Medical scheme healthcare utilisation during lockdown

With the COVID-19 crisis looming, many are concerned by the likelihood of overwhelmed and overcrowded hospitals. This is of course a valid concern. For now, as at the time of publishing, the number of hospitalised COVID-19 patients remains low.

There has been a proliferation of models which predict hospital admission rates when the COVID-19 infection rate accelerates. There has though been very little focus on what is happening our hospitals right now.

COVID-19 and the interventions aimed at mitigating its impact have already had a dramatic effect on hospital admission rates. These effects can change the way medical schemes approach the management of hospital admissions after the pandemic, the way that medical schemes plan to fund the cost of the pandemic and the way that medical schemes manage affordability constraints.

Many hospitals have temporary suspended elective admissions in order to minimise the risk of spreading COVID-19 and build spare capacity for COVID-19 patients. Patients too are wary of being hospitalised unless deemed absolutely necessary.

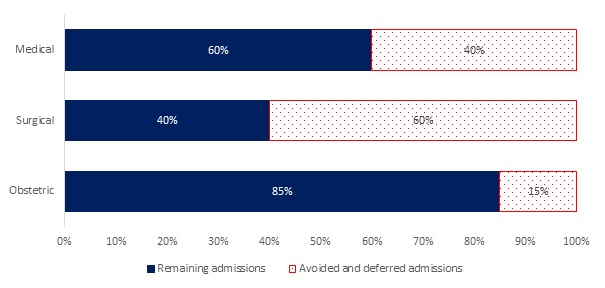

We have seen a dramatic reduction in hospital admission rates across medical schemes. The reduction in the hospital admission rate is in the order of 50% across admission types.

The admission rate for surgical cases has declined by more than 60%. Many types of surgery and theatre-based investigation are elective and can be delayed. For example, cataract procedures and diagnostic scopes are amongst the most common surgical procedures and both can often be deferred.

The admission rate for medical cases has declined by more than 40%. This is more surprising as medical admissions are not typically elective and admissions cannot usually be delayed. For example, one does not choose to develop a pneumonia or gastroenteritis that is severe enough to necessitate an admission.

This suggests either that there is some surplus demand for medical admissions that could be mitigated with proper intervention or that necessary care is currently being forgone.

In the case of the former, care systems could be better designed to minimise superfluous admissions. This would require the reorganisation of healthcare providers into patient centered teams with aligned reimbursement models. Certain managed care techniques would also need to be reconsidered.

If care is being forgone due to COVID-19 and the lockdown, we could expect health outcomes to deteriorate. Mortality rates and other adverse outcomes may rise. There is a risk that patients delay seeking care for too long and only engage the health system when their conditions are more severe.

The more than 50% decline in the hospital admission rate will save medical schemes more than R1 billion million a week for so long as the trend is sustained. Over a five-week lockdown period savings will exceed R5.0 billion.

This raises the question as to how these funds should be utilised in these extraordinary times. The more conservative amongst us might suggest that funds should be used to build reserves in preparation for the full force of COVID-19 or to facilitate temporary financial relief for members.

A less obvious but more proactive approach would be to directly capacitate the public and private healthcare sectors in the interest of members. Conservatively, R5.0 billion could fund the production of more than twenty thousand ventilators and countless pieces of personal proactive equipment. Twenty thousand ventilators could cater to the needs of more than four hundred thousand infected.

Perhaps, all these approaches should be pursed but to varying degrees. Funds should be directed towards the building of reserves, facilitating temporary financial relief for members and the procurement of vital healthcare equipment. In this way, schemes can play their part in combatting COVID-19.