Credit Originations Continue to Rebound Amid Tough Economic Climate

• Delinquencies stabilise across major consumer credit products, except for credit cards due to the recent resurgent growth in new business

• Despite recovering new account volumes, outstanding balances continue to lag prior year levels

• Secured lending performance has stabilised, with signs of a slowdown in home buying activity

TransUnion today released the findings of its Q2 2022 South Africa Industry Insights Report. The latest analysis covers a period of rising inflationary pressure, a high interest rate environment, and additional macroeconomic factors exacerbated by conflicts abroad. The report found a number of notable trends within the South African consumer credit industry pertaining to new business volumes, delinquencies and the level of outstanding debt.

The findings are in the context of the second lowest consumer confidence (1) reading in three decades, second only to Q2 of 2020 at the peak of the initial outbreak of the pandemic. That reading signalled a corresponding marked slowdown in consumer spending in the same months, with a 2.5% year-over-year (YoY) decline in retail sales from a year earlier in June (2). Consumer sentiment was primarily impacted by the highest inflation rate in 13 years (3), as well as increased interest rates (4). This was reflected in the Q2 TransUnion South Africa Consumer Pulse Study published in July, with 60% of households surveyed indicating that they were focused on cutting back on discretionary spending.

Credit Card Growth Leading the Charge

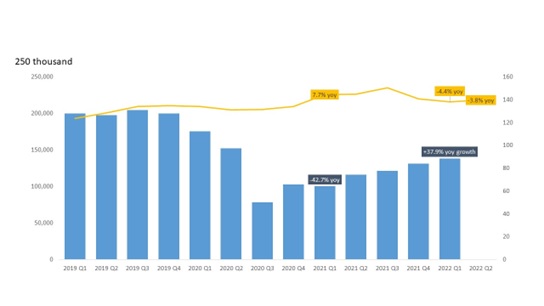

New credit activity grew despite overall consumer sentiment indicating a cutback on spend. Credit card origination volumes - the measure for new accounts opened - increased by 37.9% YoY in Q1 (the latest period for originations due to reporting lag), in stark contrast to the 42.7% YoY decrease in originations seen at the same point in 2021. The volume of credit card originations has been steadily growing since its low in Q3 2020, indicative of increased lender appetite for growth as well as higher consumer demand for credit.

However, despite the resurgence in card originations, current volumes remain below pre-pandemic levels (see chart 1). From an age perspective, 74% of all card originations came from Gen Z and Millennial consumers, indicating higher demand for credit from younger consumers and a willingness by lenders to extend credit to these borrowers. However, the growth in new cards is not yet reflected in outstanding balances, which have decreased by 3.8% YoY in Q2 2022.

The decrease in outstanding card balance levels can be attributed to several factors. Attrition from voluntary and involuntary account closures has resulted in the total number of active credit card accounts decreasing by 2.3% YoY as of Q2 2022. New business volumes also recorded six consecutive quarters of negative growth prior to the recovery that began in Q3 2021, bringing down outstanding balances. Furthermore, despite higher card origination volumes in Q1 2022, these new accounts carried lower average credit limits (down 5.2% YoY), limiting the capacity of consumers to spend and putting negative pressure on balances.

Chart 1: Card Originations (bar) and Outstanding Balances (line)

“The significant rebound in card originations compared to the depressed levels at the height of the pandemic reflects a returning appetite from lenders seeking growth from new business,” said Lee Naik, Chief Executive Officer of TransUnion Africa. “Our analysis tells us it is younger and generally higher-risk borrowers who are primarily driving new credit card growth. While expanded consumer access to credit is generally positive for the economy, lenders should closely monitor portfolio risk and leverage predictive tools to manage and predict pre-delinquency behaviours.”

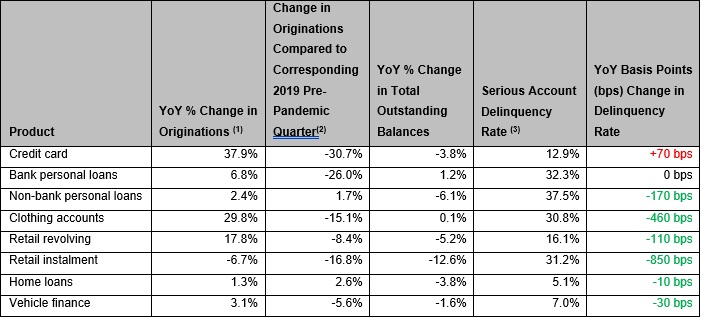

Clothing accounts and revolving retail credit saw YoY originations growth of 29.8% and 17.8% respectively in Q1 2022. While serious account delinquency, measured as a percentage of accounts three or more months in arrears, remains high - at 30.8% for clothing accounts and 16.1% for revolving retail credit - the delinquency rate on these types of accounts has improved by 460 basis points (bps) on clothing accounts and 110 bps on retail revolving credit YoY in Q2 2022.

Table 1: Q2 2022 Metrics for Major Consumer Credit Products

1 Originations for Q1 2022 compared to Q1 2022, originations are viewed one quarter in arrears to account for reporting lags

2 Originations for Q1 2022 compared to Q1 for 2019 (comparable pre-pandemic quarter)

3 Account-level serious delinquency rate, measured as a percentage of accounts three more months in arrears

The Q2 TransUnion South Africa Consumer Pulse Study found that for the second consecutive quarter, 56% of households said that they would be able to pay their current bills and loans. This positive ratio of consumers with sufficient debt service capacity could be due to a rise in household income levels in Q2 2022, as 31% of consumers surveyed indicated an increase to their household income, a 5% increase from Q1 2022.

In addition, South Africa’s unemployment rate for Q2 decreased by 60 bps to 33.9% (5). This drop in the unemployment rate may have kept consumers somewhat optimistic regarding future income prospects, with 70% expecting their household income to increase in the next 12 months. As at Q2 2022, 35% of consumers surveyed stated they had paid down their debt faster over the past three months. This figure was more pronounced for younger consumers, with 39% of Gen Z and Millennials sharing these sentiments.

In addition, one in three consumers intend to use money from their savings to service their bills and debt obligations, a sign that consumers are prioritising their credit obligations. This was observed at a time when credit data showed improvements in delinquency performance across most credit products.

“While reduced delinquency rates are good news for lenders, they are indicative of the current South African economic environment in which consumers are being more cautious towards debt than previously, as they navigate rising interest rates and an inflation environment that has contributed to a higher cost of living,” said Naik. “Lenders planning to increase origination activity could hone their acquisition strategies to focus on younger consumers, who are relatively new to the credit environment. Purposeful education initiatives can help create greater credit awareness and literacy to enable inclusion for younger consumers in the credit ecosystem.”

Decoding younger consumers’ needs and behaviours

A recent TransUnion study presented at the 2022 TransUnion Financial Services Summit, Understanding Gen Z: The Next Growth Engine, showcased the recent credit participation and usage trends of South African Gen Z consumers (born between 1995 and 2010, aged 22-26). It compared those trends against those of Millennials (born between 1980 and 1994) from five years ago, who were then in the same age range. The study compared product openings over a six-month period to assess credit participation differences between Gen Z and Millennials, and measured credit score migration for a 12-month window for both generations. It also analysed credit participation by age to identify differences in credit demand and preferences across the two generations.

The study found that South Africa’s 6.8 million credit-eligible (18 years and over) Gen Z consumers carry fewer credit products compared to their Millennial counterparts from five years ago, likely due to lower credit awareness and constraints in supply caused by recent pandemic impacts. Clothing accounts are by far the most popular credit product among these generations, at 93% within Gen Z and 84% within Millennials, followed by bank personal loans and non-bank personal loans for both cohorts.

Gen Z consumers significantly lag Millennials in personal loan participation (14% compared to 26%), which may be due to reduced lender risk appetite impacted by pandemic-induced economic stress. Gen Z consumers display a mixed credit performance compared to Millennials, performing worse (by around 500bps) on new credit cards, but outperforming their counterparts by around 200bps on bank personal loans, measured at six months on book post-account origination.

While just 13% of both groups held credit cards, survey findings suggest this is likely to grow. In all, 48% of Gen Z consumers in the Q2 TransUnion Consumer Pulse Study said they intend to apply for new credit; 40% of Gen Z consumers said they were planning to apply for a credit card; and 49% of Millennials plan to apply for a personal loan. At the same time, card issuers may be facing competitive challenges from more convenient and affordable offerings such as ‘buy now pay later’ (BNPL) providers, along with other digital payment solutions.

“During times of uncertainty, a better understanding of the credit needs and journeys of younger generations can help lenders meet demands and capture opportunities for prudent growth,” says Naik. “Rising inflationary pressures present an opportunity for lenders to educate younger consumers on the benefits of having additional liquidity, and of the importance of managing credit responsibly. This approach may help capture these consumers early in their credit journeys, creating more potential for lifetime value.”

1 According to The Bureau of Economic Research FNB/BER Consumer Confidence Index, 29 June 2022

2 According to Statistics South Africa

3 According to Statistics South Africa

4 According to Trading Economics, the South African Reserve Bank raised its benchmark repo rate to 4.75% on 19 May 2022.

5 According to Statistics South Africa

Click here for SA IIR Q2 2022 Executive Summary...