What is the impact of negative rates on companies?

While economic theory has little room for the idea of negative interest rates, nine central banks currently have a negative interest rate policy (NIRP).

Which central banks are applying negative rates?

Historically, Switzerland and Sweden had already crossed the Rubicon by temporarily applying a NIRP: in the 1970s for the former, in 2009 for the latter.

Currently, the countries with a NIRP account for a quarter of global GDP. The Danish Central Bank (DNB) was the first to introduce it on a lasting basis in 2012. This was followed by the ECB in 2014, Switzerland (SNB), Sweden (SR) and Norway (NB) in 2015 and then finally Japan (BoJ), Hungary (MNB), Bulgaria and Bosnia Herzegovina in 2016.

The application of the NIRP however varies according to the rate targeted and the reason why this policy was put in place. In the case of the ECB, the BoJ and Denmark’s DNB, the deposit rate was targeted, while Sweden’s SR, in addition to the deposit rate, also put its key lending rate in negative territory. While a number of central banks adopted a NIRP in response to weak domestic demand and a lower inflation level than their target (ECB, BoJ, SR), others wished to limit the effects of the excesses associated with nonconventional monetary policies to limit the appreciation of their currencies that serve as safe haven currencies (Denmark’s DNB and Sweden’s SNB).

What are the transmission mechanisms?

In theory, the introduction of NIRP triggers an increase in household consumption and private investment, and improves companies’ price competitiveness. The first effect is explained by two transmission channels: the interest rate and the asset portfolio.

The introduction of a NIRP indirectly affects credit. Growth in lending picks up through the fall in the interbank rate, which then triggers a decline in all rates and more favourable financing conditions in the bond markets. The second effect (assets portfolio) is due to the ECB’s asset purchase programme or those of the other central banks with a QE policy.

The massive purchase of sovereign bonds lowers long-term rates and flattens the whole yield curve. With yields not sufficiently attractive for investors, they are switching to other assets, notably equities and real estate. The resulting wealth effect and the increase in lending has therefore had a positive impact on demand and investment. The gain in companies’ price competitiveness is due to the exchange rates transmission mechanism.

Faced with a particular country introducing NIRP, and thereby discouraged from investing in that country’s currency, investors will seek superior returns elsewhere. The currency of the country in question loses its appeal, weighing on the exchange rate, which depreciates, and thereby improves companies’ price competitiveness.

Have these effects really been seen?

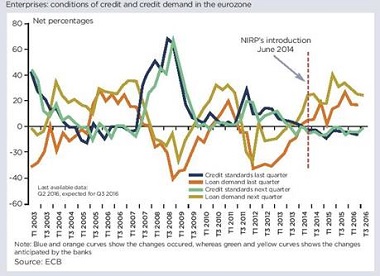

According to the Bank Lending Survey (BLS) of July 2016 conducted by the ECB, lending conditions for companies have again improved and demand for credit continued to rise in the second quarter of 2016 (see chart). Growth in lending to companies has thus picked up sharply since the introduction of the ECB’s NIRP, from a contraction of 2.6% y-o-y at the end of May 2014 to an expansion of 1.3% at the end of July 2016.

The ECB estimates that the NIRP has contributed approximately one percentage point to growth in lending to companies since July 2014 (Rostagno1). In addition, the survey on the access to finance for enterprises (SAFE) conducted by the ECB in June 2016 shows that the availability of external financing sources for PMEs is improving again and that banks are more prepared to grant them credit. The improvement in the macroeconomic environment in the Eurozone and the introduction of the NIRP had a positive impact on several components of GDP.

Growth in household consumption rose from 1.3% in the second quarter of 2014 to 2.1% in the first quarter of 2016, while growth in private investment increased from 1.7% to 3.8% in the same period. The impact on the euro/dollar exchange rate was also significant, with a depreciation of 18% from June 2014 to August 2016. The depreciation of the euro seems however to be of greater benefit to southern countries (Spain, Italy and Portugal), which have a lower range level than northern countries (Germany and the Netherlands).

Are banks heading for a fall in profitability?

A negative effect could however emerge if the negative interest rate environment continues for a long time, to the extent that lending to companies and households depends on the profitability of lending transactions, which is falling.

The introduction of the NIRP has flattened the interest rate curve. It is this phenomenon that reduces a bank’s net interest margin2 and which in turn leads to a fall in profitability. The loss in investor confidence and in banks’ willingness to grant loans could trigger a slowdown in lending growth.

The Bank Lending Survey (BLS) shows in fact that 80% of banks questioned believe that the NIRP has contributed to the fall in their net interest income3. For example, Commerzbank has quantified the cost of the NIRP on its income from bank loans at EUR161 million. The IMF estimates that even if the NIRP has up to now only had a weak impact on banks’ net interest margin (a drop of 50 basis points in the interest rate would lead to a fall of seven basis points in the net interest margin), the threshold from which the NIRP becomes counter-productive is approaching.

The ECB and other central banks have adopted a number of measures to limit the negative impact of the NIRP on banks’ profitability: namely, the increase in QE and the introduction of the TLTRO 2 by the ECB in March 2016; the introduction of a system that sets several levels of deposit rate (thereby only taxing surplus deposits) for the BoJ, Denmark’s DNB and Switzerland’s SNB. In addition, the BoJ is committed to continuing its government bond purchase programme in order to maintain the 10-year sovereign rate at 0%.

Commercial banks have been able to offset the negative impact of the NIRP up to now by increasing lending volumes, although they are still limited by regulation, the fall in interest expenditure and risk provisions, and capital gains.

Will the NIRP have other negative effects?

The weakness in interest rates has above all redistributed the resources of net savers to net borrowers. As net borrowers have a marginally superior propensity to consume than net savers, this supports consumption in the economy. However, this effect could conversely prompt certain savers to increase their savings to offset the loss in remuneration from their capital, thereby reducing their consumption. Finally, the NIRP could ultimately have an impact on financial stability.

Banks could in fact wish to increase their exposure to risk by lowering the quality of requirements for a loan or by increasing lending to SMEs (as the SAFE survey suggests) in order to generate more revenue. Historically, SMEs have recorded higher default rates than medium-sized and large companies. In addition, the risk relating to the emergence of “zombie” companies, whose activity can only be maintained through loans at artificially low rates, must also be monitored4.