Devaluating the Egyptian Pound: Challenges remain

The strong US dollar is not only affecting the South African rand, but numerous emerging and established economy currencies.

Egypt’s central bank devaluated its currency by 14% on March 14th aiming at alleviating a dollar shortage that is increasing the gap between the pound and USD on the official and black markets.

The central bank surprised markets by holding an exceptional auction where it sold $198 million (USD) at a rate of 8.85 Egyptian pounds to the USD compared to 7.73 previously. In a statement published on its web site, the bank said it has decided to adopt “a more flexible exchange rate regime to reflect better the underlying forces of supply and demand and lead to greater foreign exchange liquidity by attracting greater investments”.

On the other hand, on March 17th the bank raised its overnight deposit rate to 10.75% from 9.25% and its overnight lending rate to 11.75% from 10.25% in a move to maintain the price stability.

Dollar shortage: The Egyptian pound was mostly pegged to the dollar until January 2003, when the exchange rate was floated. However, the 2011 political turmoil put pressure on the currency with plunging tourism revenues and fleeing foreign investors. To address this, the central bank started to provide dollars by formal auctions where it set the exchange rate.

The lack of dollars in the banking system and the widening gap between the official and black markets has pushed the monetary authority to switch into more flexible foreign exchange policies. The week prior to the bank’s exceptional auction, the black market exchange rate reached nearly 10 pounds to a dollar (almost 30% higher than the official rate), before falling at the weekend to around 91. The dollar shortage fuels the black market and weakens the business environment.

Low foreign reserves: Egypt’s foreign reserves were as high as at $35 billion USD in the period before 2011. Following the uprising, reserves plunged. As of February 2016, the country’s foreign reserves were at $16.5 billion USD, equivalent of barely three months of imports. Drying foreign reserves makes liquidity management difficult for the central bank through a controlled forex regime.

Before devaluating the currency, Egyptian authorities had introduced other measures to deal with the dollar shortage including capping dollar deposits in banks to $50 000 USD a month to sap the black market. But this exacerbated the situation by limiting companies’ ability to buy dollars on the black market and place it in banks for letters of credit for imports.

Risks

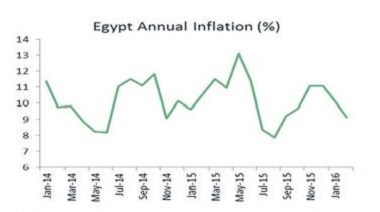

High inflation, import dependence: Having an import dependent economy, the devaluation would increase inflationary pressures. Annual urban consumer inflation reached 9.1% in February while monthly inflation rose by 0.97% driven by rising food prices.

Egypt remains the world’s largest wheat importer. Total food imports accounted for 21% of the country’s total merchandise imports in 2014, according to the World Bank. Hence, the pound’s depreciation may cause a further rise in inflation, in addition to the impact of the government decision of cutting fuel subsidies in 2014 by more than 70%.

Although the depreciation was largely welcomed by investors, it may not be enough to win back investor confidence. In fact, early in February, General Motors suspended its Egypt operations citing not having access to dollars to pay for imported parts. Air France-KLM also complained that it had been unable to repatriate earnings since October and was owed more than 100 million Egyptian pounds ($11.3 million USD)2.

The manufacturing sector’s need for a better business environment: Egypt’s economy relies primarily on revenues from tourism and the Suez Canal. The total contribution of travel and tourism to GDP is expected to be 12.7% in 20153 while annual income from the Canal Suez seen to increase to more than $13 billion USD by 20234.

Yet these revenues are easily affected by security issues and choppy global trade. Indeed, the Suez Canal revenue decreased 4% on a monthly basis in January 2016 to $412 million USD. In this sense, the devaluation of the pound could strengthen Egypt’s competitiveness yet other challenges such as corruption, the informal economy and difficulties for SMEs to access to credit continue to weaken the country’s manufacturing sector.

Coface country risk assessment for Egypt: B and GDP forecast 2016: 3.8%

1 “Egypt devalues pound, signals move toward floating currency”, March 14,

2016, Reuters.

2 “Egypt says reaches agreement over foreign airline payments”, March 3,

2016, Reuters Africa.

3 “Egypt: a slow and fragile recovery”, Oct. 2015, Coface.

4 “Egypt's Suez Canal revenue rises to $462.1 million, Oct. 2015, Al Arabiya.