4Q20 GDP: Growth sustained but slow relative to 3Q20

The economy officially grew by 6.3% q/q seasonally adjusted and annualised in 4Q20 following upwardly revised growth of 67.3% q/q (previously: 66.1% q/q) seasonally adjusted and annualised.

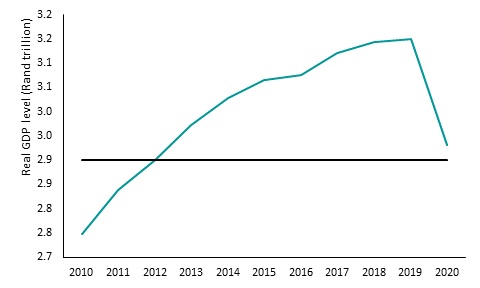

The outturn was marginally higher than our 6.0% q/q estimate and Bloomberg consensus estimate of 5.6% q/q. As measured by real GDP, the economy contracted by 7.0% in 2020 due to the severe impact of the pandemic. Effectively, the economy lost around R219 billion of real GDP in 2020, more than five times the loss recorded in 2009, pushing the economy back to levels last seen around 2012 (Figure 1).

Figure 1: Economy reverted to around 2012 levels in 2020

Source: Stats SA, FNB Economics

Growth outlook: revised cautiously higher

Today’s outcome has led to an upward revision to our forecast; we now expect GDP growth of around 3.5% (previously: 2.9%) in 2021 amid increasingly higher expectations for global growth, which will substantially support exports. The resilient growth outturn in domestic demand components, particularly the upside surprise in gross fixed capital formation (fixed investment) in both public corporations and private business enterprises, despite the pandemic, should provide support to GDP growth in 2021. We nevertheless remain cautious in our growth outlook amid the prevailing uncertainty, the slow roll-out of vaccines and slow progress of economic reforms, including the continued electricity supply disruptions.

Production: broad-based weakness in 2020 but better performance in 4Q20

In 4Q20, eight out of ten sectors of the economy posted favourable quarterly growth rates, with the most considerable growth of 21.1% q/q seasonally adjusted and annualised coming from the manufacturing sector. Within the manufacturing sector, growth was supported mainly by food and beverages; motor vehicles, parts and accessories and other transport equipment; basic iron and steel, non-ferrous metal products, metal products and machinery; and wood and wood products, paper, publishing and printing.

This was followed by the construction sector, which grew by 11.2% q/q annualised, supported by increases in residential buildings, non-residential buildings and construction works. Trade, catering and accommodation increased by 9.8% q/q annualised, supported by retail trade sales, motor trade, catering and accommodation. Transport, storage and communication grew by 6.7% q/q annualised, supported by increased economic activity in land and air transport and communication services.

The agriculture, forestry and fishing sector grew by 5.9% q/q annualised, mainly due to increased production of animal products. The personal services sector increased by 4.8% q/q annualised, supported by fitness centres services and sporting and recreational activities as easing of lockdown restrictions continued in 4Q20. Increased employment in provincial government and extra-budgetary institutions supported an increase of 0.7% q/q in general government services. The electricity, gas and water sector grew by 2.2% q/q, supported by increases in electricity distribution and water consumption.

The mining and quarrying, and finance, real estate and business services sectors contracted by 1.4% q/q and 0.2% q/q respectively. The contraction in mining and quarrying was primarily due to reduced platinum group metals (PGMs) and coal and diamonds, while gold production supported the sector. Meanwhile, the decline in finance, real estate and business services was mainly due to reduced economic activity in financial intermediation and auxiliary activities.

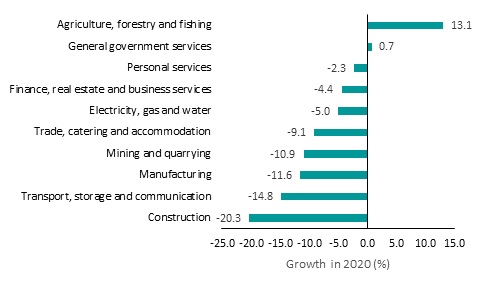

Overall, in 2020, the 7.0% contraction in GDP was broad-based, with eight out of ten sectors posting negative growth rates (Figure 2).

Figure 2: Sectorial growth performance in 2020

Source: Stats SA, FNB Economics

Expenditure: resilient consumption expenditure and upside surprise to fixed investment

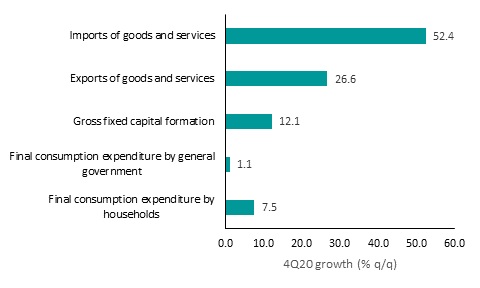

Measured from the expenditure side (excluding residuals), real GDP grew by 6.5% q/q seasonally adjusted and annualised with all expenditure components posting growth (Figure 3). Household consumption expenditure, which contributed the largest to real GDP growth, grew by 7.5% q/q annualised – supported mainly by non-durable consumption expenditure, which posted annualised growth of 10.1% q/q. This was followed by services consumption (5.2% q/q), semi-durable consumption (15.8% q/q) and durable consumption (1.3% q/q).

Figure 3: GDP expenditure quarterly growth rate (annualised)

Source: Stats SA, FNB Economics

Gross fixed capital formation (GFCF) surprised to the upside, posting an annualised growth rate of 12.1% q/q in 4Q20, supported mainly by public corporations’ investment, which grew by 57.4% q/q, and investment by private business enterprises, which grew by 5.8% q/q – contributing 5.7 percentage points (ppt) and 4.1ppt respectively. General government investment grew by 12.0% q/q, adding 2.2ppt to GFCF growth. Within various types of assets:

• Investment in transport equipment grew faster than other assets by 97.1% q/q, contributing 7.3ppt to GFCF growth in 4Q20.

• Construction works investment grew by 9.7% q/q, adding 2.7ppt.

• Investment in machinery and equipment (which includes computers) grew by 3.5% q/q, adding 1.4ppt.

• Investment in residential buildings grew by 14.2% q/q, contributing 1.2ppt, while investment in non-residential buildings grew by 12.8% q/q, adding 0.9%ppt.

General government expenditure grew by 1.1% q/q annualised, supported mainly by quarterly expenditure increases in compensation of employees and spending on goods and services.

The rate of inventory drawdowns slowed in 4Q20, with a change in inventories amounting to an annualised R115.1 billion compared to R144.1 billion in 3Q20, contributing 4.0ppt to real GDP growth. According to Stats SA, large decreases in mining and trade contributed to inventory drawdowns in 4Q20. The large cumulative real inventory drawdowns in 2020 may imply that inventory levels as a share of GDP are now low, effectively requiring some restocking. Nevertheless, the increased input costs, particularly oil prices, may imply moderate or slow restocking in sectors such as mining and manufacturing if viewed as transitory.

Goods and services exports grew by 26.6% q/q annualised, supported by higher commodity prices and rising global demand, which supported the strong trade of vehicles and other transport equipment, precious metals and stones, and base metals and articles of base metals. Meanwhile, imports of goods and services grew strongly by an annualised 52.4% q/q, driven mainly by increased imports of vehicles and transport equipment, base metals and articles of base metals, and machinery and electrical equipment. Nonetheless South Africa reported a trade surplus in the last quarter of the year.