SA budget preview – staying the course on fiscal consolidation

Sanisha Packirisamy, Economist at Momentum.

Herman van Papendorp, Head of Asset Allocation at Momentum.

With many indicators of economic development in SA falling short of its debt peer group, broad political/institutional stability and macro policy continuity remain key in preserving SA’s investment grade status.

Sound fiscal management and commitment to reform necessary to allay rating agencies’ fears of political interference

As such, all eyes will be on government’s ability to stay the course on sound fiscal management in the upcoming national budget to be tabled by National Treasury on February 22nd.

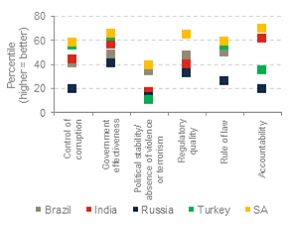

Chart 1: Governance Indicator for SA and its peer group

Source: World Bank, Momentum Investments

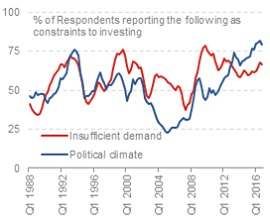

Chart 2: Constraints to domestic investment

Source: BER, Momentum Investments, data up to 4Q16

Rising perceptions of political interference in key spheres of government institutions threaten SA’s macroeconomic performance. Continued political infighting could have a negative impact on SA’s current favourably-perceived governance indicators (see chart 1), the handling of public finances and ultimately the economic outlook for the country. An uncertain political climate has dissuaded corporates from investing in new projects (see chart 2), limiting SA’s ability to achieve a higher trend growth rate.

Necessary combination of tax hikes and expenditure cuts

A lackluster growth environment is a risk to government’s fiscal consolidation path as it may negatively impact on revenue collection. We see slight downside risks to Treasury’s nominal GDP (and hence revenue) forecasts, with our figures projecting a potential nominal GDP undershoot of around 0.5% on average over the next three years based on a more optimistic view on headline inflation.

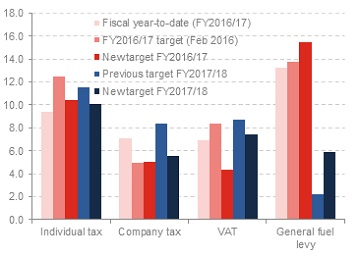

On a fiscal year-to-date basis, corporate income taxes and value-added taxes (VAT) are tracking marginally ahead of Treasury’s revised forecasts, while personal taxes are trailing the target. Growth in corporate income taxes jumped to 7.1% y/y on a fiscal year-to-date (YTD) basis in December 2016, ahead of Treasury’s October 2016 forecast of 5.0%. Although VAT collections are currently running at a pace of 6.9% y/y (fiscal YTD), exceeding Treasury’s target of 4.3%, the sharp downturn in growth in VAT refunds (reflecting delays in the payment of refunds) raises a flag on whether VAT will be able to increase at the same pace in upcoming months. Meanwhile, personal taxes have been increasing at a clip of 9.4% y/y (fiscal YTD), slightly below Treasury’s target of 10.4%. Similarly, fuel levies have been lagging Treasury’s forecasts (13.2% y/y fiscal YTD versus a target of 15.5%).

Chart 3: Tax collection run-rate relative to Treasury’s full-year targets

Source: National Treasury, Global Insight, Momentum Investments, new target = set in October 2016

At the tabling of the medium-term budget, Treasury proposed a balanced solution to fiscal consolidation, including a number of (unnamed) additional tax policy measures amounting to R28 billion in FY2017/18 and R15 billion in FY2018/19. This incorporated announcements made in the February 2016 national budget. Treasury also intends to slash expenditure. It plans to cut the expenditure ceiling by R20 billion in FY2017/18 and R31 billion in FY2018/19.

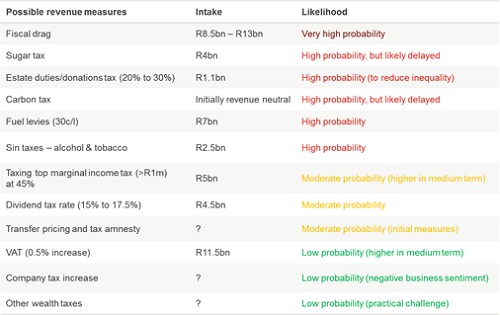

In our view, the bulk of the additional R28 billion in revenue to be raised this year could be collected through renouncing compensation for fiscal drag, as well as by raising fuel levies and sin taxes (see table 1). Although hiking the VAT rate could reap meaningful revenue gains, VAT is deemed to be a regressive tax, falling disproportionately on the poor and middle class, which is exacerbated in a challenging economic climate. Nonetheless, we believe that VAT increases in the future, to finance large-scale expenditure programmes such as the National Health Insurance (NHI) plan, are highly likely. The NHI white paper published in December 2015 suggests that “there are several arguments for favouring an increase in VAT” given that it is “moderate by comparison with the international average (16.4%) and its base is broad, reaching both the formal and informal economies”. The paper notes that VAT “is considered less distortionary in its impact on the productive allocation of resources” as “it does not impact negatively on formal sector employment and does not discourage savings”.

Although lower expected food prices could benefit consumers’ real wages this year, an anaemic jobs outlook and elevated debt levels will continue to burden SA consumers in 2017. Moreover, higher potential taxes (highlighted in table 1 below) could act as a drag on higher real wage growth this year, particularly for middle and higher-income earning groups.

Table 1: Garnering an additional R28 billion in revenue is achievable

Source: Macquarie, PWC, Treasury, Momentum Investments

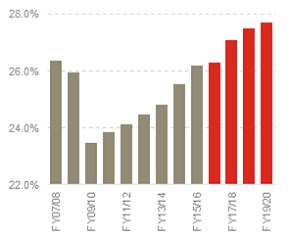

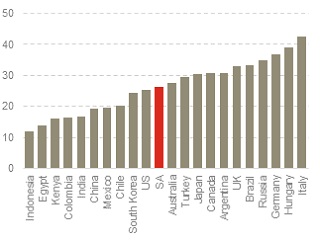

Including all tax revenues, SA’s tax burden (tax revenue-to-GDP ratio) has increased from 23.5% in FY2009/10 to 26.2% in FY2015/16 (see chart 4). According to the Heritage Foundation, this is broadly in line with the ratio in the United States (25.4%) and Australia (27.5%), lower than Turkey (29.3%) and Brazil (33.4%), but higher than India (16.7%) and China (19.4%), see chart 5.

Chart 4: SA’s rising tax burden

Source: SARS, Treasury, Momentum Investments

Chart 5: International tax burden comparison (%)

Source: Heritage Foundation, Momentum Investments

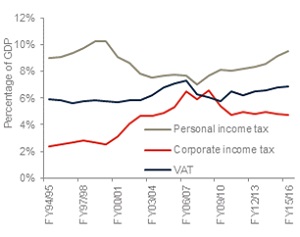

A tough economy has seen the share of corporate income tax as a share of GDP fall from 6.6% in FY2008/09 to 4.7% in FY2015/16. Over the same period, personal income tax as a share of GDP increased from 7.7% to 9.5% and VAT shifted higher from 6.0% to 6.9% (see chart 6). However, despite an unfavourable growth milieu, tax collection has been resilient. The tax revenue buoyancy ratio, which describes the relationship between tax collection and economic growth, has averaged 1.25 since FY2010/11, implying that for every 10% growth in nominal GDP, 12.5% growth in revenue collection could be achieved. However, with moderate average wage settlements, declining wealth gains, anaemic employment growth, a strong probability of bracket creep, weaker import demand and a firmer rand, there is a risk that tax buoyancy rates could decline by more than Treasury’s assumptions over the medium term, leading to a slightly wider than expected budget deficit than projected by Treasury. In its October 2016 medium-term budget policy statement, Treasury forecasted a narrowing of the budget deficit from 3.7% of GDP in FY2015/16 to 2.5% by FY2019/20.

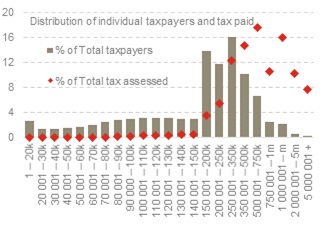

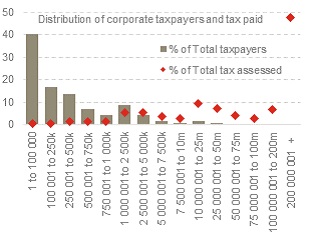

An analysis of the latest available South African Revenue Services (SARS) tax statistics for 2015 shows a narrow proportion of taxpayers servicing SA’s personal income tax bill. Around 12% of taxpayers were responsible for over 60% of the personal income tax take in 2015 (see chart 7).

Chart 6: Revenue share of GDP

Source: SARS, Treasury, Momentum Investments

Chart 7: Personal income tax take leans on higher-income earners

Source: SARS, Treasury, Momentum Investments

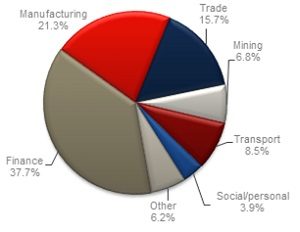

By the same token, the corporate tax take relies on a few large corporates in SA. Corporates ranking in the top 1% of taxable income contributed 68% of total corporate taxes collected in 2015 (see chart 8). On a sectoral split, financial services companies and manufacturers contributed the most to corporate taxes, at 38% and 21% respectively, while mining’s share came in under 10% (see chart 9).

Chart 8: Corporate tax take heavily skewed

Source: SARS, Treasury, Momentum Investments

Chart 9: Corporate tax contributors

Source: SARS, Treasury, Momentum Investments

Adherence to expenditure ceiling crucial in limiting rising debt profile

SA’s fiscal flexibility is limited in a subdued growth environment. Sticking to the expenditure ceiling will be an important positive signal to the rating agencies that government remains committed to its path of fiscal consolidation. Though government has already announced significant cuts to the goods and services component of government spending, we might see a further commitment to reduce wasteful expenditure. One of the largest drags on the fiscus is the civil servant wage bill. Although the escalation in the public wage bill to GDP from below 12% before the global financial crisis to around 15% more recently can be partly attributed to public sector hiring, the International Monetary Fund (IMF) has found that excessive real wage growth is the main culprit behind SA’s exorbitant public sector wage bill, which ranks as one of the highest in the world (as a share of GDP).

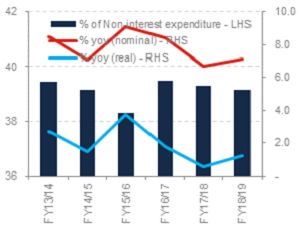

Public sector worker wages are currently consuming almost 40% of government’s non-interest expenditure bill (see chart 10). The current multi-year wage agreement extends to the end of June 2018, lowering the risk of a public sector strike this year. In August 2015 an agreement was reached after seven months of negotiations. The parties concluded a 7% wage increase for civil servants in year 1, increasing at CPI + 1% in the following two years, considerably lower than the unions’ opening demand of 15%. Treasury has alluded to an earlier and more inclusive discussion on wages this time around, which should lower the risk of public sector unrest next year.

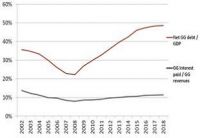

In addition, government’s interest bill is draining the fiscus. With nearly 12 cents of every rand of state revenue going towards debt-servicing costs (see chart 11), this line item remains the fastest-growing expenditure item between FY2016/17 and FY2019/20, increasing at an average rate of 11.0% y/y p.a. The rapid rise in debt-servicing costs is crowding out other (social and growth-enhancing) spending priorities and has been raised as a key concern by the rating agencies in the past.

Chart 10: Public sector wage bill

Source: Treasury, Momentum Investments

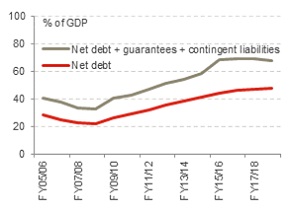

Chart 11: Government debt and interest (% of GDP)

Source: S&P, GG = gross government

Unaffordable demands and underperformance of many state-owned enterprises (SOEs) hazardous to overall debt metrics

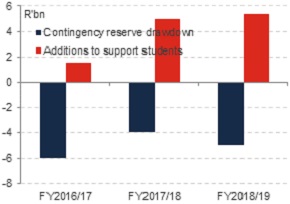

Moreover, unaffordable demands and the weak state of select state-owned enterprises (SOEs) in SA pose a threat to the country’s debt metrics (see chart 12). While we are not forecasting any additional funding to be announced for tertiary education in the upcoming February 2017 budget, the campaign for free education for all is likely to continue. Treasury reallocated a substantial chunk of the contingency reserve (an amount set aside, but not allocated in advance, to accommodate changes to the economic environment and to meet unforeseen spending pressures) to fund R17.6 billion in student fee increases for the 2017 academic year up to a maximum of 8% for students from households earning up to R600 000 per year (see chart 13). Treasury’s contingency reserves currently sit at R6 billion for FY2017/18, R10 billion for FY2018/19 and R20 billion for FY2019/20.

Chart 12: Overall debt levels flirting with 70%

Source: Treasury, Momentum Investments

Chart 13: Drawdown in contingency reserve funds

Source: National Treasury, Momentum Investments

In response to ailing SOEs, Treasury and the Presidency have constructed a reform plan on remuneration policies, governance controls and board appointments. However, progress has been incremental at best. Despite the 2016 Integrated Resource Plan confirming that nuclear power would not be required over the next two decades, Eskom was appointed as a nuclear procurer in December 2016, creating uncertainty over Treasury’s ability to curb the increase in contingent liabilities. In this regard, it has been reported that at least 27 companies have so far notified Eskom of their interest in participating in the first stage of the new nuclear build programme. While the State of the Nation Address (SONA) was quiet on the nuclear matter, uncertainty clouds the matter.

Structural reform needed to boost trend growth

In our opinion, fostering political and economic stability is key in retaining SA’s position as an investment grade country. Political-induced uncertainty around economic policies is likely to hinder government’s quest for higher growth and is likely to further tarnish SA’s credit worthiness.

Government has prioritised cost containment and curbing corruption through its Chief Procurement Office. It aims to achieve savings of up to R25 billion a year by FY2018/19. We are likely to see the upcoming budget re-emphasising these targets and repeating the savings made thus far on corrupt activities and wasteful expenditure.

Government has made significant strides towards ensuring labour stability. The upcoming budget is likely to reiterate the agreement on the national minimum wage, as well as advanced discussions around the code of good practice (involving collective bargaining, industrial action, picketing and the use of weapons during strikes).

Equally, government’s restated commitment to the Renewable Energy Independent Power Producers Programme will be seen a positive in generating higher levels of fixed investment and employment growth.

Treasury has responded to the #FeesMustFall campaign by freezing fees at 2015 levels for students whose parents earn less than R600 000 per year. A ministerial task team set up to tackle the free education debate estimates that SA will need between R42 billion and R45 billion a year to cover the full cost of tertiary study (tuition, accommodation, books and meals, plus one extra year) for up to 65% of the students currently enrolled at universities in SA. With government providing roughly R17 billion a year in the short term, the remaining is to be sourced from the private sector. It has been proposed that the Black Economic Empowerment Act be amended to have companies voluntarily contribute 1.5% of their payrolls towards funding poor students. This alone is estimated to raise around R8 billion in additional funding this fiscal year, increasing to R15 billion by 2020.

We expect little new information regarding the progress made towards gazetting the mining charter and passing the Mineral and Petroleum Resources Development Act (MPRDA) Bill. Moreover, the implementation of the Mining Company of SA Bill during the course of this year is likely to worsen the relationship between government and the mining sector. Without definitive legislation, SA is unlikely to be seen as an attractive destination for new (and foreign) investment in the mining sector.

The February 2017 national budget could touch on the controversial issue of land reform, by reiterating a point raised in the SONA that the Department of Human Settlements will draft a Property Practitioners Bill to accelerate efforts of increasing black land ownership. More equitable land ownership could compromise agricultural investment and food security if not approached correctly. Ceilings for private agricultural land ownership and regulating ownership of agricultural land by foreigners could hamper the agricultural sector’s development, in our view.

Given that the SONA failed to address SOE reforms, ratings agencies are likely to be watching the budget for any progress made on improving governance at these institutions.

Disruptive politics undermining reform and a low-growth environment top the rating agencies’ worry list

Since the last ratings review, global growth expectations have improved. Together with a near 20% recovery in commodity prices (since January 2016), SA’s export prospects are looking better. In addition, a likely improvement in domestic growth and the announcement of much-needed labour market reforms could allow SA to avert a ratings downgrade in June 2017. However, a downgrade in December 2017 cannot be ruled out. SA remains stuck in a low-growth environment marred by ongoing policy uncertainty. Little mention of strategies to reform SA’s ailing state-owned enterprises in the SONA is likely to be a concern to the rating agencies. A failure to accelerate SA’s trend growth prospects suggests, to us, a higher-than-even chance of a sovereign downgrade by at least one of the rating agencies by year end (see chart 14).

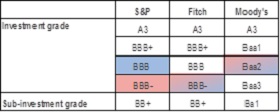

Chart 14: SA’s sovereign ratings

Source: S&P, Moody’s, Fitch, pink = foreign currency rating, blue = local currency rating