Advanced economies: The recovery is underway, but remains fragile

Growth outlook remains strong for the US. After the brief downtick recorded during the first quarter resulting from number of temporary factors (fall in energy sector investment, harsh weather conditions, etc.), the economy rallied sharply from Q2 onwards (+0.9% q/q), driven by both household consumption and investments.

Consumer spending remains underpinned by the decline in the unemployment rate, household debt being lower than pre-crisis levels and cheap petrol prices. Investment also seems to be gaining momentum, as illustrated by the strong increase in durable goods orders in July and continued buoyancy in the property sector.

There are nonetheless two clouds on the horizon. The strong dollar is likely to continue weighing on exporting companies and the continued slide in the oil price this summer could have contrasting effects on the US economy by the end of the year.

This was the case at the beginning of the year, when gains in terms of household purchasing power due to lower petrol prices, were partially offset by lower investment in the energy sector.

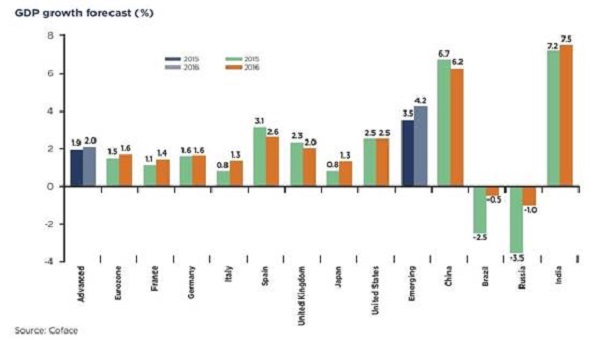

In the eurozone, successive quarters have recorded positive growth indicators: +0.3% q/q during the second quarter, after +0.4% between January and March. Multiple factors are supporting the Eurozone economy: lower unemployment (10.9% in July, down 0.7 point of percentage over one year), less rigorous budgetary policies and a low inflation rate, which is benefitting household consumption, combined with a highly expansionist monetary policy leading to a gradual increase in private sector credit (+1% annualised in July).

Economic growth rates lack consistency however. Although growth in Spain should exceed 3% this year, it will be more moderate in Germany (+1.6% expected in 2015 and 2016) and particularly France (+1.1% and +1.4% respectively) and in Italy (+0.8% and +1.3%).

Furthermore, the fall in the oil price is maintaining inflation at a low level and helping restore corporate margins. Paradoxically however, wider margins do not necessarily mean a sharp recovery in investment. Corporate investment hinges chiefly on business confidence, which has been tested to the full recently, starting with the Russian crisis during the summer of 2014, which weighed temporarily on investment (particularly in Germany), followed by the risk of Greece exiting the Eurozone this spring, while incertitude over Chinese growth is currently worrying company managers and delaying investment decisions.