France’s presidential election: The closer we get, the less we see

On May 7th 2017, French voters will elect a new President to succeed Francois Hollande. Less than two weeks before the first round, according to the latest polls, there is still uncertainty.

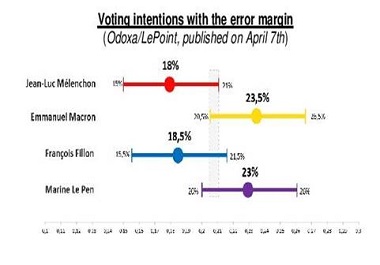

For the first round of the elections, the main candidates were given the following voting intentions on April 12th (OpinionWay/Les Echos/Radio Classique): M.Le Pen (far right, 24%), E.Macron (centrist, 23%), F.Fillon (conservative, 20%), J.-L.Mélenchon (far left, 18%), B.Hamon (socialist, 7%). As the gap between the four leading candidates has narrowed over recent weeks, uncertainty has increased.

Macron and Mélenchon: Two sides of the same coin

Macron and Mélenchon are the two candidates among the four favourites with the highest share of undecided voters (60% for Macron and 47% for Mélenchon). This shows that the two candidates are taking advantage of increasing voter mobility.

Both candidates are benefiting from the implosion of the socialist party, already perceived during President Hollande’s term and highlighted again by the difficulties that Hamon encountered when it came to gathering his own side following the primary elections.

The rapid increase in Mélenchon voting intentions (+ 6pp since March 23th), as well as the constant fall in voting intentions for the socialist candidate, are both evidence of a bandwagon effect within the left-wing. If Mélenchon struggled to translate his high voting intentions (17%) into votes in 2012 (given that he was affected by a strategic vote towards President Hollande), he is currently benefiting from this.

Le Pen and Fillon: Abstention the best ally?

These two right-wing candidates have the most stable electorate, considering the share of their voters that are certain about their votes (80% for Le Pen and 74% for Fillon). Nevertheless, in recent weeks they have had difficulty attracting voters beyond this.

Given the determination of their voters, compared to the more fragile electoral base of their rivals, Fillon and Le Pen would benefit the most from a high rate of abstention.

As uncertainty is continuing to grow, there are several scenarios. With the recent rise of Mélenchon in the voting intentions and the uncertainty resulting from the error margin of the polls1, a second round comprising Le Pen and the far-left candidate is now more likely.

This ex-ante-unexpected scenario increases the likelihood of victory for one of these

two candidates, negating the safety-net effect of the second round. In the worst case, the newly elected far-right or far-left candidate would be given a majority to rule the country during the parliamentary elections, which will be held on 11th June and 18th June (also following a two-round system).

In the context of growing uncertainty, recent voting events - such as the Brexit referendum, the US elections and the Italian referendum - highlighted a constant underestimation of non-mainstream positions. The gap between the last poll and the outcome of the vote was equal to 4.2% on average for “non-mainstream positions” in these three votes.

When comparing the political risk in France with Brexit, it would appear that this risk is still of a lower probability, given the amount of ballots, but of a much higher risk, due to its potential monetary consequences.

Unlike Fillon and Macron, the far-right (Le Pen) and far-left (Mélenchon) candidates intend to implement a complete restructuring of institutional and economic frameworks. In addition to protectionist measures, both candidates intend to increase public spending significantly, which they would finance through public debt monetisation as well as by massive tax reforms, as in Mélenchon’s plan.

If both candidates manage to find political support at the national level and subsequently fail to renegotiate European treaties with other member States, the Eurosceptic views they share and the agenda they have suggested would mean that France leaves the euro area. Given the framework shifts that these two candidates intend to implement, their elections could be sufficient to trigger an economic fallout.

The financial markets would price the default premium at a high rate due to the resulting political and redenomination risks2, in addition to the possibility of massive withdrawals of bank deposits leading to capital controls, as occurred in Greece in 2015. As a matter of fact, the 10-year bond spread with Germany increased to 70bp after a poll forecasting Mélenchon was in third position was published3.

1. The error margin for the survey realized by Opinion Way is for instance between 1,4 and 3,1 pp.

2. The redenomination risk is the risk a euro asset (such as public and private debt) is redenominated into a devalued legal currency, according to the law (national or international) under which the contract has been concluded.

3. Survey realized by Kantar Sofres-OnePoint and published on April 9th.