Deterioration in 2Q16 consumer confidence

Sanisha Packirisamy, Economist at Momentum.

Herman van Papendorp, Head of Asset Allocation at Momentum.

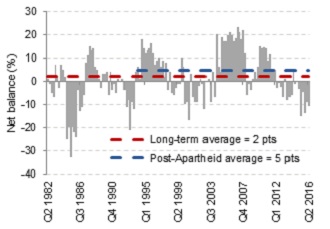

The Bureau of Economic Research’s (BER) Consumer Confidence Index (CCI) fell two points from a reading of negative 9 index points in the first quarter of the year to negative11 points in 2Q16.

Consumer confidence dips again

(see chart 1) due to all three contributing sub-indices (including economic prospects, expectations about personal finances and the appropriateness of the current time to purchase durable goods) declining during the quarter. The BER attributes the weaker reading to elevated political uncertainty, a limited expansion in public sector employment, social unrest, surging food prices and previous hikes in the domestic interest rate. Tshwane violence and Britain’s vote to exit the European Union would not have been captured in the second quarter confidence print seeing as the survey was conducted between 17 May and 10 June 2016. As such, consumer confidence is likely to remain in the doldrums into the third quarter of the year.

Chart 1: Consumer sentiment printing in negative territory for a sixth consecutive quarter

Source: BER, Momentum Investments

Confidence gap between high- and low-income earners widens

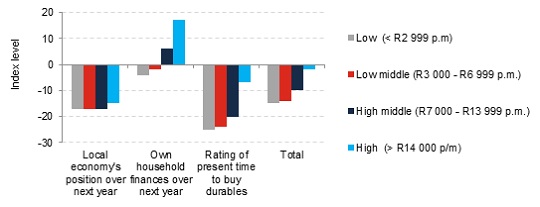

Although confidence levels remained in negative territory for all income-earning groups, sentiment only deteriorated in the lower-income earning categories. Low-middle income earners experienced the largest fall in confidence, while consumers surveyed in the high-income earning category observed the largest positive quarterly change in consumer confidence. This resulted in the gap in confidence between high- and low-income earners widening from 2 index points in the first quarter of the year to14 points in 2Q16.

Chart 2: Low-income earners are under increasing pressure

Source: BER, Momentum Investments

The BER suggests that the divergence in sentiment across the various income-earning households is a function of real disposable income growth and wealth effects. Whereas low-income households are facing a weak job market (particularly in the traditionally low skilled/lower-income occupations) and soaring food costs, the fact that SA’s sovereign rating remained in investment grade following Standard and Poor’s credit rating review in early June resulted in wealth gains for higher-income earners exposed to the equity market. This may have led to a further rise in high-income households’ expectations of their own personal finances over the next year (see chart 2).

Consumer spending to remain under pressure

Suppressed consumer sentiment mirrors the sharp deterioration observed in retailers’ confidence levels, which crashed to a 15-year low in 2Q16 as poor demand and rising input costs dented profitability levels further. In particular, we expect low-income earners to remain under pressure in the near term in response to a further expected rise in food inflation, poor job prospects (particularly in low-skilled areas of the economy) and more stringent lending conditions. Muted credit growth appears to be a function of both demand and supply. Banks are likely restricting the supply of credit as they remain cautious on the economic outlook, while high levels of indebtedness are curbing demand for additional household credit. The latest 1Q16 National Credit Regulator (NCR) data pointed to a decline in the number of consumer credit applications in the first quarter of the year as well as a rise in the rejection rate related to new credit applications. Within overall household consumption expenditure, we expect discretionary goods spend to take the biggest knock. Consumers across the income-earning spectrum currently view the current time as inappropriate to buy durable goods (furniture and appliances), while semi-durable retailers experienced the largest dip in confidence levels (from all retail categories) in the second quarter of the year, boding ill for clothing and footwear spend in the upcoming quarter.