2016 Christmas sales outlook – how will embattled households fare?

Luke Doig, Senior Economist at Credit Guarantee Insurance Corporation.

“Pray – for rain and much more!”

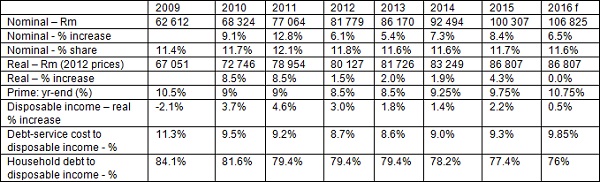

The nominal and real growth in December 2015 retail sales of 8.4% and 4.3% respectively (2014 = 7.3% and 1.9% resp.) was ahead of our expectations as tills ran up a total in excess of R100bn in monthly sales for the first time. Increasing pressures on household spend as economic growth has ebbed and amidst rising fuel and food prices presages a disappointing year-end outcome.

Evidence of the stress on consumer pockets is shown by the contraction in real demand (Gross Domestic Expenditure) of 1.2%% year-on-year in the first half of 2016 (6.5% nominal) while real growth of just 0.8% (6.7% nominal) was seen in final consumption expenditure by households (FCEH). The lack-lustre growth performance of the economy was reflected in weak big-ticket spend as the real growth in sales of durable goods (vehicles, furniture, appliances and electronics) declined significantly (-8% in real terms in the first half of 2016). Semi-durable sales (clothing, footwear, household textiles, tyres and vehicle parts) held up well although stresses may also begin to appear in this segment. However, these segments accounted for just 7.6% and 8.2% of current FCEH in the first half of 2016 respectively. Notable is the intense pressure on non-durable spend (essentially food and power/fuel; 39.6% of FCEH) with real growth of just 0.9% in the first half of 2016 with the 8.5% nominal growth in this category reflecting food inflation. Spending on services (rent, medical, transport and communication; 44.5% of FCEH) has held up well, with real growth of 2% in the first half of 2016.

Final consumption expenditure by households (FCEH): 1st half 2016 vs 1st half 2015

![]()

Source: SA Reserve Bank Quarterly Bulletin

Strike activity has been far more muted to date which implies less lost wages. Retail sales in the first eight months of 2016 are 8.2% higher in nominal terms and 2.2% in real terms with the strain in big ticket items noticeable. Furniture and appliances have shown a contraction in nominal and real terms of 3.4% and 6.8% respectively over June-August 2016 compared to the same period last year.

Petrol and diesel prices are currently running at an under-recovery of 47c/l and 65c/l respectively and price hikes of that magnitude will be a bitter pill to swallow following this month’s hike 44c/l and 23c/l respectively. This will take prices above the levels of R12-40/l for petrol and R10-81/l for diesel that prevailed during December 2015, obviously dependent on what oil price and currency movements occur during November.

As growth has ebbed, so has growth in real disposable income. GDP growth of 1.6% and 1.3% in the previous two calendar years saw disposable income of households rise by 1.4% and 2.2% respectively. Real disposable incomes are expected to improve by just 0.5% in 2016 and understandably when growth in real disposable income slows, so does that in real consumption expenditure by households. We expect FCEH to barely advance (0.1% real growth) this year.

Affordability and the wherewithal of consumers to weather the economic climate drives consumer spend. Debt servicing costs have risen from a low at 8.6% of disposable incomes in 2013 (from a peak of 13.4% in 2008 when household debt to disposable income was at 85.7%) to 9.3% last year and further to 9.8% in the second quarter of 2016 (saar). While we hope that the SARB will not have to hike rates again this year, its hand may be forced if the Fed hikes, if political wrangling continues unabated and/or if a rating downgrade eventuates. Household debt to disposable income ebbed to 77.4% last year and lower still to 75.1% (saar) in the second quarter of 2016 but many household balance sheets are distressed and higher interest rates would place further strain on consumer spend.

Competition, price consciousness and the commensurate pressure on loyalty are factors that all retailers are facing. In this weak demand environment, promotional activity amongst food retailers for one is evident and more may be necessary to push volumes and clear stocks. Risks in the credit space have seen many retailers shift focus and try to gain momentum in cash sales. This strategy shift is justified given credit extension to households having ebbed to a very sluggish 1.4% year-on-year rate in recent months. Online spending for non-food goods and services is certainly growing and all retailers need to have a presence here in order to offer consumers convenience. Notwithstanding the logistics challenges, those retailers that have mastered this will benefit both this year and increasingly in times ahead.

Over the years, better stock management has seen inventory levels ruthlessly run down with industrial and commercial inventories to GDP falling from 15.8% in 2007 to 12.8% last year and marginally lower in the first half of 2016. The decline in final demand (GDE) of -2.2% in the first quarter of 2016 and -3.3% in the second quarter of 2016 (saar) was to some extent driven by inventory movements. The July 2016 growth in wholesale sales of 1.2% in real terms is further evidence that inventory levels are being managed tightly. Just-in-time ordering dominates and our experience to date is that the extent of large advance ordering is no larger than previously.

After recovering from the trough of 11.4% of annual retail sales in 2009, the contribution of Christmas sales improved to 12.1% in 2011 before ebbing to 11.7% last year. The trend by retailers to shift towards a greater reliance on cash as opposed to credit sales, tighter lending standards and the waning appetite for credit by households implies a further waning in the contribution of credit to Christmas sales.

We are detecting a normal pick-up in volumes in the run-up to Christmas across the food manufacturers and wholesalers and similarly for certain freight operators. The cellular sector is showing steady growth in the normal ramp-up towards year-end but we expect little joy in spending across most other sectors with pressures starting to trickle down into semi- and non-durable spend. Pharmaceutical, medical, cosmetic and toiletry spend may surprise somewhat if current sales trends are maintained.

Most measures of consumer confidence and personal financial health issues justify a cautious stance. Given this guarded outlook, we foresee Christmas sales growing by 6.5% in current prices with no growth expected in real terms. Retailers will need to price very keenly to move stocks and this may see consumers benefit. But the wherewithal to spend remains severely constrained and the current outlook for this Christmas trading season will hopefully be very much on a par with last year’s performance; for that alone we need to be thankful. Retailers are going to have to pull out all the stops if they wish to garner a share of the additional R6.5bn in additional sales expected in December; in a best case scenario that should see monthly sales of almost R107bn.

Table – Christmas retail sales analysis

Source: Stats SA & SA Reserve Bank; CGIC analysis and forecast