The IMF is putting pressure on Europeans to grant Athens substantial debt relief

On April 12, 2016, Greece and teams from its EU and IMF lenders adjourned talks on a major bailout review¹, due to disagreements between:

• the IMF and European lenders over fiscal projections and the need for a major debt restructuring,

• Athens and its lenders over the magnitude of sacrifices imposed to the Greeks.

The lenders should return to Athens after this week’s IMF spring meetings in Washington (April 15-17). On this occasion, they are expected to discuss Greek reforms and debt with the possibly of reaching a preliminary agreement prior to the April 22 Eurogroup meeting.

The review has already been adjourned twice since January 2016 due to the rift among the lenders over the estimated size of Greece’s fiscal gap by 2018 and disagreements with Athens on pension reforms and the management of non-performing loans, which represent more than 50% of total Greek bank loans.

Due to “reform fatigue”, the IMF forecasts a primary deficit (i.e. excluding interest payments) of 0.5% of GDP this year and surpluses of only 0.25% and 1.5% in 2018 whereas EU institutions believe Athens can reach a primary surplus of 3.5% by 2018.

The IMF reiterated that, despite generous concessional official financing, debt dynamics where projected to remain highly unsustainable and that a decisive action by its European partners, in the form of a debt restructuring, was needed. However, the German finance minister has told the press that he saw no need for such an action. At the same time, Germany would like the IMF to participate in Greece’s third bailout programme, which is not yet the case.

The Greek government would like to restructure its debt but it also accuses the IMF of overstating the situation in order to extract concessions from it (the Greek government interpreted the leak, at the beginning of this month, from the site Wikileaks, related to a March 19 conference call of senior IMF officials, as an IMF effort to blackmail the Greek government with a possible “credit event” to force it to give in on pension cuts²). Compared to the Fund, the European Commission seems to have a more lenient approach concerning the pace of reforms and the government capacity to carry them out.

Risks

1. Political situation is still precarious. The leftist government promised to mitigate the impact of austerity and has a fragile parliamentary majority. It can hardly run the risk of a social upheaval at a time when it is already struggling with the migrant crisis. However, further measures will probably be required to achieve budgetary goals

including reforms related to the pension system, income tax, value added tax and the public sector wage bill.

2. A payment incident cannot be ruled out if no deal is reached. Greece must repay €3.5 bn next July to the IMF and the ECB. It will not receive any more assistance until the bailout review is concluded (otherwise, this would unlock a fresh tranche of the European loan of about €5 bn). Athens wants to avoid ending up in the same situation as in July 2015 when, being short of cash, it was forced to sign a new Memorandum of Understanding.

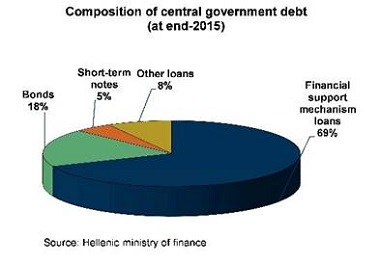

3. Without a substantial renegotiation of the public debt, it will be very difficult to pursue a less restrictive fiscal policy in the few coming years. The IMF already said in July last year that Greece’s public debt has become unsustainable due to the easing of policies during the previous year and the deterioration in domestic macroeconomic and financial environment. Public debt (estimated to be close to 180% of GDP at the end of 2015) was expected to peak at close to 200% of GDP in the next two years.

It is difficult to say, at this stage, if negotiations on reforms and debt relief could be interlinked from now on or if the bailout review will have to be concluded before considering any debt relief.