Currency depreciation is Having mixed effects on Latin American Economies

The perception among investors that the US economy will outperform other economies in the coming months has caused an appreciation of the US dollar against other currencies. In Latin America this is no different, but a second factor is at play, this region is a major producer of commodities. Trade within the main Latin American countries has been hit by lower international commodity prices.

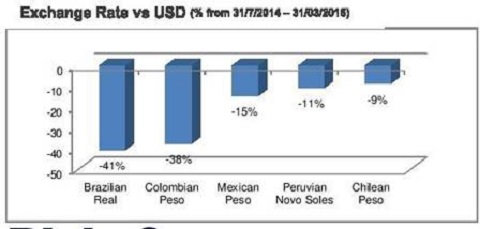

The five main free floating currencies in the region have depreciated (see chart above): the Brazilian Real, the Colombian, Chilean and Mexican Pesos and the Peruvian Novo Soles.

The fall was notably stronger in Brazil (-41%) and in Colombia (-38%), due to the effect of lower oil prices. A weaker currency tends to improve the manufacturing sector’s competitiveness by decreasing the price of the exported products and exporters may postpone sales if they expect another strong fall.

In Brazil, industry reported a contraction in the 12 months to February 2015. Manufacturing exports reduced by 10% from January to March 2015 compared to the same period in 2014.

In Colombia, the manufacturing activity decreased by 2.5% in January 2015 Y-o-Y and exports shrank by 8.5% in the first two months of 2015. In the opposite direction Mexico, whose currency reported the third highest volatility, observed a robust manufacturing industry.

Since the implementation of the Nafta in 1994, the country has increased productivity. The transport infrastructure is weak (ranked at 65 from 144 countries of the World Economic Forum Survey), but it is still better than other major economies in Latin America (the exception is Chile positioned at 49).

Overshooting in exchange rates also reveals fears of financial stress for countries with high external debt or with a corporate segment that is highly exposed to external liabilities. In the 80´s Latin America was strongly associated with public foreign external debt and moratorium cases.

However, nowadays none of these countries hold a high dependence on foreign financing. Taking the private sector into account, entrepreneurs in the region seem to have learned from the subprime crisis triggered in 2008.

Particularly in Brazil and Mexico the corporate segments were significantly impacted. Since then regulatory changes have been made to address the risk of currency mismatch. Additionally, unlike the 2008 episode, the recent weakening was expected for some time.

A study of the Brazilian Central Bank shows that total corporate foreign currency denominated debt stands at 17.1% of GDP, of which 6.1% are export companies (which have a natural hedge), 3% had currency cover in local markets, 5.1% are multinationals and only 2.9% have no hedge.

In Colombia the ratio represents 11% of GDP. In Mexico a central bank study based on listed companies revealed that they have issued 88% of the total bonds abroad. Despite this, it estimates that a 30% currency depreciation would equate to only 5% of the equity, considering the hedging made by the companies.

Risks

The US dollar appreciation is not expected to prompt turmoil in foreign debt, neither in the public or private sectors. Latin American free floating countries were able to considerably increase their international foreign exchange reserves stock in recent decades against a backdrop of high commodity prices that had been in force until recently. In this manner, even if there was an unexpected event of currency mismatch, central banks would be able to help the corporate segment.

The main risk involves industries that depend on imported raw materials, mainly Brazil and Colombia (where depreciation has been stronger). In Brazil the agro segment depends on imported fertilisers. The Colombian agro segment has also been impacted for the same reason, in addition to the auto industry, textile and clothing.