Your clients get another layer of protection

The financial services regulatory authorities have at last put the finishing touches to the consumer protection supervisory mechanisms envisioned in the Financial Sector Regulation (FSR) Act. This follows the establishment of an Ombud Council and appointment of the Chief Ombud, which many commentators have lauded as a super ombudsman structure to preside over the country’s already substantial consumer complaints resolution machinery. [Note to readers: Yes, I am aware that the word (sic) ‘Ombud’ is somewhat of a capitulation by local regulators as a misguided attempt at gender or political correctness, so please bear with me … I have mostly used their ‘Ombud’ instead of the original and correct ‘ombudsman’ in today’s piece.]

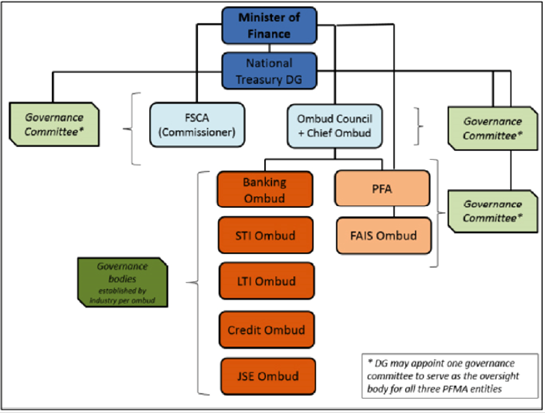

Caption: Structure of the Ombud systems in the FSR Act (source, FSCA)

Announcing a super ombudsman

The super ombudsman title is probably deserved, given that it will effectively operate as the regulator of both industry and statutory ‘dispute resolution’ schemes within the financial services sector, with authority to standardise best practices and promote and coordinate cooperation between them. “The Ombud Council [will] establish a single point of entry into the Ombud system, by clarifying the relationships between the Ombud Council, the various Ombud schemes, financial institutions and the Financial Sector Conduct Authority (FSCA),” writes Reneilwe Mthelebofu, of the Communication and Language Services team at the FSCA. It will recognise all of the existing industry schemes while it works towards establishing consistent governance procedures and standards of practice over time.

From a consumer perspective, the change should be welcomed as a sensible step towards simplifying and streamlining the submission of complaints against financial services providers (FSPs). Per National Treasury’s formal announcement of the scheme: “The objective of the Ombud Council is to assist in ensuring that financial customers have access to, and are able to use affordable, effective, independent and fair alternative dispute resolution processes for complaints about financial institutions in relation to financial products, financial services and services provided by financial infrastructures”. The industry will still be serviced by a smorgasbord of schemes, including the Banking Ombud; Credit Ombud; JSE Ombud; Long-term Insurance Ombud; and Short-term Insurance Ombud alongside the FAIS Ombud and Pension Funds Adjudicator.

On equity, fairness and TCF

We can also expect these schemes to continue along their treating customers fairly (TCF) journeys, each being required to consider principles of equity and fairness in addition to the law of contract and financial services legislation when investigating complaints and making decisions.

All stakeholders to the complaints process should benefit from a uniform framework of external dispute resolution mechanisms being applied consistently across the financial services sector. And although advisers and brokers might be excused for thinking they face a Wheel of Fortune insofar which Ombud scheme they eventually face, it would appear that both the complaints and operational processes will not differ massively from before. One hope is that complaints end up at the right channel from the ‘get go’ … and that the practice among unhappy consumers of using the FAIS Ombud as a last means of financial redress is addressed.

The Finance Minister has appointed Eileen Meyer as the Chief Ombud for the Ombud Council, for a short transitional period, and the Ombud Council’s Board of Directors is quorate, with members including: Deanne Wood (Chairperson); Adv Dikeledi Chabedi (Vice Chairperson); Emmanuel Lekgau; Silindile Kubheka; Adam Horowitz; and Charmaine Soobramoney.

Timely resolution would be most welcome

Consumers and financial services professionals will be watching closely to see whether adding another layer of supervision will result in improved complaints resolution outcomes. A common issue, going back decades, is that the process takes far too long. The Ombudsman for Short-term Insurance, for example, applauds its average complaints resolution time of 136 days (Annual Report 2020) while the FAIS Ombud (Annual Report 2019-20) is still sitting on more than 1000 property syndication matters that were lodged more than a decade ago!

“The establishment of the Ombud Council to transform the financial sector comes with many advantages and expectations,” concluded Mthelebofu. “Not only will financial customers enjoy more customer-centric services and products from financial institutions, they will also get better protection from a dispute resolutions process that is effective, independent, fair and timely”. We are not sure about the super ombudsman’s impact on customer-centric services and products; but we hope the wish for effective, independent, fair and timely complaints resolution comes true.

Writer’s thoughts:

A common management failing is to allocate more financial and / or human resources to a problem in the hope that it will be resolved. As I read about the establishment of our super ombudsman, my thoughts turned to the oft-repeated anecdote of adding more managers to the mix when increasing the productive workforce is all that is actually required. Do you think that an additional supervisory layer above South Africa’s existing industry and statutory Ombud schemes will result in better complaints resolution outcomes for consumers and / or FSPs? Please comment below, interact with us on Twitter at @fanews_online or email us your thoughts [email protected].

Comments

Report Abuse