Budget better than expected, but not good enough for Moody’s

“Minister Mboweni largely delivered despite the obstacles but may not have done enough to avert a ratings downgrade.” - Johann Els, Chief Economist, Old Mutual Investment Group

“The proposed wage bill spending cuts remain a risk as these still need to be negotiated with unions.” – Johann Els, Chief Economist, Old Mutual Investment Group

A major positive from this Budget is that it shows that Treasury is willing to do tough things, and this will help business sentiment, says Old Mutual Investment Group’s Chief Economist Johann Els.

The focus of this Budget was on expenditure cuts rather than tax hikes — the absence of big tax hikes is good news for long-suffering consumers. However, Els cautions that risks remain around the ambitious plans to cut expenditure on the wage bill as this will still need to be negotiated with unions.

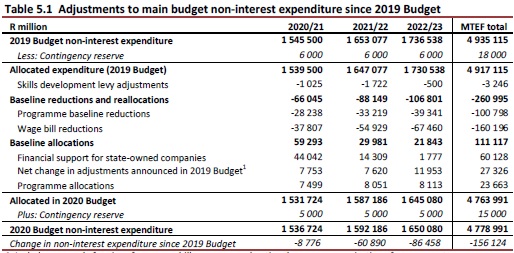

R261 billion in baseline spending reductions were announced by Finance Minister Tito Mboweni, with adjustments on the wage bill penned in at about R160 billion over the medium term.

Highlights:

- Large Wage Bill Expenditure Reductions

- No Net Tax Increases, which means hard-working taxpayers, who earn on average R265,000 a year, for example, will see their income tax reduced by over R1,500 a year

- Cut in corporate tax to below 28% being mulled

- Focus on getting corruption and wasteful expenditure under control

- Government says it will “do whatever it takes to ensure a stable electricity supply”

Some Other Key Adjustments:

- Threshold for property transfer duties being adjusted for inflation - property costing R1 million or less will no longer be subject to transfer duty.

- Plastic bag levy increased to 25c

- -Electronic cigarettes, or so-called vapes, will be taxed from 2021

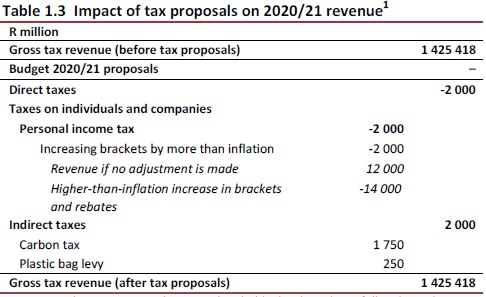

- The carbon tax and other measures will help green the economy and will bring in R1.75 billion over the next few months

- -R80 increase for the old age, disability and care dependency grants to R1,860 per month

- Government has allocated R16.4 billion to settle guaranteed debt and interest on SAA.

- Innovation Fund will be capitalised with R1.2 billion over the next three years

- Industrial business incentives worth R18.5 billion expected to create and retain approximately 56,500 jobs

- R6.5 billion is allocated for small business incentive programmes

- An additional R500 million is reprioritised over the medium term for the department to finalise land claims.

In summary: positives outweigh the negatives – but the jury is out on the wage bill…

• Positives:

o Intension of significant reduction in the wage bill over the next 3 years. (-R160bn)

o No net tax increases

o Deficit to decline over the next three years

• Negatives:

o The large wage bill reduction is not realistic given union opposition.

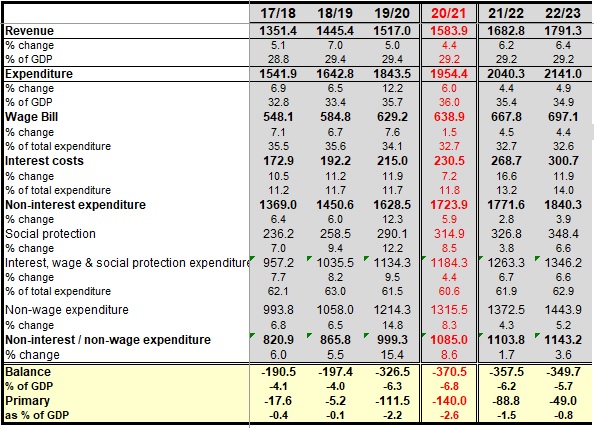

o Deficit to reach -6.8% in 2020/21

o Primary balance (budget balance excl interest payments) remains in deficit

o No stabilization in debt ratio over the medium term

o Further SOE support

Johann Els comments on the Impact of the Budget:

Impact on ratings

Despite the budget’s focus on expenditure reductions over the medium term the still very large deficit, rising debt ratio and weak economic growth will likely lead to a ratings downgrade by Moody’s this year (most likely in March). This is my base case. The risk is that they wait till Nov to see if the wage bill reductions can realistically be achieved. In my view that “overhang” of uncertainty on the market will be more detrimental than the downgrade in March. While S&P and Fitch will also not be ecstatic, they might wait for evidence of wage bill savings…

Impact on markets

The equity markets will likely initially focus on the fact that there are no tax increases coming and that the focus of this budget is on expenditure cuts. But the bond market will likely immediately focus on the very large deficit and rising debt ratio – as well as the risks associated with achieving the wage bill savings.

Impact on the economy

While the very large deficits might seem like this is an expansionary budget, that is not true to the full extent these deficits might imply as expenditure excl wages and interest payments only rise on average by 4.5% pa over the next three years. That is slightly below expected inflation over this period. (Interest payments increase on average by 12% pa over the next three years). Overall though, this budget should help in the process of building confidence in policy makers, as they have made some difficult decisions.

From an inflationary perspective, there will likely be very little impact as the increases in fuel and excise taxes are generally lower than last year. I maintain also that this still a very deflationary environment.

Impact on consumers

While the absence of tax hikes is good for consumers, the reductions in the public sector wage bill expenditure is not positive. However, that reduction might take a while to play out, so the immediate impact likely not too negative. On balance, the budget does not move the dial a lot for consumers in the very short term.

Impact on corporates

No direct impact through any budget-related policy changes, but the strong statements on the public sector wage bill and the need to involve the private sector and create an environment where confidence should improve and enabling the private sector to invest is clearly positive. The envisioned lower corporate tax rate in future is a positive.

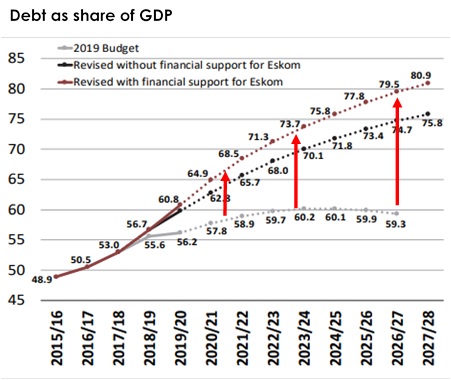

Deficit and debt ratio

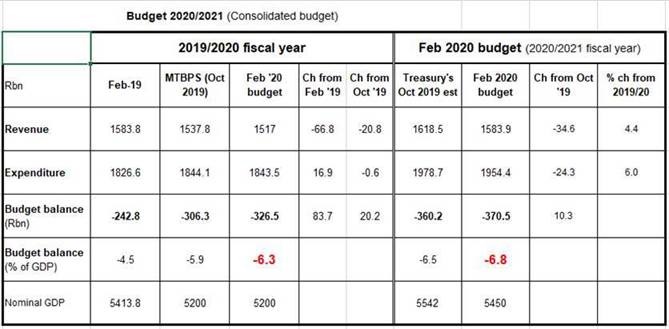

• Deficit ratio revised:

o 2019/20 from -5.9% in Oct ‘19 to -6.3%

o 2020/21 from -6.5% in Oct ’19 to -6.8%

o 2021/22 unchanged at -6.2%

o 2022/23 from -5.9% in Oct ’19 to -5.7%

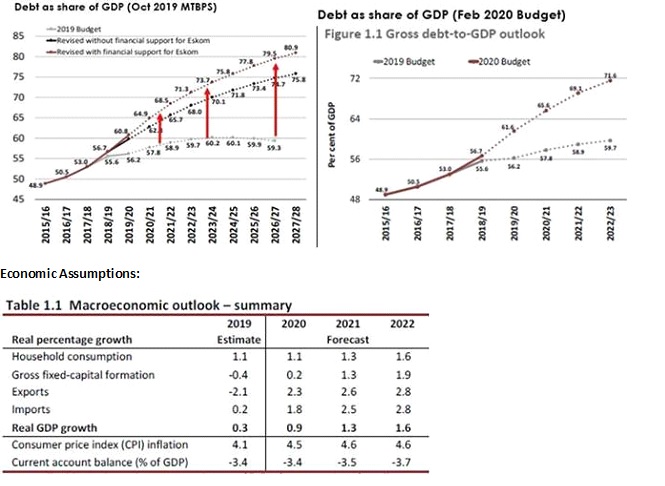

Debt ratio:

Revised slightly worse than last Oct’s estimate. No stabilization seen.

Revenue:

• Current fiscal year:

o Downward revision in revenue: since Oct MTEF -R21bn; since Feb ’19 budget -R67bn

• No significant tax changes in 2020/2021 – no net tax increases

(Treasury officials mentioned in the lock-up that they discussed various additional tax increases, but decided against any given the weak economy)

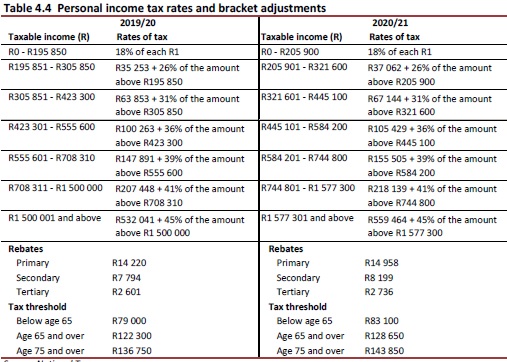

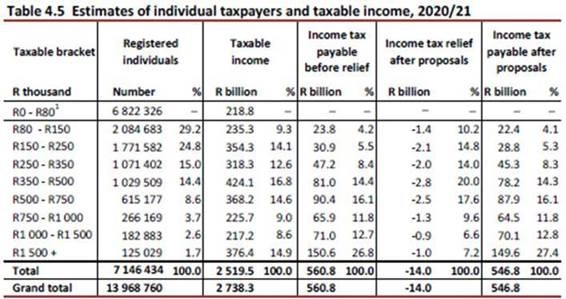

o Individual income tax brackets adjusted by more than inflation (5.2% adjustment vs expected 4.4% inflation).

o This provides for total individual income tax relief of R2bn (vs a potential extra R12bn had there been no tax bracket adjustments)

o Medical tax credits adjusted by less than inflation

o Tax-free savings acc limits adjusted from R33k to R36k

o Broadening corporate income tax base (restrict net interest expense deductions and setting sunset date for tax incentives for airport and port assets). Additional revenue to be used for future corporate tax rate reductions.

o The threshold for transfer duties is adjusted. Property costing R1 million or less will no longer be subject to transfer duty

o Increased excise duties:

? between 4.4% and 7.5% increase in duties for alcoholic beverages and tobacco

o Fuel tax increase: Total of 25c/l from 1 April

? Fuel levy: +16c/l

? RAF levy increase of 9c/l

o Carbon tax increase 5.6%.

o Plastic levies from 12c to 25c per bag.

Expenditure:

- Current fiscal year:

- R17bn higher than Feb 2019 estimate and R0.6bn down from Oct 2019’s estimate

- Very large cuts in baseline expenditure over the next three years

- Gross reduction R261bn

- R100bn downward adjustment in “programme” spending

Mainly conditional municipal and provincial grants (human settlements, infrastructure, transport grants, educational and health infrastructure)

- Wage bill: R160bn reduction relative to base line (-R37.8bn in 2020/21, -R54.0bn in 2021/22 and -R67.5bn in 2022/23)

- Avg wage bill growth over the next three years of 3.5%

- This is obviously a big risk – i.e. that these savings cannot be attained

(Minister mentioned that he has the full backing of his cabinet colleagues. These reductions have been fully approved by Cabinet. This is not a wage freeze, but low increases – thanks to low inflation. Treasury realizes that tough (“extremely difficult”) negotiations are ahead. One of their arguments is some claw-back from past few years big increases. They propose either cost of living adjustments and no pay progression (usually 1.5%) or pay progression and no cost of liv adjustments.

They have no fall-back plan…

- There are also some increases totaling R111bn – mainly extra SOE (Eskom and SAA) support and some programme increases

- Net expenditure reduction of R156bn – obviously heavily exposes to the wage bill risk…

- Other items: better procurement system, merging and consolidation public entities, a proposed law to stop excessive salaries in public entities.

- Expenditure growth rates: (avg over the next three years

- Total: 5.1%

- Wage bill: 3.5%

- Interest bill: 11.9%

- Expenditure excl interest payments and the wage bill: 4.6%