Despite Challenging Economic Conditions, Serious Consumer Credit Delinquency Rates in South Africa Generally Declining

TransUnion South Africa introduces inaugural Industry Insights Report containing latest consumer credit trends

• Newly released figures show slow or declining new account originations, as both consumers and lenders exercise caution in response to economic headwinds

• Declining delinquency rates across most major consumer lending categories suggest that, despite the economic environment, consumers have been steady in managing their financial obligations

Despite difficult economic conditions throughout 2018, serious delinquency rates for nearly all major South African consumer credit products declined in the third quarter of 2018 on an annual basis. The findings were revealed today in TransUnion’s (NYSE: TRU) inaugural Industry Insights Report, the first in an ongoing series of quarterly reports that summarise data and trends in the South African consumer credit market. The report draws on TransUnion’s unique dataset of over 23 million South African consumer credit records.

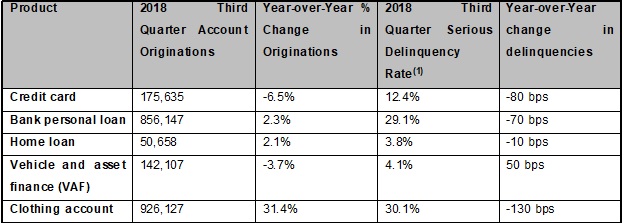

TransUnion’s new report found that home loans, the credit product with the highest total balances outstanding, also had the lowest serious balance-level delinquency rate in the most recent quarter. As of Q3 2018, home loans comprised 1.84 million accounts and R888 billion in total balances. The balance-level serious delinquency rate—measured as 3 or more payments past due—saw a 10-basis point decline in the last year to close the quarter at 3.8%. While almost all other credit products also experienced yearly declines in serious delinquency rates, TransUnion noted that vehicle and asset finance (VAF) loans – the credit product with the second highest total balances – experienced a 50-basis point year-over-year rise to 4.1% in Q3 2018. Approximately 2.5 million VAF accounts were open with total balances of R414 billion.

“Tough economic conditions continue to prevail in South Africa, as consumers’ wallets have been challenged by continued high unemployment rates, weak wage gains, significant fuel price hikes, and the ongoing rand weakness. In light of these conditions, it would be reasonable to expect a deterioration in consumer credit performance over the past year. However, we have seen largely the opposite, with serious delinquency rates improving for most credit products since Q3 2017. This is certainly welcome news for the South African credit market and the recently announced improvement in GDP for Q3 2018 is indeed an encouraging development that could result in more positive consumer credit trends in future quarters.” said Carmen Williams, director of research and consulting for TransUnion South Africa.

“There are multiple potential drivers of this improved delinquency rate over the past year,” continued Williams. “Originations growth for most consumer credit products has been relatively slow in recent quarters, likely due to more cautious underwriting practices by lenders. We also suspect that consumers, in the face of a challenging economy, may be more focused on keeping their credit relationships in good standing, thereby maintaining their access to credit going forward. This trend was also echoed by the results of our recent Consumer Credit Index research, which indicated cautious consumer credit behaviour.”

Delinquencies Primarily Down, As Originations Are Dropping for Many Credit Products

(1) Balance-level serious delinquency rate, measured as percentage of balances 3 or more payments past due

While delinquency rates on consumer credit have fared relatively well through the 2018 recession, new account growth has been impacted to a greater extent. Most major credit products experienced low—less than 3%—or negative Year-over-Year (YoY) new account growth in the third quarter of 2018 compared the same quarter of 2017. Bank personal loans saw muted growth of 2.3%, while home loan originations grew 2.1%. Meanwhile, VAF originations dropped 3.7% and new credit card accounts fell 6.5%. The exception was clothing accounts, which saw a robust 31.4% growth in the third quarter.

“Clothing was the only product that showed substantial origination growth YoY in Q3 2018. Other account types remained essentially flat or negative as lenders’ appetite for risk appeared to wane,” continued Williams. “The consequent subdued levels of balance growth across consumer credit products is not surprising. While it is encouraging to see some growth in select products, it is clear that the recession has had an impact on growth dynamics in the market overall.”

Credit card market stabilises following period of considerable growth

The report examines major credit products in depth and found that, overall, the number of credit cards in circulation increased 1.5% YoY and stood at more than 6.6 million in the third quarter of 2018. Over the same period, outstanding balances increased by 3.2% and stood at R108 billion in Q3 2018. While positive, the card balance growth was considerably lower than the 8.7% YoY growth seen the prior year, in Q3 2017. That prior year, originations expansion was due in large part to new market entrants and increased card marketing. Card originations in Q3 2017 were 32.7% above the level seen in the prior year period. As origination efforts have plateaued and in fact begun to recede since then, the YoY decline in originations observed in the most recent quarter does not come as a surprise.

While account and balance growth has slowed in the 12-month period ended Q3 2018 compared to the prior year, it is important to note that the credit card market is continuing to expand, albeit at lower rates. This dynamic reflects that, particularly in difficult economic times, consumers continue to need and seek credit and to use the credit facilities they have available.

Moreover, consumers appear to be taking care of their credit card accounts in order to preserve continued access to their available credit. Balance-level credit card delinquencies (3+ months in arrears) fell by 80 bps from 13.2% in Q3 2017 to 12.4% in Q3 2018 – an indication that consumers are managing their available credit despite the recessionary environment.

“Access to credit is particularly important to consumers during difficult times. The ability to use credit to make ends meet is a source of stability for struggling families. It is encouraging to see that consumers have continued to gain access to credit cards over the past year, and have generally managed their accounts responsibly to maintain their access to these accounts. That is good news for families, and a positive sign for the recovery of the economy,” observed Williams.

Vehicle and asset finance (VAF) market pauses for breath as delinquencies rise

After significant expansion in the VAF market in recent years, growth appears to have slowed more recently. The report reveals that in Q3 2018, total VAF balances grew at a slower pace YoY—6.9%—compared the levels seen in the prior two years. It should be noted that this balance growth rate is still higher than those of most other South African consumer credit products.

This balance growth occurred as the total number of VAF accounts remained flat, increasing by a mere 0.1% YoY in Q3 2018. Meanwhile, origination growth declined in the third quarter by 3.7% compared to the prior year period, likely driven by tighter lending criteria. The tightening of lender underwriting may be a response to the significant rise in VAF delinquencies over the past year: the percentage of balances 3+ months in arrears increased by 50 basis points, to 4.1%, from Q3 2017 to Q3 2018. This follows a 70 basis point increase the prior year from Q3 2016 to Q3 2017.

A potential bright spot in the delinquency picture is in the most recent quarter’s data, as the Q3 2018 account-level serious delinquency rate (3+ months in arrears) dropped 16 basis points Quarter-over-Quarter (QoQ) from Q2 2018, to 4.7% (balance-level delinquencies dropped by 30 basis points from 4.4% to 4.1% over the same period). QoQ delinquency comparisons can frequently be misleading due to normal seasonality, which causes movements in the same quarters each year; for this reason YoY delinquency comparisons are generally more accurate indicators of trends. But in this case, the QoQ drop in Q3 2018 is the first sequential quarterly decline observed in the past 7 quarters. While it is difficult to draw conclusions from a single quarter’s data, this development bears watching in future quarters to determine if the recent rise in VAF delinquencies has stabilised.

“Though it is just a short-term trend at this time, it’s one we are closely observing as the decline did not follow recent seasonal patterns. This quarter’s performance certainly bodes well for this industry, especially if further improvements are observed in the final quarter of the year,” added Williams.

Signs of potential future improvements in vehicle purchase demand and related VAF originations comes by way of TransUnion’s recent Vehicle Pricing Index, which showed that price increases for both new and used vehicles have slowed over the past year and are increasing at below-inflation levels. This points to improved vehicle affordability and may bring more buyers into the market who will seek financing for their vehicles, a welcome development for VAF lenders.

An evolving consumer credit market causes a clear shift in lending strategies

“In light of the difficult economic environment, consumer credit growth is relatively subdued by recent standards. After a period of relatively robust growth in 2017, it has clearly cooled over the past year. Lenders are still making new credit available, but appear to have become more cautious in their originations strategies to ensure that loss rates remain manageable. Based on recent performance data, this strategy seems to be working. The challenge going forward will be for lenders to find ways to prudently grow and expand credit access to more consumers, and thereby help facilitate consumer spending and stimulate economic activity. Lending strategies are about finding the right balance between growth and risk, and lenders need to find that balance as they play a critical role in the economic expansion of South Africa,” concluded Williams.

About South Africa Industry Insights Report

TransUnion’s South Africa Industry Insights Report is an in-depth, full population-based solution that provides statistical information every quarter from TransUnion’s national consumer credit database, aggregated across virtually every active credit file on record. Each file contains hundreds of credit variables that illustrate consumer credit usage and performance. By leveraging the Industry Insights Report, institutions across a variety of industries can analyse market dynamics over an entire business cycle, helping to understand consumer behaviour over time. Businesses can access more details about and subscribe to the Industry Insights Report. The South Africa Industry Insights Report looks at major consumer lending categories: credit cards, personal loans, home loans, vehicle and asset finance (VAF), and clothing. The report primarily focuses on three dimensions across these categories: originations (new accounts opened), balances (outstanding total and average lending balances) and delinquencies (accounts in payment arears).