2Q16 Growth concerns rise in response to weaker business confidence

Sanisha Packirisamy, Economist at MMI Holdings.

Herman van Papendorp, Head of Asset Allocation at Momentum.

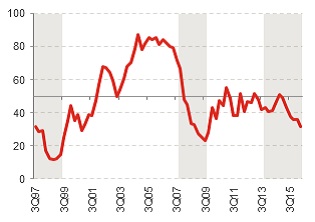

The Bureau of Economic Research’s (BER) Business Confidence Index (BCI) decreased for the sixth consecutive quarter, declining to its weakest level since the fourth quarter of 2009 (see chart 1).

Worrying deterioration in retailer business confidence

The overall index dipped to 32 points suggesting that two-thirds of all respondents (1 700 firms surveyed) viewed business conditions as unsatisfactory in the second quarter of the year.

Chart 1: Business confidence index (>50 = expansion)

Source: BER, Momentum Investments, economic downturns (as defined by the SA Reserve Bank) shaded in gray

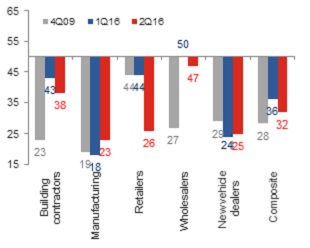

Of the five contributing sectors, the retail sector experienced the sharpest deterioration in business sentiment. The retailer confidence sub-index crashed to 26 points, plummeting by 18 index points relative to the first quarter reading. Although the manufacturing and new vehicle dealer indices improved over the quarter (by 5 and 1 index points, respectively), sentiment improved from a low base and as such these sub-indices remain significantly below the critical 50 level separating an expansion in activity from a contraction (see chart 2). The fact that confidence levels for new vehicle dealers and retailers are now weaker than where they were in the depths of the global financial crisis highlights the stress that SA consumers are currently facing. In addition to weaker domestic demand, rising input costs have contributed to the headwinds facing consumer-related sectors.

Chart 2: Business confidence index by sector (>50 = expansion)

Source: BER, Momentum Investments

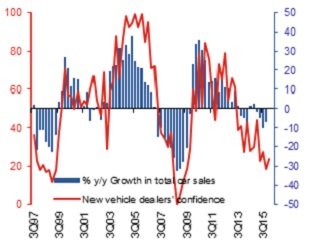

Growth in new car sales likely to remain under pressure

Confidence levels for new vehicle dealers inched higher to 25 index points in 2Q16 from 24 points in the first quarter of the year (see chart 3). The National Association of Automobile Manufacturers of SA (Naamsa) has warned that subdued economic growth, double-digit new vehicle price increases (estimated between 10% and 15%), credit availability and further possible interest rate hikes would exert downward pressure on new vehicle sales. Naamsa estimates that (new) passenger car sales could decline by 9% for the year as a whole following a negative 10.4% rate on a year-to-date basis.

Chart 3: Negative growth in new car sales likely to persist in the near term

Source: Global Insight, Stats SA, Momentum Investments, data up to 2Q16

Downbeat retailers

Retailer confidence weakened to 18 index points in 2Q16, the weakest level since the final quarter of 2000 (see chart 4). According to the survey results, the BER attributes the plunge in confidence to a decrease in turnover. Sales volumes remained weak into the second quarter of the year while many retailers were unable to hike selling prices to the same extent as they did in 1Q16 in an effort to protect volumes. The outcome of the wholesaler survey pointed to some resilience at the wholesaler level as wholesalers exhibited more pricing power and did not have to scale back selling price increases to the same extent as retailers.

Chart 4: Retailers feeling the pain

Source: Global Insight, Stats SA, Momentum Investments, data up to 2Q16

Weak operating environment for manufacturers

Though manufacturing confidence increased by 5 points in 2Q16, the index remained deep in negative territory at 23 points. The survey results suggest that manufacturers are being hurt by poor domestic sales volumes, rising inventory levels and an inability to fully pass on price increases in both domestic and external markets. The global manufacturing Purchasing Managers’ Index (PMI) declined steadily from 52.8 points in February 2014 to 50 points in May. Anaemic global manufacturing output signals weak demand on a global scale which has hindered further export gains for SA manufacturers despite a sharp depreciation in the exchange rate (18% on a trade-weighted basis) over the past year.

Subdued environment for fixed investment and GDP growth overall

Lacklustre business confidence reflects falling growth in corporate profitability, downbeat domestic demand and elevated economic policy uncertainty. As such, private fixed investment spend is unlikely to stage a meaningful recovery over the next year. With consumers facing increasing headwinds (including a deceleration in real disposable income growth, dismal employment growth and rising interest rates), overall domestic demand is likely to remain under pressure well into 2017. Moreover, an inability to raise export selling prices and muted global demand will likely limit the export sector’s contribution to overall GDP growth this year. We expect a marginal improvement in GDP growth from around 0.5% this year to above 1% in 2017 as (business and consumer) sentiment improves on a rosier outlook for emerging markets. We anticipate a correction in the demand-supply imbalance in commodities in late 2017 to drive commodity prices higher, leading to an improvement in growth conditions for net commodity-exporting countries.