A tale of two recoveries – slow and steady in the US

Last week, US first quarter gross domestic product (GDP) growth was revised downward from -1% to -2.9%. This disappointing number, mostly due to the bad weather and weaker consumer spending, obscured the fact that the American economy’s ‘Great Recession’ ended five years ago in June 2009. The 18-month long recession was the longest and deepest contraction in economic activity since the 43-month long first leg of the Great Depression (1929 to 1933).

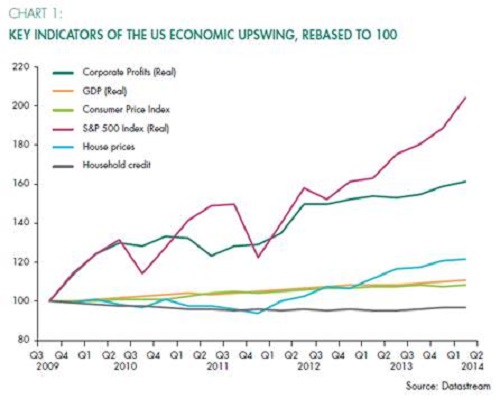

Recovery slow, but profits surge

The massive overhang of the private sector and especially household debt, high and persistent unemployment and untimely fiscal austerity have resulted in the weakest recovery since World War Two. Real GDP is only 10% higher than at the start of the recovery. However, the recovery in real corporate profits has been among the strongest of previous cycles. Real corporate profits are 60% higher than in June 2009. Even during the weak first quarter of 2014, non-financial company profits increased.

At the same time, inflation has been among the lowest (only the upswing that started in 1961 has had lower inflation). The consumer price index (CPI) has risen 9% since June 2009. During this entire upswing phase, the Federal Reserve (Fed) has kept short-term interest rates flat (at near zero levels), an unprecedented occurrence. Despite the record-low interest rates, households have reduced their outstanding debt over the past five years.

Good environment for equities

With a combination of strong profit growth and low interest rates, it is perhaps not surprising that the S&P500 has doubled in real terms since the start of the current upswing phase in the US business cycle. The equity rally started three months earlier, in March 2009, after stress test results showed that the banking sector would survive, and when then Fed Chairman Ben Bernanke noted the “green shoots” of recovery. The equity rally has experienced ups and downs – as is usually the case – most notably in mid-2011 when fears of a double-dip recession and debt default gripped both sides of the Atlantic.

Some investors are concerned that share prices are growing faster than profits and means the price to earnings (PE) ratio is relatively high. But if profits catch up, as is currently the consensus market forecast, the forward PE ratio is not historically high.

US bonds did well too, anchored by zero short-term rates, consistently lower-than-expected inflation and also helped along by the Fed’s US$4 trillion asset-purchase programme. The 10-year Treasury yield fell from 3.5% to a low 1.4% in mid-2012. Though it has now risen to 2.6%, it is still lower than at the start of the year.

House prices have risen 10% in real terms since June 2009, but fell for the first 11 quarters of the economy’s recovery. Despite record-low interest rates, quantitative easing and special incentives from the government to stimulate the property market, it has been the second weakest housing price cycle since 1975.

Given that the housing recovery is fragile, and that consumers are still shell shocked from the financial crisis and housing collapse, the biggest risk to the recovery would be premature interest rate hikes. US headline inflation recently breached 2%, but inflation as measured by the personal consumption expenditure (PCE) index - the Fed’s preferred measure – is still well below 2%. More importantly, the drivers of inflation – wage and household credit growth – remain historically low.

Slow and steady ahead

According to data from the Business Cycle Dating Committee, the official “timekeepers” of US economic cycles, the current recovery is not historically long. Since World War Two, 11 economic upswings have averaged 58 months, with the longest lasting 10 years. There is no reason to expect that this recovery will end anytime soon. A highly accommodative monetary policy, less fiscal headwinds, an improving labour market, slightly better global growth, firming asset prices and households that are more comfortable with their debt exposures are developments supporting US growth into 2015. Fixed investment as a share of GDP is at 20-year low levels, and if it picks up could give the US economy a further boost. So would ending fiscal austerity. This implies that the US economic upswing should continue with subdued but steady growth. Second quarter data so far indicates that the economy recovered a lot of the ground lost in the first quarter. This long but slow growth scenario, combined with low inflation, and accommodative monetary policy, remains a favourable environment for equity investors.