Delicate balancing act

Dr Adrian Saville, Chief Investment Strategist at Citadel

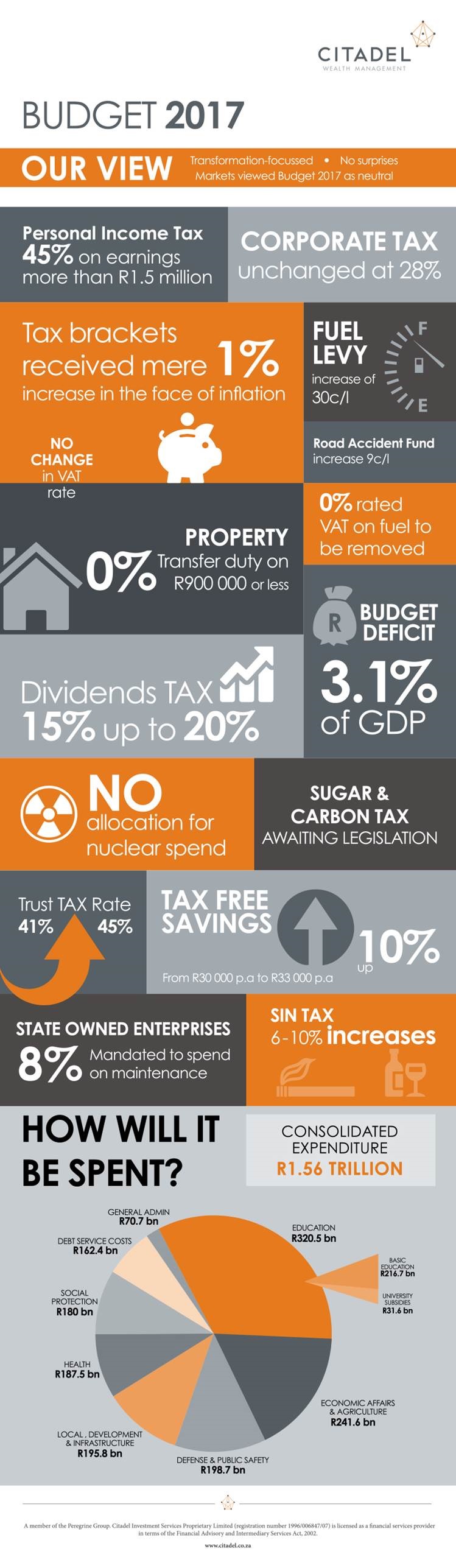

At a time of severe economic stress in South Africa, the Minister of Finance had few options available to deliver a budget which is “highly redistributive to poor and working families”. The outcome, therefore, contained few surprises and will help to promote transformation and redistribution.

“We knew upfront that the fiscus had a R28 billion hole to fill,” said Dr Adrian Saville, Chief Investment Strategist at Citadel, “and it will largely come from the individual tax payer.” Personal income tax is set to deliver R482.1 billion to the fiscus in the 2017/2018 tax year while VAT’s contribution will be R312.8 billion and corporate income tax will bring in R218.7 billion. This is a far cry from the 30:30:30 ratio that Treasury targeted from these three revenue sources in the early 2000s.

All the usual hidden taxes are rising – from sin taxes to carbon tax, the fuel levy and the soon-to-be-introduced sugar tax – but perhaps crucially, an additional R16.5 billion will be funded through bracket creep – the higher rate of tax that is paid as one’s income rises. With an inflation rate nearing 7%, the tax brackets have been hiked by a mere 1% across the board. In addition, a new top bracket has been introduced for income over R1.5 million at a tax rate of 45%. With the top marginal rate for individuals rising, the 45% rate will apply to trusts (excluding special trusts) as well.

The other notable source of higher revenue is a rise in the dividend withholding tax from 15% to 20%. “This one-third hike in the rate will bring in an additional R6.8 billion, but it is capital unfriendly”, notes Saville.

A clear focus has also been placed on tax avoidance and both individuals and corporates will need to ensure that they stay on the right side of the law. “The Minister made several allusions to curbing tax avoidance by both individuals and multi-national companies in both local and foreign jurisdictions. Especially in the context of increasing global tax transparency and the local Special Voluntary Disclosure Programme, tax payers need to ensure that they are fully compliant,” comments Hilary Dudley, MD of Citadel Fiduciary.

“On the expenditure side, there are two ballooning items that are cause for concern: debt service costs and the government wage bill,” notes George Herman, Head of South African Portfolios at Citadel. “Servicing debt now accounts for 12% of total expenditure – and this is at a time of low interest rates. At 10.5% p.a. it is the fastest growing line item. Clearly this is unsustainable.”

What was omitted from the budget speaks volumes as well:

- There was no increase in the VAT rate of 14% – a move which would have been extremely unpopular as well as having a greater negative impact on the poor.

- No large scale infrastructure spend was mentioned. “Capital expenditure is vital to stimulate economic growth,” explains Vanessa Hofmeyr, Portfolio Manager and Head of Equities at Citadel, “yet this was sadly absent from the budget speech. Given the tax hikes announced, the consumer economy will be dampened, with no corresponding uplift from fixed investment spending.”

- The corporate tax rate was maintained at 28%. “It is already at the upper end of global corporate tax rates, so there is little room for manoeuvre here,” explains Dudley.

There are several positives that we can take out of this budget:

- Compared to a year ago, there is greater stability in the fiscus, which is most encouraging;

- We have seen a healthy improvement in the performance of some of the state owned enterprises – the Development Bank of SA, the Industrial Development Corp and Transnet come to mind. Although others are lagging, there is certainly progress;

- The state is able to provide a moderately improving social welfare net – all social assistance grants, while modest, have been given inflation-related increases.

Applying strict fiscal discipline, Pravin Gordhan has managed the impossible – to shrink the budget deficit slightly from the 3.4% of GDP for the current tax year to an estimated 3.1% for the coming year, with debt being maintained below the 48% threshold. “However, the budget deficit isn’t 3.1%,” says Saville. “It’s a yawning gap between revenue collection and service delivery. We need to address the structural imbalances in the economy in order to reach the 3% growth we need to stave off a credit rating downgrade.”