Sub-Saharan Africa: Sunny in the East, cloudy in the centre

Most of the sub-Saharan (1) economies have been enjoying economic growth since 2008, which has reached nearly 5% p.a. on average since that date, despite the storms such as Lehman Brothers collapse and the sovereign debt crisis in the Eurozone.

The reasons for this are numerous structural readjustments linked to a relatively low initial per capita wage level; high foreign investments in a context of abundant world liquidity; more stable political environments; as well as public finances in better order due to numerous debt cancellations. Also benefiting were the high prices of raw materials on which the region is dependent. Oil, metals, minerals and foodstuffs account for 80% of exports.

The sharp fall in global raw material prices over the last year means economic clouds are looming on the region’s horizon. Which countries are coming out best in this unfavourable environment? Are there other sources of growth to protect these countries from the coming headwinds?

To do this, it is important to distinguish between the countries which export non-renewable raw materials (oil, metals and minerals) from those that export renewables (food and agricultural products). the prices of the first having fallen more than those of the second during the past year.

The countries where the risk is highest have begun to diversify their exports and, more generally, their economy, allowing them to be sheltered from the adverse conditions.

Sub-Saharan African debt is expanding again

The cancellation of the debt of nearly thirty African countries, under the heavily indebted poor countries (HIPC) initiative, since 2000 and the acceleration in growth have made it possible to bring the overall burden of sub-Saharan African debt within reasonable limits.

The region's public debt/GDP ratio dropped from 66.7% in 2000 to 23.6% in 2008, its lowest point in three decades. This cancellation took the form of relief initially granted by the official creditors of the Paris Club (2) involving the cancellation of a flow of maturities over a certain period. To this which was added, at a second stage, after the HIPC completion point was reached, a reduction granted by the multilateral creditors (multilateral debt relief initiative or MDRI) and the cancellation of the debt stock still owed to the Paris Club creditors.

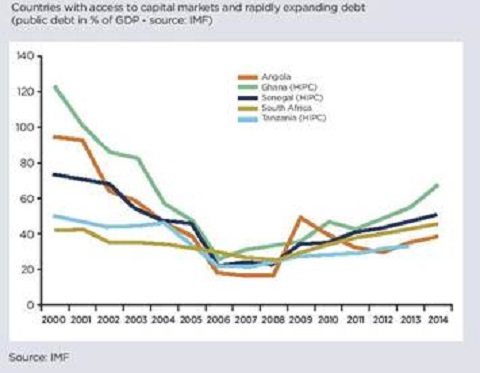

Since 2009, there has been a process of re-indebtedness, along with the reappearance of a budget deficit. Indeed, after five years of surpluses, the region’s public accounts recorded a deficit of nearly 3% of GDP on average over the 2009-2014 period. Turning away from concessionary loans from multilateral institutions, numerous African countries, including some of those which benefitted from the HIPC initiative, (3) successfully tapped the international financial markets from 2007 (Ghana and Gabon opened the way).

These eurobond issues were oversubscribed at interest rates generally lying between 6% and 7%. Moreover, certain countries took out significant bilateral loans outside the Paris Club countries, from countries such as China.

The borrowers benefit from greater freedom in their borrowing policy, in the context where their infrastructure needs require the mobilisation of a significant amount of capital. Facilitated by the monetary easing applied in western countries and abundant liquidity, this renewal of debt has proceeded at a fast pace in certain countries. The cost of these new debts is higher than that of the loans obtained from the multilateral institutions or the Paris Club countries.

This could again increase the region’s vulnerability. So, the recovery in the United States and Europe and the fall in oil prices are already beginning to lead to a tightening of borrowing conditions, noticeable for oil-producing countries, Ghana and Zambia. Some countries will therefore be forced to scale down their bond issuance programme, which could delay their investment programmes and will not make it easy to refinance their existing debts.

The depreciation of certain African currencies against the dollar (the currency in which eurobonds are denominated) is further complicating the task of the governments of the countries concerned, since it increases the value in local currency of repayments in foreign currencies.

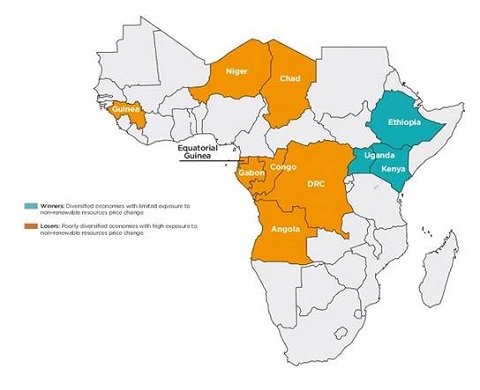

Several countries are very exposed to the fall in the price of oil, which is their main export. This has hardly encouraged them to undertake reforms with a view to diversifying their economy. Angola, Gabon and the Congo, for example, are among them.

Not all the countries which are net exporters of non-renewable raw materials are among them. Rwanda and, to a lesser degree, Nigeria are benefitting from the current process of economic diversification, which is lessening the effects of their worsening trade terms.

Other economies are, however, not very vulnerable to these recent fluctuations in raw materials prices, but are poorly diversified. Among them are Togo, the Central African Republic and Malawi. These are economies with low per capita income.

Finally, three countries are emerging as the big winners because they meet all these criteria: Kenya, Ethiopia and Uganda. They therefore have all the advantages necessary for achieving long-term growth without being penalised in the short term by the fall in raw materials prices.

The recent figures confirm this: GDP growth there reached nearly 7% on average in 2014. However, these favourable prospects with regard to short-term growth do not mean the total absence of risk and vulnerability. The recent terrorist attacks in Kenya demonstrate, for example, risks to political stability in the region.

The lack of infrastructure is also a well-known vulnerability as are high current account deficits (more than 7% on average expected in 2015). In the region as a whole, the level of public debt is moderate (33% of GDP on average) but is on a rising trend. Despite all these risks, perspectives for growth are particularly favourable in both the short and medium term in these three countries.