With more than 9000 complaints received, PFA urges funds to resolve disputes internally

Muvhango Lukhaimane

Total complaints finalised

New complaints received

Complaints received by geographical area

Categories of complaints

Key Figures

Rather than just determining all the complaints it receives, the Office of the Pension Funds Adjudicator also seeks to maintain the trust between funds and their members by using the refer-to-fund (RtF) process.

During the RtF process, the Office of the Pension Funds Adjudicator (OPFA) facilitates the lodging of a complaint with the fund for internal dispute resolution.

Pension Funds Adjudicator Muvhango Lukhaimane has reported that a notable number of disputes have been resolved in this manner without the need for a formal complaint being registered and investigated.

“The RtF process has been largely welcomed by the industry and it continues to mature for those funds that do not have compliance issues,” she said in the 2023-2024 annual report of the OPFA.

“During the year under review, 699 disputes were resolved via the RtF process, which is approximately 10% higher than in 2022/23.

“For those funds that failed to take advantage of this process, however, it is hoped that with time, constant encouragement, and an increase in compliance-related regulations, all funds will fully embrace the RtF process as a means of addressing dissatisfaction by their members and increasing trust in the system,” said Lukhaimane.

A total of 9 177 new complaints were received for the 2023/24 financial year, which translates into an average of 765 complaints a month. This was a marginal decrease of 0.14% when compared to the previous year and an increase of 3.60% when compared to the 2021/22 financial year.

A total of 8 399 complaints were investigated and finalised as either determinations, out of jurisdiction, or settlements. In total, this represents an increase of 25% in the number of cases closed compared to the previous year.

In keeping with its mandate to resolve complaints in an expeditious manner, 77% of complaints finalised as either determinations, out of jurisdiction, or settlements were done within six months. However this represents a decrease of 5% compared to the previous year.

“Some of the decrease can be attributed to certain retirement funds that are habitually uncooperative by failing to provide proper responses to complaints or funds undergoing some form of regulatory intervention by the Financial Services Conduct Authority (FSCA) where the grievances raised by complainants are of secondary concern to the statutory manager,” said Lukhaimane.

The Private Security Sector Provident Fund (PSSPF) remained the largest contributor to new complaints with a total of 3 654 lodged by members of the PSSPF.

Ms Lukhaimane said the requirement for compulsory membership in the PSSPF by security guards remains questionable as employers continue to evade the requirement to pay contributions and this problem has evolved into an “acceptable business practice”for the private security industry, notwithstanding the existence of a collective bargaining agreement, an independent regulator in the private security sector, and criminal consequences for defaulters in terms of the Pension Funds Act.

“The PSSPF board of management appears to be unwilling to hold defaulting employers liable with the majority of complaints arising from individual members as and when they become entitled to benefits.

“The PSSPF has been encouraged to monitor, identify and act against its defaulting employers as it is required to do in terms of legislation.

“Adding to the problem, the PSSPF and its administrator are failing to allocate contributions paid by compliant employers timeously, leading to delays in processing of benefits.

“The PSSPF and its administrator also fail to communicate with one another whereby the fund will issue a letter confirming an employer as compliant and the administrator will state that the very same employer is in arrears with their contributions.

“If one considers that the purpose of the PSSPF is to provide retirement benefits, the fund does not appear to be achieving its purpose since the majority of its members do not remain in the fund until retirement age given the nature of their occupation.

“The impact of the introduction of access to the savings component via the two-pot system is expected to create further issues for PSSPF as members will become aware, when attempting to claim, that their employer is noncompliant.

“This will likely lead to an escalation in the number of complaints lodged by members of the PSSPF, a development that will further strain the resources of the OPFA,” said Lukhaimane.

Complaints pertaining to withdrawal benefits continue to be the most dominant category of complaints investigated and closed by the OPFA, together with non-compliance with section 13A (non-payment of contributions by participating employers). Jointly, these two categories constitute 84% of the total closed complaints categories, with almost 50% of these types of complaints arising from members of the PSSPF.

Ms Lukhaimane also reported that a new trend has emerged after the rules of the PSSPF were amended to reduce the contribution rate from 7,5% to 5% effective from 01 September 2021 to 28 February 2024. With effect from 01 March 2024, the contribution rate is 6,5%.

“This has been exploited by unscrupulous employers that continued to deduct contributions at the higher percentage from members’ wages and pay over the lower percentage to PSSPF. Again, this points to a failure by PSSPF and its administrator to compare deductions to schedules and the regulated industry salary scales,” she said.

Persons aggrieved with the decisions of the PFA are permitted by law to either make an application to the High Court or apply for reconsideration at no cost to the Financial Services Tribunal (FST). During the year under review 81 applications were made and 69 decisions were issued by the FST. Among these 54 upheld PFA decisions whilst 15 were remitted for reconsideration by the OPFA.

Click here to read more...

______________________________________________________________________________________________________

Stakeholders give OPFA 84% satisfaction rating

The Office of the Pension Funds Adjudicator (OPFA) has received a resounding thumbs up from the majority of its stakeholders who believe it is delivering on its mandate.

As a public entity, stakeholder feedback is an essential pillar in enhancing the quality of the OPFA’s customer service and ensuring it is adhering to its mandate.

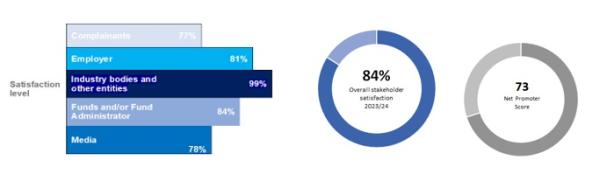

Over 200 stakeholders participated in a survey and these included complainants, pension funds and administrators, industry bodies, employers and the media. The OPFA achieved an 84% overall stakeholder satisfaction rating, which is a marked improvement from the 64% achieved in the baseline survey conducted in the 2020/21 financial year.

The OPFA had a target of 60% stakeholder satisfaction rate for the 2023/24 financial year, escalating to a desired outcome of 90% customer satisfaction by 2027/28.

Almost all industry bodies who participated in the survey noted that they were satisfied with engagements and interactions with the OPFA, for all the main strategic goals of the organisation.

“The OPFA achieved an 84% stakeholder satisfaction rating, surpassing the targeted satisfaction rate. There was 99% satisfaction from industry bodies, 84% from funds or fund administrators, 81% for employers and 77% for complainants.

“The overall survey findings are positive and provide the OPFA with good insights on what can be improved within the core areas of its business,” said Pension Funds Adjudicator Muvhango Lukhaimane.

In general, OPFA stakeholders prefer person-to-person engagement (29% of the respondents), even though positive feedback was received about the user-friendly interactivity of the OPFA website (13%). Complainants prefer lodging complaints online through email and website at an aggregate of 59%, and 10% of them still prefer visiting OPFA offices. This is reportedly positive for the OPFA which adapted quickly during and post Covid-19 to utilising technology and innovation effectively to continue to provide access to its stakeholders.

Ms Lukhaimane said specific issues were raised regarding longer turnaround times in handling complaints. She acknowledged the OPFA needs to communicate to its complainants clearly and continuously about the progress of complaints, but also explain the legal procedures required for a fair process, which at times may take relatively long to obtain responses from funds, fund administrators and employers to be able to finalise the complaint properly.

A limited number of stakeholders (22%) were not fully satisfied that the OPFA disposes of complaints in a procedurally fair manner, mainly the media and complainants, even though 86% agree that they were given sufficient opportunity to respond and 71% were satisfied that they were informed of the appeal process that was free of charge when they are not satisfied with the outcome of the complaint. While this may be due to an information gap regarding the legal processes followed in disposing of a complaint in accordance with the Act, this will be interrogated further by the OPFA.

Most of the stakeholders (85%) are of the view that the services of the OPFA were efficient and valuable. However, complainants were not entirely satisfied with provision of information regarding checking of progress status of complaints by OPFA officials. This information is already contained in the complaint forms, and on awareness presentations conducted but the OPFA needs to extensively highlight this information, especially the use of the website which is user-friendly and interactive.

Ms Lukhaimane said there is room for improvement regarding availability of OPFA officials. Overall, awareness levels of the work of the OPFA for all categories of stakeholders is at an impressive 97%.

Among the recommendations submitted by stakeholders was that the OPFA should consider naming and shaming non-compliant funds or funds administrators or employers; and the OPFA must devise an effective plan to garner support and agency from the government, regulators, and entities with enforcement powers to ensure that there are punitive measures for those that ignore the determinations of the OPFA.

Ms Lukhaimane said based on the findings of the stakeholder satisfaction survey, it was notable that the OPFA is living up to its core mandate of resolving pension fund complaints in a procedurally fair, expeditious and economic manner whilst achieving meaningful engagement with its key stakeholders.

“The OPFA will interrogate the findings and recommendations made and develop an action plan that will endeavour to address shortcomings and leverage the positives for more impactful engagements with stakeholders while delivering on its mandate diligently,” she said.

______________________________________________________________________________________________________

All stakeholders must strengthen trust in the Two-Pot System

In drafting the operational report of the annual report of the Office of the Pension Funds Adjudicator several months ago, Muvhango Lukhaimane predicted that the launch of the two-pot retirement system would see a surge in complaints.

Ms Lukhaimane, the Pension Funds Adjudicator, said in the OPFA 2023-2024 annual report which was released this week, that there would be an increase in complaints, especially at the initial stages of implementation because of non-compliant employers.

Her forecast has come true - since the launch of the two-pot system on 1 September 2024, thousands of employees have found that the funds deducted by their employers had not been paid over to the funds.

Political parties have raised concerns about missing pension fund money and employees and their unions have staged protest marches.

The two-pot system was introduced to help South Africans manage financial stability and flexibility. One-third of total contributions goes into the savings component and two-thirds into the retirement component. The two-pot system aims to address past challenges where people could not access their benefits when faced with serious financial hardship whilst in employment and for those that cash out their full pension savings when changing jobs, leaving nothing for retirement.

With the new system, from the value of the fund on 31 August 2024, 10% or R30 000, whichever is lower, would be allocated to the savings component as seeding capital. A once-off taxable withdrawal per annum from the savings component was allowed from 1 September 2024.

The rush by members to withdraw from the savings component, inadvertently exposed widespread maladministration as many security firms, municipalities and employers in other sectors have been caught withholding contributions meant for fund members.

Over the years companies have come under fire for short-changing their employees by deducting pensions from their salaries and not handing those deducted amounts over to funds. The Financial Sector Conduct Authority has exposed 3 000 employers for not paying pension funds last year.

Lukhaimane said that with the launch of the two-pot system, more complaints were expected from workers, mainly due to inadequate member communication and education, poor records management by funds and disputes regarding value of benefits withdrawable from the savings pot.

“The successful implementation of the two-pot system will require collaboration and a concerted effort from all stakeholders to strengthen trust in the retirement system.

“The OPFA anticipates an unheralded volume of complaints as members seek to withdraw from the savings component, highlighting the need for funds to ensure readiness and provide clear communication to members.

“It is also imperative that funds register their two-pot rule amendments with the FSCA within the prescribed timelines, to avoid prejudice to members,” said Ms Lukhaimane.

She said the OPFA has developed a response plan that includes deployment of additional resources, staff training and a stakeholder engagement plan specific to the two-pot retirement system.

The past financial year also saw significant developments which highlight the interconnectedness of various stakeholders that operate within the retirement fund system.

One of these was the release of the National Treasury’s policy statement, “A Simpler, Stronger Financial Sector Ombud System” that aims to reform the financial ombud

system in South Africa, strengthening consumer trust and ensuring the system is accessible, efficient, and effective.

The reformed system will include the National Financial Ombud Scheme South Africa (NFOSA), which consolidates various financial ombud schemes into a single entity. A Retirement Fund Ombud is to be created by renaming the OPFA. For now, the OPFA remains separate from the NFOSA.