What can we expect from the 2017 Budget Speech?

Dave Mohr, Chief Investment Strategist at Old Mutual.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

This year’s Budget Speech will attract a great deal of attention. In the Trevor Manual years, the Budget was a fairly dull and technocratic affair focused on numbers, such as the extent of tax relief (which was possible in those boom times) and not politics. There was no doubt that Manual had the support of his colleagues in the Cabinet. Furthermore, South Africa’s credit ratings were improving, partly as a result of better fiscal management and also because of a global upgrading cycle on the back of strong growth. The increased attention on the Budget is largely because of the threat to South Africa’s credit rating as we are still in a global downgrading cycle and have experienced a rapid build-up in debt and decline in growth.

The current dilemma

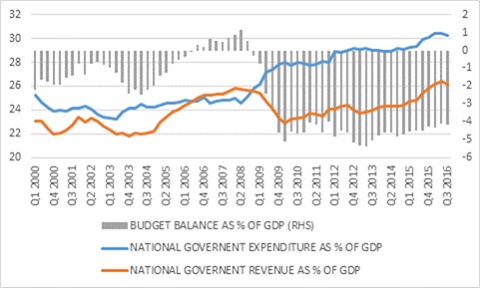

Chart 1 below illustrates how we got to our current predicament. In 2009, tax revenues collapsed as the recession hit. In his first stint as Finance Minister, Pravin Gordhan increased expenditure to help stimulate the struggling economy by borrowing and turning the modest budget surplus into a sizeable deficit (this was text-book countercyclical fiscal policy). Since then, tax revenue and spending have grown roughly at the same pace. However, to close the deficit and reduce debt, tax revenue has to grow faster than spending. Economic growth declined and from 2012 onwards forecasts had to be revised down year after year. The tax revenue assumption in the Budget is based on the growth forecast, but the initial growth estimate has been too high every year since 2012. This meant disappointing tax revenue (especially from companies) and that “fiscal consolidation”, the process of cutting the deficit and stabilising debt, had to be postponed further and further into the future. The alternative - to aggressively increase taxes and cut spending - risked tipping the economy into recession, worsening the debt and deficit ratio in a vicious cycle.

Chart 1: Tax revenue, expenditure and budget balance as percentage of GDP

Source: SA Reserve Bank

Tax trends

Chart 1 also shows that taxes have increased as a percentage of gross domestic product (GDP) over the past few years as GDP growth declined. According to the Davis Tax Committee (DTC), the current ratio of 26% is above the peak of the boom years and higher than the average of OECD countries (excluding social security taxes). A further increase to 27% is projected, but it is debatable whether this ratio can rise much further without killing the metaphorical golden goose. This means that either economic growth needs to accelerate to increase tax revenue at a stable ratio or spending as a percentage of GDP needs to moderate.

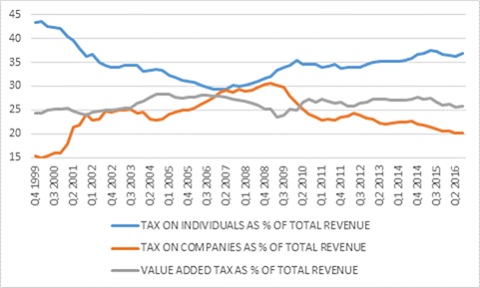

Chart 2 shows important trends in terms of the three main tax items. Company taxes surged to 30% a share of total tax revenue at the peak of the commodity cycle, but fell to around 20% (or from 8% to 5% of GDP). This is the cost of weak growth. Company tax collections could show some improvement as mining profits rebound.

Chart 2: The three main tax items

Source: SA Reserve Bank

The decline in company taxes had to be made up largely by personal income tax (PIT), which has been surprisingly robust growing faster than nominal GDP over the past few years. This was supported by wage settlements consistently in excess of inflation while asset price increases also helped (and a 1% increase in the tax rate in 2015). According to the DTC, the richest 10% of the population (who earn 63% of income) contributes 86% of PIT, and the buoyancy of PIT suggests this segment have done well despite tough times elsewhere. But there are also limits to how much this segment can be squeezed further, as it already funds a third of government spending through PIT and contributes to value-added tax and municipal coffers (not included in the Budget). Value-Added Tax (VAT) collections tend to rise and fall with the economic cycle but is very stable compared to company tax. Growth in VAT slowed down to close to zero in the middle of last year. However, it has rebounded to 7% by December as the economy improved.

The R28 billion question

The Finance Minister is expected to stick to the fiscal consolidation plans as set out in the October Medium Term Budget, but doing so will require R28 billion extra in tax revenue relative to the February 2016 baseline for the coming fiscal year. How he plans to fill this R28 billion gap is probably the key item to watch in this year’s Budget, since there is no luxury of much faster growth.

Funding this gap will be challenging in its own right, but also comes against the backdrop of a broader discussion of where the burden should fall, given the concentration of wealth and widespread poverty. The easiest way to close the revenue shortfall is through VAT. A 1% VAT rate increase could raise around R20 billion extra. South Africa’s VAT rate of 14% is below global standards and has not changed since 1993. However, since rich and poor alike pay VAT, it is not seen as politically feasible to implement an increase at this stage (although it is likely at some point in the future). In contrast, some form of “wealth” tax would be politically popular (and symbolically important given the extreme income and wealth inequality) and is likely at some point in the future. However, it would not raise significant amounts of additional revenue. For instance, increasing the marginal tax rate by 3 percentage points to 44% on taxable incomes above R1 million per year (130 000 taxpayers according to SARS’ 2016 Tax Statistics publication) would increase revenue by roughly R7 billion, assuming no changes in the behaviour of taxpayers.

According to the DTC, estate duty collections have declined in real terms and relative to other taxes and play a small part in the overall tax take compared to other jurisdictions. If the share of estate duties in overall tax revenue increases from around 0.17% to approximately 0.5%, where the UK currently is, an additional R4 billion could be raised. Since the wealthy has larger estates, this would be progressive, but the DTC also noted that difficulties in compliance and administration associated with collecting these taxes might make more aggressive targets unrealistic.

Another approach would be a tax on wealth (assets) as proposed by French economist Thomas Piketty in a 2015 lecture in Soweto. We have limited detail on household assets - as the DTC noted, the asset declaration associated with such a tax would yield valuable information on who owns what - but the Reserve Bank’s estimate of household net wealth for 2015 was R9 384 billion, including property and financial assets and excluding debt. Assuming the distribution of wealth is narrower than that of income with the richest 10% accounting for 80 - 90% of the total, an annual tax of 0.1% on net wealth could yield around R7 billion, but with considerable challenges in administration and compliance. For instance, it would place great strain on the cash flows of these taxpayers, whose wealth might be in illiquid assets. There are very few examples of such taxes in the world, but then South Africa is unusually unequal. It is also clear that the narrow tax base means wealth taxes will not be a game changer in terms of government funding.

The South African company tax rate of 28% is already higher than the OECD average of 24%. The election of Donald Trump and Brexit is expected to result in downward pressure on corporate tax, not just in the US and UK, but also with knock-on effects elsewhere. However, effective company tax rates are always lower as companies engage in various activities to reduce their tax bill (including transfer pricing and base erosion) and Government also offers a number of tax incentives. Emphasis is therefore likely to be on closing any loopholes, and possibly redirecting some of the incentives or subsidies (for instance, the World Bank recently proposed reducing the effective tax burden of manufacturers, which is higher than for mining firms). So changes in company tax rates are unlikely, but since corporate tax revenue is highly sensitive to economic growth, corporate tax revenues are likely to improve.

A combination of sources

Therefore, the Finance Minister is likely to turn to a combination of sources, instead of a big change. A 1% increase in the marginal income tax rate for the 3 million taxpayers with a taxable income of more than R150 000 per year could raise approximately R10 billion rand. Limiting fiscal drag relief could add another R5 billion. The contentious sugar tax (a 20% tax on sweetened beverages) could earn a further R5 billion according to Treasury. A 30 cents increase in the fuel levy from the current level of R2.85 per litre – the same increase as last year - could raise an additional R6 billion. However, financial troubles at the Road Accident Fund could necessitate an increase in the RAF levy, limiting the scope for a fuel levy increase. The voluntary disclosure programme related to offshore investments is expected to net as much as R15 billion over time, but not necessarily in the coming fiscal year.

The DTC’s work continues, suggesting restructuring the tax system to get the optimal mix of tax revenues, balancing growth, equity and efficiency. This might include wealth taxes in the future. A structural increase in state spending – such as the proposed National Health Insurance – could lead to a structural increase in tax revenue as a share of GDP. At the same time, 2% faster growth at a static 26% tax to GDP ratio would yield an additional R17 billion. Therefore, faster economic growth is required to keep Government’s finances on a sustainable path. However, for the time being, it is a case of getting the most out of existing taxes.

Spending under control

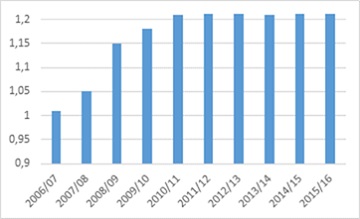

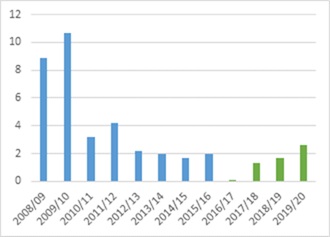

On the spending side of the equation, there is no shortage of competing demands, with calls for free tertiary education still top of mind. Treasury has a reputation for discipline in spending growth (not always matched elsewhere in Government). It is expected that the expenditure ceiling which has done much to build fiscal credibility will be adhered to. Charts three and four from the Medium Term Budget Policy Statement (MTBPS) show that progress has been made in terms of spending discipline as growth in headcount has moderated and real spending growth slowed sharply.

Chart 3: National and provincial headcount, millions

Chart 4: Actual and planned growth in real non-interest spending, %

Source: National Treasury 2016 MTBPS

The most immediate risk is the public sector salary agreement that expires at the end of the coming fiscal year. The proposed nuclear build programme remains a source of uncertainty, but it is unlikely that the Budget will make provision for it.

Unfortunately, fixed investment, rather than salaries, typically bears the brunt of attempts to control spending. Government fixed investment has increased by almost a third in real terms over the past five years, but its share of GDP barely increased from 2.9% to 3.4%.

Implications

Therefore, the deficit reduction as proposed in the 2016 Medium Term Budget - with the budget deficit declining from 3.1% in the current fiscal year to 2.5% over the subsequent two years – is likely to remain on track. What are the implications?

For the economy:

In the short term, fiscal consolidation – higher taxes and slower growth in government spending - is a drag on economic growth, but should not derail the recovery. Longer term, the South African economy needs policy certainty and restructuring of the major state-owned enterprises to ensure that they no longer put strain on the fiscus or hampers economic activity and other growth enhancing reforms. The Budget could give updates on this, but big policy changes seem unlikely before the ruling party’s elective conference at the end of the year.

For consumers:

Tax increases are expected to come from a variety of sources but ultimately involves the taxman sticking his fingers deeper into consumers’ pockets. This will place some pressure on household spending, but declining inflation should offset the negative impact on real disposable income to an extent.

For bonds:

A “good” budget is necessary but not by itself sufficient for securing South Africa’s investment grade rating. Political stability and faster economic growth will also be required. But Wednesday’s Budget is likely to be the first step in maintaining current ratings. Either way, a commitment to fiscal discipline is positive for bonds as it caps the new and therefore supports prices. Fiscal consolidation tends to put downward pressure on inflation, making it more likely that the Reserve Bank will consider interest rate cuts, a further positive for domestic bonds.

For equities:

The company tax rate is expected to remain unchanged, which means that there is no impact on after-tax profits. Small increases in dividend withholding tax or capital gains tax are possible, which will make equities relatively less attractive for local but not foreign investors. Since the R28 billion tax increase was already announced in October last year, it is likely to already be discounted in the share prices of domestically-focussed companies. Sugar and carbon taxes – which will impact a few specific listed companies - are still being debated and the timing of implementation is uncertain. Global market developments are more likely to drive the JSE than the outcome of the Budget Speech.

For the rand:

The rand has appreciated sharply over the past year despite global and local political uncertainty and the risk of ratings downgrades. Commodity prices, sentiment towards emerging markets and expectations for US interest rate increases will more than likely continue to be the primary drivers of the rand. The Budget is unlikely to change this.