Coface say EuroZone bankruptcies to persist

Emerging economies vulnerable to external shocks.

The situation of advanced countries is delicate. While the systemic financial crisis in the Eurozone is receding, the credit crisis affecting European companies is far from over. Coface forecasts that the Eurozone will remain in recession in 2013. Sluggish domestic demand is unlikely to be offset by exports.

The outlook is more favourable in the US and in Japan. But concerns are still lingering on the policy-makers’ ability to reduce the fiscal deficit in the US and in Japan, on the evolution of exports to China.

The outlook is far more encouraging in emerging countries. They proved resilient in 2012 with growth expected to reach 4,8%. According to Coface’s forecast, it is likely to accelerate over 5% in 2013, thanks to the dynamism of domestic demand and the implementation of reactive and prudent economic policies. However, these good figures should not mask vulnarabilities.

Advanced Countries Prolonged Crisis in the Eurozone, a Shock to Growth in Emerging Europe

In the context of a Eurozone crisis and given the rate of company bankruptcies, the credit risk is likely to increase in France, Spain and Italy. This trend reflects businesses’ weak financial situations, except in Germany, although there bankruptcies turn out to cost more when they do occur. In contrast, American and Japanese companies have a more favourable profile, but confidence remains a problem, as evidenced by the volatility of SME confidence indicators in both of these countries.

European companies face a degraded macroeconomic environment…

The weakness in domestic demand largely explains the expected contraction in the economic activity of the Eurozone in 2013. Firstly fiscal adjustment efforts restrict public demand and will therefore have a negative impact – even more negative than expected - on growth. Secondly, household consumption, despite a comfortable level of net wealth in some countries, will be restricted by the social impact of internal devaluations stemming from declining real incomes and the deteriorating labour market.

The significant steps made by European institutions have helped calm the markets, but have not yet been felt in the real economy. Thus, investor confidence, which is a leading indicator of GDP growth, will remain at levels consistent with a recession in the next six months.

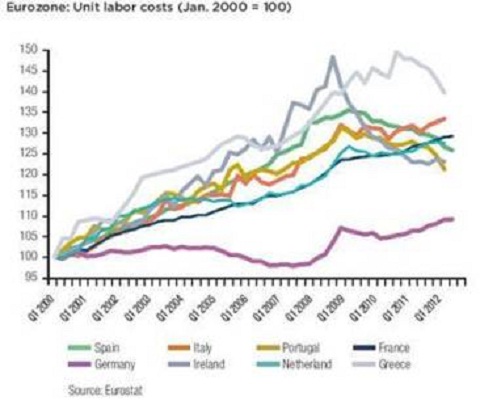

Exports will play a limited role given the low share of exports to emerging countries and competitiveness problems. Indeed, some countries such as Spain, Portugal and particularly Ireland have started a process of adjusting their cost competitiveness. But this is not the case in France and Italy.

It is important to note that cost competitiveness does not necessarily result in price competitiveness. Companies are trying to rebuild their margins and accumulate cash to repay debt rather than invest. The last element explaining the limited contribution of exports to growth is the fact that emerging countries tend to implement protectionist measures to protect their own industries.

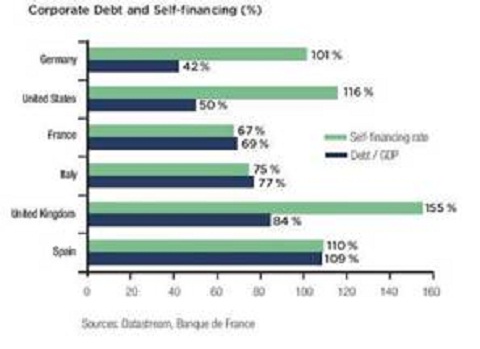

The situation of companies differs greatly from one country to the next. In Spain and in the United Kingdom, companies have high profits but are also highly indebted. Their profits are therefore primarily dedicated to repay debt. French and Italian companies have a much lower level of debt but the weakness in their self-financing and profit levels makes them vulnerable. By comparison, American and German companies are more resilient with high profits and a high self-financing rate on a low level of debt.

In terms of business sectors, the credit risk increased in distribution, food processing and services, sectors sensitive to household consumption. Coface also recorded payment incidents in the metals sector, which reflects the difficulties in the automotive and construction sectors. But the economic downturn is not solely responsible for these sectoral risks. Most of these sectors have long-term structural weaknesses that the economic situation has merely revealed. One case stands apart: that of German companies which have proven highly resilient to economic conditions due to their comfortable financial situation and export dynamism since 2010.

Credit risk is deteriorating in France and in Southern Europe

The way Germany managed to stay ahead during the crisis contrasts sharply with the French situation where the number of company bankruptcies has been double that of Germany since 2007. It is true that, when they occur, German bankruptcies are generally more costly but in France, there is an increasingly high financial and social cost.

This worrying dynamic is explained by French companies' high dependence on household consumption. In 2013, Coface expects a slight contraction in private spending, which should increase the number of bankruptcies in France.

Spanish and Italian companies have also been weakened. This situation is explained in Spain by the purging of the debt and, in the short term, by the banking reform underway. In Italy, electoral uncertainty and the contraction in bank credit since last summer should result in increased credit risk.

In the United States and in Japan, companies are in a better position, but SME confidence indicators show that concerns persist. In the United States, they are concerned about political gridlock around the budget. In Japan, confidence has been affected by the problem of exports to China, a key driver of growth.

After last October’s decision to place a negative watch on the assessments of a few core countries of the Eurozone (Belgium, France, the Netherlands), Coface has lowered its assessments on Italy and Spain, and put the assessment of Japan under negative watch.

Emerging Countries Growth is Accelerating but Vulnerabilities Remain

Compared with the mixed but globally sluggish picture of advanced economies, the evolution of emerging countries may appear enviable. But despite strong growth, emerging countries remain vulnerable to external shocks that are felt through two channels, trade and finance. There is a negative correlation between the growth rate in emerging countries and their rate of openness. The emerging countries in Europe, which are very open and dependent on Western European demand, are suffering from the prolonged crisis in the Eurozone.

As for the Asian countries, they continue to show very dynamic growth, whatever their degree of openness. The Philippines and Indonesia remain relatively closed, but are faring remarkably well thanks to high domestic demand and expatriates’ remittances. Thailand and Malaysia, which are very open countries, had to resort to counter-cyclical economic policies to mitigate the impact of the global slowdown on their activity.

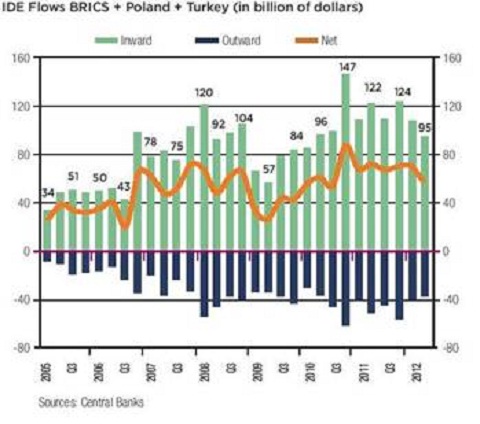

The transmission of the European crisis through the financial channel is more complex. Foreign direct investment has decelerated but remains substantial and loans from European banks have fallen but have not collapsed. We are clearly witnessing a gradual withdrawal of funding from European banks, especially in emerging Europe and the CIS.

Development of domestic financial systems under control

In order to reduce their dependence on external funding, emerging countries are trying to develop their own financial markets, with varying success. There are three groups of countries. First, there are those with oversized credit markets (around 125% of GDP), such as China and Vietnam. Here credit certainly plays a role as a significant growth driver, but the rate of non-performing loans on banks' balance sheets has grown. The challenge for these countries is twofold: to restrict the size of the market, but also to improve lending practices.

The second group consists of countries such as Turkey, India or Russia, which still have a moderate stock of domestic credit (around 50% of GDP), but where expansion has been very rapid in a catching-up dynamic. Paradoxically, although the market is weak, credit bubbles may develop.

The third group of countries consists of economies marked by undersized credit markets (less than 20% of GDP) such as Argentina and Algeria, which are characterised by an investment rate which is too low and an underdeveloped private sector.

When domestic credit is insufficient, the companies fund themselves in international markets. A too rapid and high debt level carries greater risks so it is generally undertaken in foreign currencies by a small number of large firms, as is the case in India.

A quasi-sovereign risk to be monitored

A weak sovereign risk must not be confused with the risk on public sector entities. Indeed, since the 2009 crisis we have seen a number of defaults in quasi-sovereign public entities, which were heavily indebted (BTA in Kazakhstan, Dubai World in the United Arab Emirates), where state support seemed to have been acquired. Borrowers and lenders have played on the ambiguity of this support. However, emerging countries that have become good sovereigns are not guarantors for quasi-sovereign entities if they have not given a formal guarantee.

Circumventing economic policies

Furthermore, certain economic policies do not always work effectively, despite a comfortable financial position and a very low sovereign risk. The case of China is quite telling. The authorities are trying to reverse the growth model where investment is oversized and household consumption underrepresented, a trend which began in the 1990s.

One of the ways is to control access to credit, which is almost in its entirety devoted to investment and, in particular, to the financing of small non-viable players. Bank credit is now under control but businesses and households have succeeded in circumventing the directive of the central authorities by using ‘shadow banking’, causing an explosion of poorly-regulated loans at very high rates, which carries risk.

Governance: A burning issue

Governance is the latest risk to emerge. On the socio-political level it is certainly the major challenge that emerging countries are facing today. This issue has become increasingly topical due to the expansion of the middle classes who are more demanding in terms of transparency and the combating of corruption. They ask the public authorities to be accountable for their actions, as in the (Arab Spring) but also in Russia and in India.

As a result, Coface has lowered its assessments for South Africa, the Ivory Coast and India, countries where the central question is not growth, but rather the capacity of political institutions to cope with social change.