China’s future currency fluctuations unsure

Rocky Tung, Coface.

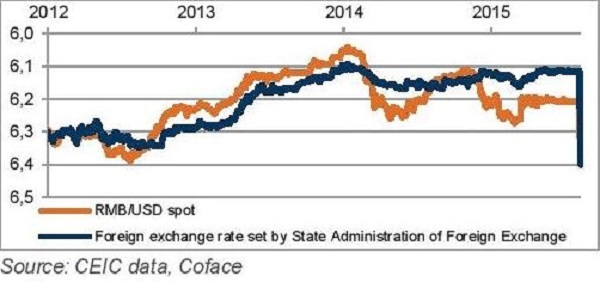

The People’s Bank of China (PBoC) surprised the market by lowering the benchmark exchange rate from 6.1162 to 6.2298 (approximately 1.9%) per dollar on Tuesday August 11.

The currency continued to depreciate in the following days, leading to an accumulated depreciation of 3% in three days. The move was the most significant one-day devaluation of the currency against the USD since the PBoC adopted exchange-rate reform on July 21, 2005

Growing concerns about the Chinese economy's health led to a slump in commodity prices (WTI down to 42,3 USD per barrel, the lowest level since march 2009) and global stocks. To reassure markets, PBoC then raised the value of yuan against US dollar by 0.05%.

The Chinese authorities said the motive for the adjustment was to step up the country’s effort to liberalise the foreign exchange market. In a report on August 3, IMF staff economists appeared to be sceptical that the central parity rate (the reference rate) is an appropriate exchange rate to be used as a reference in SDR calculations, due to the consistent discrepancy between the rates, which implies that the daily fixing does not directly reflect actual trade activities. Going forward, PBoC’s daily fixing rate should be more responsive to changes in market conditions. The reaction of the central bank was directly addressing such issues.

The yuan’s devaluation is also a timely intervention considering China’s current economic slowdown, indicated by recent economic data: exports declined 8.4% Y-o-Y in July –dragging year-to-date export down -0.6% as at the end of July – while the purchase price index (PPI) continued to decline for the 41st month, hitting its lowest since October 2009 of -5.4% Y-o-Y.

The slowdown is also in the context of the strengthening of the RMB in the last year. As at August 7, most of the other Asian currencies depreciated against the USD since the end of April, highlighted by Malaysia’s Ringgit (-9.3%), the Korean won (-7.5%), the Thai baht (-5.9%), the Singapore dollar (-4.3%) and Taiwanese dollar (-3,2%), while the renminbi (RMB) remained stable during the same period.

Risks

The currency devaluation has better positioned the renminbi (RMB) for an SDR-basket inclusion. In its response to media requests on August 11, the IMF said the new development is “a welcome step”, and that that it should allow market forces to have a greater role in determining the exchange rate.

While suggesting that there appeared to be no direct impact on the SDR-basket review, the IMF suggested that “a more market-determined exchange rate would facilitate SDR operations in case the RMB were included in the currency basket going forward”.

Coface expects that the devaluation will boost Chinese export only slightly but could induce new capital outflows. Indeed, exchange rate elasticity is relatively high: according to Thorbecke (2013). A 10% appreciation of the integrated real exchange rate, REER, would decrease exports by 10% or more.

However, the REER increased sharply in recent years (+36% between January 2010 and May 2015, and +14% Y-o-Y according to IMF) and should remain high despite the recent devaluation.

The risk of expanded capital outflows could be on the rise with the continued weakness of return on capital. In 2014, capital outflows were already large and this trend appears to be confirmed with the sale of a net $38.9 billion in foreign exchange in July by the PBoC and commercial banks.

The impact on other countries is uncertain. The devaluation is moderate and the risk of a currency war is not Coface’s base-scenario. Exporters to China such as Australia (27% of total exports to China) and Taiwan (26%), could be affected by the devaluation initially, but more so because of the slowdown of internal demand from China.