Economic and market snapshot for April 2016

Sanisha Packirisamy, Economist at MMI Holdings.

Herman van Papendorp, Head of Asset Allocation at Momentum.

Global economic developments.

United States (US)

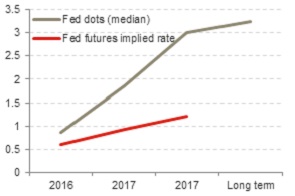

Federal Reserve (Fed) median interest rate expectations shifted closer to market pricing, but large gap remains

Dovish rhetoric by major central banks has helped investors regain risk appetite, aiding a recovery in emerging market (EM) assets. The European Central Bank (ECB) has extended quantitative easing and long-term refinancing operations, as well as recently introducing corporate bond purchases, in their latest attempt to roll out more anti-deflation artillery. Meanwhile, the Bank of Japan (BoJ) cut interest rates into negative territory and will likely expand their quantitative easing programme in upcoming months given anaemic economic growth forecasts and subdued inflation prints. The US Fed also surprised markets this year, signaling that rates in the US would remain lower for longer, which has caused a reversal in the US dollar’s appreciating trend.

Chart 1: Divergent interest rate views (%)

Source: Bloomberg, Momentum Investments

Though the Fed has talked down their own dot plot (expected path of US short-term interest rates), the Fed and the market remain far apart on their opinion of where the federal funds rate will end this year and next (see chart 1).

After taking a breather, a resumption in US dollar strength against the euro is likely given the divergences in growth and monetary policy stances between the two regions. The market anticipates a rosier growth outlook in the US for the remainder of the year (following a poor start to 2016) and rising inflation pressures as the labour and housing markets continue to strengthen. This should allow the Fed to raise rates twice this year, while the ECB (and BoJ) are set to maintain an easy monetary policy bias well into 2017 on discouraging growth and inflation prints.

The robust recovery in EM assets lost steam in April suggesting that the asset class remains vulnerable to a potential turnaround in the US dollar and renewed concerns about Chinese growth and currency prospects.

Eurozone

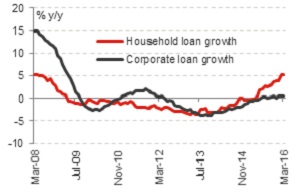

Accommodative monetary policy stance and improving loan growth to support modest recovery

The central bank’s April 2016 quarterly bank lending survey pointed to an improvement in loan supply conditions for firms and a continued increase in loan demand across all loan categories on the back of monetary policymakers’ stimulus efforts. Euro area banks reported a further net easing of credit standards for loans to corporates (with a net 6% of banks reporting less stringent criteria compared with 4% in 4Q15).

In the household sector, credit standards on consumer credit and other lending to households returned to a net easing position in 1Q16 (a net 3% of banks reported easier lending conditions from a net balance of 1% reporting stricter criteria in 4Q15). However, lending standards for household mortgages tightened as a result of a change in European rules.

Credit access is likely to improve in upcoming months as ECB interventions continue to encourage banks to extend loans. The ECB recently cut interest rates to record lows in March 2016 (the ECB’s deposit rate was cut to -0.4% while the benchmark refinancing rate currently trades at zero) and announced a series of Targeted Longer-Term Refinancing Operations (TLTROs). Policymakers also upped their monthly asset purchases from €60 billion to €80 billion.

Chart 2: Slow recovery underway in credit growth

Source: ECB, Bloomberg, Momentum Investments

Meanwhile, previous areas of growth support (including a weaker euro boosting exports and a low oil price benefiting consumers) are fading, suggesting that the onus is now on policymakers to support the fragile growth recovery through monetary and fiscal stimulus efforts.

Japan

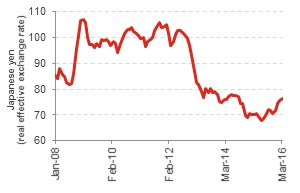

Strengthening exchange rate a risk to an already-weak growth and inflation outlook

The Japanese yen strengthened further after the BoJ kept policy on hold at their April 2016 rate-setting meeting. A firmer yen (see chart 3) has damaged business confidence, with the Tankan Business Conditions survey dropping from 12 index points to 6 since the beginning of the year. Currency strength has also pushed down the rate of headline inflation to -0.1% y/y in March, prompting the BoJ to downgrade their expectation on average inflation (excluding fresh food) for the fiscal year to March 2017 from 0.8% to 0.5%.

Though the BoJ lowered interest rates into negative territory in a surprise move only three months ago, softer growth and inflation forecasts will likely see the central bank either announcing a deeper move into negative rates territory, a ramp up in the current ¥80 trillion a year quantitative easing programme or a change in the composition of asset purchases in upcoming months.

Chart 3: BoJ struggling to keep the yen down

Source: Bloomberg, Momentum Investments

Emerging markets (EM)

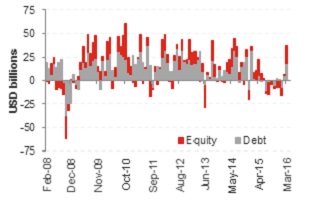

Robust inflows into EM bonds and equities in global risk-on trade

According to the Institute of International Finance (IIF) emerging markets were the recipients of USD36.8 billion foreign portfolio (bond and equity) inflows during March (see chart 4). Although macro fundamentals remained poor across many emerging economies, dovish signals from major developed market central banks and an uptick in economic data surprises in China fueled a risk-on shift in investor behaviour.

Chart 4: Sharp reversal in EM bond and equity flows

Source: Bloomberg, Momentum Investments

Of the USD36.8 billion inflows, USD17.9 billion flowed into EM equity markets. The quantum of equity inflows in March equated to nearly 50% of the EM equity outflows experienced in the second half of 2015. The remainder of the USD36.8 billion worth in EM portfolio inflows in March poured into EM bond markets, more than matching the extent of bond outflows experienced over 2H15.

The recovery in portfolio inflows into the South African bond and equity markets in March 2016 was in line with the reversal in flows into emerging markets. According to JP Morgan, SA experienced inflows of USD1.6 billion in March, amounting to roughly 70% of the portfolio outflows endured over 2H15.

Local economic developments

Reserve Bank assesses implications of a sovereign debt rating downgrade to sub-investment grade

The South African Reserve Bank (SARB) has estimated the consequences of a downgrade to below investment grade based on a study of foreign-currency debt ratings data (by Fitch rating agency) for 70 economies. The evidence confirmed that countries with investment-grade ratings have lower borrowing costs than their speculative grade peers. As countries migrate from investment grade into speculative grade, costs do not increase in a linear trend with the curve instead steepening. The SARB suggests that these trends prove that markets attribute less significance to variations within investment grade than they do in the speculative grade zone.

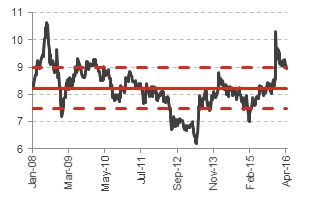

Extrapolating trends across the 70 economies led the SARB to estimate a likely 80-basis point increase in short-term rates and a 104-basis point increase in long-term bond yields (see chart 5) in SA, should the foreign-currency debt rating fall to below investment grade.

The Reserve Bank warned that higher long-term borrowing costs would result in government allocating more spending towards debt-service costs. Moreover, the private sector would also face a higher cost of investment given the link between corporate borrowing costs and the sovereign rating.

The SARB assumes a likely depreciation in the rand against major currencies in the event that foreign investors sold out of their holdings, which would induce further inflationary pressures.

Chart 5: SA ten-year government bond yield (%)

Source: INET BFA, Momentum Investments

Financial market performance

Global markets

World equity and commodity markets continued to recover off their mid-February lows in April 2016 driven by accommodative policies by global central banks and improved risk sentiment. The VIX volatility index rolled back from 27.8 points in mid-February to 15.7 points in late-April, but remained relative steady from a month ago, while commodity prices rose by a further 8.5% in April.

The MSCI All Country World Index (ACWI) increased by 1.5% in April on the back of a firm performance in European stock markets. The Eurostoxx 50 Index gained 1.5% during the month, followed by a mild 0.4% uptick in the S&P 500 Index on the back of disappointing corporate results. The Nikkei 225 Index slipped towards the end of April and ended the month 0.6% lower.

Concerns over the longevity of the EM rally have emerged as gains across EM equity markets fizzled out in April. The MSCI Emerging Markets Index inched 0.5% higher in April, led by gains in Latin America (LatAm) and Europe, Middle East and Africa (EMEA), while Asian bourses were down slightly. The MSCI Emerging Markets Latin America Index increased by 6.0% in April, followed by a 3.8% rise in the MSCI Emerging Markets EMEA Index, while the MSCI Emerging Markets Asia Index lost 1.3%.

Local markets

The performance of the underlying sectors diverged markedly across the local equity market in April. The FTSE/JSE ALSI ended the month only 1.7% higher, largely supported by the 13.5% jump in the FTSE/JSE Resources Index. After gaining 11.5% over March, the FTSE/JSE Financials Index lost 0.3% in April, while the FTSE/JSE Industrials Index fell by nearly a percent over the corresponding period.

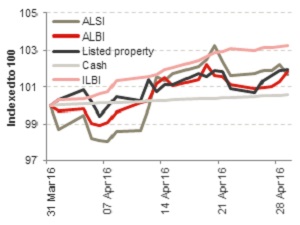

Chart 6: Local asset class returns

Source: Bloomberg, Momentum Investments, data up to 29 April 2016

Small-caps outperformed mid-caps in April. The FTSE/JSE Mid-cap Index gained 4.6% during the month, while the FTSE/JSE Small-caps Index ended the month 5.9% firmer.

The ALBI increased by 1.9% (ten-year bond yields ended April at a similar level relative to a month ago, selling off towards month end after a rally from 9.2% to 8.8% in the middle of the month). Listed property posted a marginal gain of 2.0%, leaving cash as the worst performing asset class in April (+0.6%). Inflation-linked bonds, on the other hand, were the best-performing asset class, gaining 3.3% over the same time period.

The South African rand’s gains tapered off in April relative to its marked appreciation in March as the US dollar reversed nearly a percent of its prior losses against the euro. The rand appreciated marginally over the month in line with a firmer Argentine peso, Colombian peso and Russian rouble. The rand ended the month 2.7% firmer against the US dollar and 1.6% stronger against the euro.