The True Cost of Financing a Car Purchase – Opportunity Cost

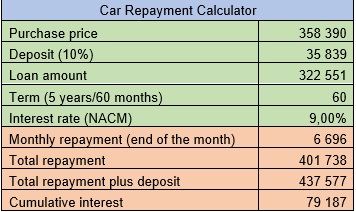

In a recent article in TopAuto, “How much you need to earn to drive an “average” new car in South Africa”, it was stated that the average price of a new car financed through Wesbank in January 2021 was R358 390.

An important key to financial success is to manage your lifestyle costs and to build an investment portfolio from a young age. If you make good, prudent decisions about the use of debt and how you finance the big-ticket items such as your home and the car you drive, it will make it much easier to save more and to build true wealth.

Consider the following example which is based on purchasing a so-called “average” car:

Given the monthly repayment of R6 696 (excluding any costs), the full repayment of the loan amounts to a total of R401 738 over the five-year period. Add the deposit of R35 839 and the car will cost you R437 577. You end up paying R79 187 in interest over the term, which represents about 22% of the car’s initial purchase price.

This brings us to a very important financial concept, namely: “Opportunity Cost”. According to Investopedia.com, opportunity cost is the cost of an alternative that must be forgone in order to pursue a certain action. Put another way, the benefits you could have received by taking an alternative action.

So, what is the opportunity cost of financing, please note financing and not buying, this car?

If you take the total interest paid of R79 187 and spread it over the term of repayment, i.e. 60 equal payments made at the end of each month and then leave the investment to grow, assuming an investment return of 9% per annum:

You would have about R155 000 after 10 years, R382 000 after 20 years and R2 295 000 after 40 years. That is R2 295 000 which you will not have, which is the opportunity cost of financing this car, the true cost of the debt.

And here’s the daunting thing – we are only talking about the cost of financing, i.e. the interest paid, without the fees. And only the cost of financing one car, a depreciating asset, over your lifetime.

Although we all need a car, we get to choose the car we drive and how we finance the purchase of that car. Over the long run it is prudent to find a balance between the amount of money you spend on financing costs and the amount of money you invest – ideally the scales should be tilted in favour of the latter.