Greek election: More legitimacy but a difficult road ahead

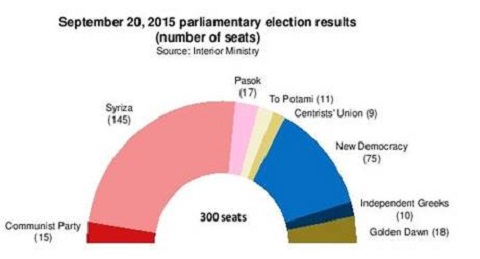

The left-wing Syriza party won the 20 September 2015 parliamentary elections with 35.5% of the votes and took 145 seats out of a total of 300 due to a majority bonus (50 extra seats for coming first).

This almost reiterated the January 2015 results and Syriza now holds a majority of 155 seats with the backing of the nationalist Independent Greeks, thus renewing its previous ruling coalition.

New Democracy, which was neck and neck with Syriza in opinion polls, took 28.1% of the votes. The Far-right Golden Dawn remained the third political force in parliament. The new coalition government was sworn in on 23 September 2015.

The snap elections were called after prime minister Alexis Tsipras lost his majority in August following the defection of some of his MPs who had opposed the new bailout conditions. The country has gone through five elections in six years.

The outcome of the ballot has been welcomed by European institutions and the bond market because of the strengthening of the legitimacy of the coalition and of the stability of Syriza.

In the near term, the re-elected prime minister Alexi Tsipras should have sufficient leeway to implement the bailout programme that he agreed to this summer. He can expect to experience stronger loyalty from his party as many hardliners of Syriza have left and formed a breakaway faction that has failed to enter parliament. If things go wrong, he would likely receive the support of a substantial part of the parliamentary opposition.

Risks

In the longer term, friction could re-emerge in the party and relations with the country’s creditors could become strained again. Mr. Tsipras, who was forced to accept tough conditions for Greece's third bailout, will probably continue to fight to obtain better terms on certain issues. The first review of the €86bn bailout package is due this month.

To be successfully completed, the new government must vote for further cuts in pension spending and tax hikes, reduce some salaries, adopt budgetary reforms, privatise big ports, the railway company and the electricity network operator, and liberalise product markets. The implementation of reforms could prove difficult and lengthy although they have been passed by parliament. The government, which already faces a long “to do” list, will also have to deal with the problem of migrants.

Disillusionment among the population remains high September elections were marked by a low turnout: 56% and farmers and unemployed are already planning to organise protests.

Bank deposits shrunk markedly before the imposition of capital controls at the end of June 2015 (-26% between then and September 2014). Non-performing exposures have surged to a record high (more than 40% of banks’ loan portfolios). The new government will have to recapitalise banks and set a timetable for lifting remaining capital controls. These were softened in July for businesses and in August for individuals.

The debt issue has not yet been addressed. Due to the current context of negative inflation and economic slump (Coface is forecasting a GDP contraction of 1.6% this year), the country will not be in a position to reduce its public debt ratio despite fiscal consolidation efforts.

As announced by the IMF, debt sustainability can only be restored due to a significant debt relief, well beyond what has been considered so far by the Eurozone. The IMF is ready to reschedule the debt but some European governments are opposed to writing off part of it.