towards month end.

The headline index ended the month 0.6% higher, but masked a stark divergence between the performances of resource and financial/industrial stocks. The FTSE/JSE Resources Index gained 15.6% over February, while the FTSE/JSE Industrials Index and the FTSE/JSE Financials Index lost 2.3% and 1.5%, respectively.

The FTSE/JSE Mid-cap Index gained 6.6% in February, while the FTSE/JSE Small-caps Index ended the month nearly 8% firmer.

The ALBI tracked 0.7% lower in February (SA ten-year yields sold off by 19 basis points), while strong gains (c.3.6%) were noted in listed property over the month. SA cash ended the month marginally higher (+0.5%), followed by a 0.3% gain in inflation-linked bonds.

The rand experienced significant intra-month volatility, partly owing to the anticipation of the national budget, but was little changed over the month. The rand ended February around 0.2% weaker against the US dollar and 0.2% firmer against the euro.