Argentina’s agreement with holdout creditors

The first step towards normalisation, but not the Panacea.

The February agreement between Argentina’s government and its holdout creditors in exchange for a payment of USD $4.6 billion to the the toughest funds (Elliot Management, Aurelius Capital and Bracebridge Capital) abandoning their lawsuits against this country.

The parties agreed to settle the details of the litigation in weeks. Admittedly this agreement is positive for restoring investor confidence in the medium-term, but does not mean higher growth prospects in the very short-term.

The agreement is subject to the approval of the local Congress that also needs to address the so called “Lock Law and Sovereign Payment Law”, that forbids the government from making payments to litigating funds.

In March, President Macri called Congress to support the holdout deal that will cover around 85% of the defaulted debt without providing any dates to debate the agreement in the Lower House and Senate. Government needs 135 votes to repeal the law but President’s coalition “Cambiemos” doesn’t have a majority.

However, a compromise will probably be reached before the end of March. Senators and regional governors are aware that their provinces could obtain cheaper financing if the agreement is sealed. According to the local press, the holdout deal will be submitted for vote in Senate on March 17th-18th.

The agreement will put an end to the 15-year legal saga between Argentina and “vulture funds”. In 2001, following a long period of economic and political instability, Argentina defaulted on its sovereign debt. Over the years Kirchner´s renegotiated the debt with a huge discount with 92% of the creditors.

A diverse group of “holdouts” opted instead for litigation in the hope of achieving a better settlement. Although Argentina succeeded in reducing much of its sovereign debt, its unorthodox methods did please the international credit markets and triggered legislative action and sanctions in the United States.

Since then, Argentina couldn’t tap into the international debt market. In June 2014, a U.S. judge gave a favourable ruling for bondholders, which did not include the structured debt (the holdout funds).

Government refused to comply with the judge´s sentence and defaulted for the second time. The US courts have blocked payments to other bondholders until an agreement with the holdouts is reached.

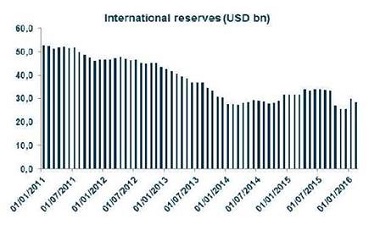

Argentina cannot rely on its international reserves to settle the payments and will probably seek to raise money in the international markets after the Congress decision.

Despite a small rebound in the level of international reserves at the begging of the 2016, Argentina’s reserves were estimated at only $28.3 billion dollars on February (the lowest level since 2006).

This could decrease further in the next few months if central bank is obliged to use this to support peso depreciation (the peso depreciated about 38% since the currency controls were lifted last December).

Argentina will probably tap on the international debt market as soon as possible to solve the litigation and to support local currency in case of stronger volatility. Holdout funds have already agreed not to intervene if Argentina decides to issue bonds in foreign markets.

Despite the optimism generated by the agreement, investors will probably maintain a wait-and-see approach in the coming weeks while expecting judiciary reform.

The economy is likely to benefit from the gradual normalisation of economic policies in the medium-term, but the transition will be painful because of internal policy adjustments. Private consumption is likely to suffer, depreciation of the peso (given the limited local production, numerous of products are imported) as well as the acceleration of inflation. Inflation will also be boosted by the elimination of massive public subsidies (electricity, transport and gas).

A revival of activity by government seems unlikely. Government is committed to bring down public spending to redress public accounts (the fiscal deficit achieved 7% of GDP in 2015). Last but not least, the automotive industry is still being affected by the slowing demand from Brazil, the leading trading partner.