April headline inflation print in line with expectations

Sanisha Packirisamy, Economist at MMI Holdings.

Herman van Papendorp, Head of Asset Allocation at Momentum.

Year-on-year inflation dipped to 6.2% in April from 6.3% y/y in March, but increased by 0.8% over the month largely owing to a drought-induced acceleration in food prices.

Temporary dip in headline inflation as a result of statistical base effects created in petrol prices

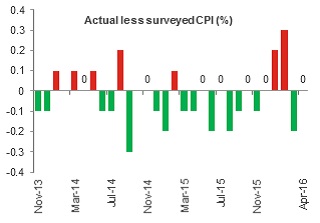

The print came in line with our and the market’s expectations (see chart 1), after factoring in the large base effect created by a hefty petrol price increase of R1.62 in April last year which led to a marginally negative year-on-year rate in petrol inflation in April 2016 despite a steep 6.1% increase in month-on-month terms.

Chart 1: Headline CPI in line with market expectations

Source: Stats SA, Bloomberg, Momentum Investments

April is traditionally a relatively low survey month, with only c.12% of the basket surveyed in addition to the normal monthly surveys. Relative to our own forecasts, the price increases related to food (notwithstanding our expectation of higher food costs given the impact of the drought), non-alcoholic beverages, bank charges and funeral costs surprised to the upside, while hotel prices plunged unexpectedly by 3% over the month.

Food inflation rises more aggressively

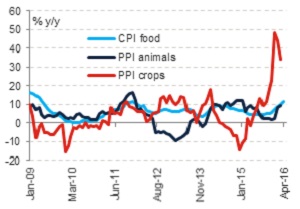

Food prices continued to surge ahead. Agricultural food prices (crops in particular) at the producer level had been signalling a steep rise in prices since 4Q15 which has started to filter through at the consumer level as retailers begin to pass on the cost increases of sharply higher rand food prices (see chart 2).

Chart 2: Crop prices at the producer level signalled a steep increase in consumer food prices

Source: Stats SA, Global Insight, Momentum Investments

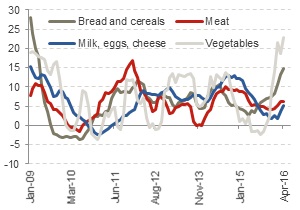

Food inflation rose to 11.3% y/y in April and increased by 1.9% m/m. Bread/cereal inflation has risen to levels last seen in early 2009 thanks to a steep rise in rand maize prices. Further upside risk to food prices is evident based on a twelve-month lead in yellow maize prices (see chart 3).

Chart 3: Further upside risk to food prices

Source: Stats SA, Global Insight, Momentum Investments

The lowest rainfall on record has also had a negative impact on vegetable prices which rose to 23% y/y in April (see chart 4). Although meat inflation remains only marginally above the 6% upper target of the inflation band, a marked increase in PPI animal prices points to a likely rise in meat prices in upcoming months. Farmers are expected to rebuild herds following an increase in culling on the back of soaring feed input costs which is in turn expected to push meat prices higher in due course.

Chart 4: Drought impact drives food inflation higher (% y/y)

Source: Stats SA, Global Insight, Momentum Investments

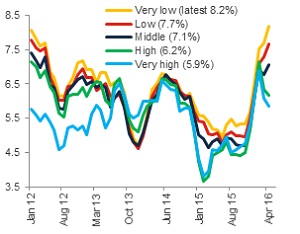

Low-income households hit by rising food inflation

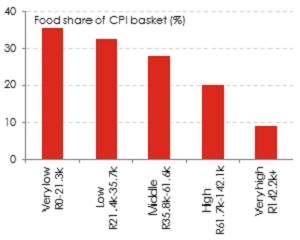

Low-income households (classified as earning under R21 300 per annum) are more heavily exposed to rising food inflation given that over 35% of their basket is allocated to food costs (see chart 5), while less than 10% of the very high-income earners’ (classified as earning above R142 200 per annum) consumer basket is spent on food. It is this discrepancy that has led to a major divergence in consumer price inflation outcomes between the various income-earning groups (see chart 6).

Chart 5: Low-income highly exposed to food inflation

Source: Stats SA, Momentum Investments

Chart 6: Low-income experiencing higher inflation (% y/y)

Source: Stats SA, Momentum Investments

Higher inflation amongst the lower income-earning groups will detract from real disposable income. Together with a bleak employment outlook, low-income earners will continue to face tough conditions for the remainder of the year. On a more positive note, current weather predictions are forecasting a 90% chance of average (neutral) or above-average (La Nina) rainfall in SA later this year, implying that food prices are likely to fall sharply in 2017, providing some inflation relief and real wage growth support to consumers next year.

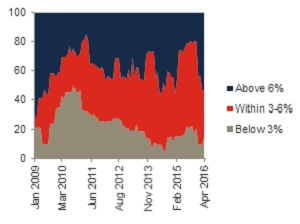

Broad-based price pressures emerging

Over 54% of the consumer inflation basket has experienced price increases above the 3% - 6% inflation target band, highlighting the broad-based nature of the impact of currency pass-through (see chart 7).

Chart 7: Proportion of CPI basket trading below, within and above the 3% - 6% target band

Source: Global Insight, Momentum Investments

Core inflation (headline CPI excluding food, non-alcoholic beverages, energy and petrol) remained at 5.8% y/y in April from a month ago, but increased by 0.3% in month-on-month terms. Non-durable goods inflation increased to 7.2% y/y (+2.1% m/m) in April on the back of higher food prices, contributing to the 1.6% m/m increase in overall goods inflation. Services inflation tracked sideways at 5.7% y/y in April, marginally lower than the previous twelve-month average of 5.8% y/y.

Rising inflation trajectory and stubbornly high inflation expectations point to further rise in interest rates

While the risks of a 25 basis point hike at the upcoming Monetary Policy Committee meeting remains high, we expect the central bank to hold rates steady as they continue to assess the impact of previous monetary policy tightening efforts. The SA Reserve Bank (SARB) raised rates by 100 basis points since 4Q15 (200 basis points since 1Q14) against a fragile economic backdrop as they continued to weigh potential negative effects of interest rate tightening on cyclical growth against the SARB’s mandate of maintaining price stability.

A steeper ramp up in food inflation and increasing evidence of broader-based price pressures, owing to a steep depreciation in the currency on a trade-weighted basis, are indicative of a likely prolonged breach in the headline measure of inflation. The SARB has highlighted the risks of potential currency shocks on an inflation profile that is already expected to track outside the target band in 2016 and most of 2017.

Currency weakness and wage cost pressures have further led to stubbornly high (and rising) inflation expectations by businesses and trade unions in particular. The latest Bureau of Economic Research (BER) Inflation Expectations Survey noted the overall measure surveying five-year inflation expectations remaining at 6.1% threatening further second-round effects of the exogenous shocks to inflation. The further uptick in core inflation in recent CPI prints and the result of escalating selling price pressures being noted in the BER sector surveys suggest the possible emergence of such second-round inflation pressures.

In addition to a rising inflation trajectory and the threat of second-round inflation pressures, a still-elevated current account deficit raises concerns over funding given our reliance on volatile portfolio flows. The need for positive real interest rates further points to the likelihood of additional interest rate rises to the order of 50 basis points over the course of 2H16.